Retirement

Can you still bring forward your non-concessional cap?

New rules regarding non-concessional super contributions mean Australians need to be across current legislation to avoid landing in hot water.

Can you still bring forward your non-concessional cap?

New rules regarding non-concessional super contributions mean Australians need to be across current legislation to avoid landing in hot water.

The introduction of the new $1.6 million cap has changed the game for members wanting to make contributions in advance – so-called bring-forward contributions. The legislation not only introduces eligibility requirements, it also requires members to meet further criteria at the beginning of each year, making up their bring-forward period before being able to use any shortfall from a previous year in that bring-forward period.

Can a member still bring forward their non-concessional cap?

The existing rules allow a member to pay up to three years’ worth of the $180,000 annual non-concessional contribution limit in one go. Once they reach that three-year maximum amount ($540,000) they can’t contribute any further non-concessional amounts in those three years. Paying up to three years’ worth upfront is referred to in superannuation industry parlance as a member’s ‘bring-forward’ strategy.

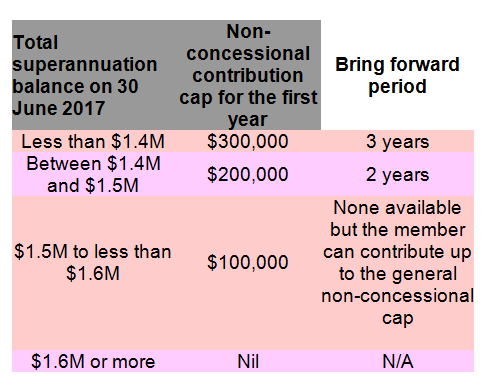

The rules around using the bring-forward cap have changed. Firstly, the annual maximum limit has been decreased from $180,000 to $100,000. In addition, the member must also meet the following eligibility criteria:

1. The amount that is being contributed must exceed the annual non-concessional cap;

2. The member’s total superannuation balance at 30 June of the previous financial year must be under the general transfer balance cap ($1.6 million);

3. The member must be under the age of 65 at any time during that financial year;

4. The bring forward must not have been triggered in the last two financial years; and

5. The difference between the general transfer balance cap ($1.6 million for 2017-18) and the member’s total superannuation balance is higher than the annual non-concessional cap ($100,000 for 2017-18).

Once the member has ticked all of the above boxes, they have to ascertain what their bring-forward cap and their bring-forward period are.

Under the new rules, a member is no longer able to automatically bring forward three years’ worth of contributions in one year. Instead, the maximum amount will be either two or three times the annual cap, depending on the member’s total superannuation balance at 30 June immediately before the relevant financial year (being the year during which the bring forward is to be triggered). A summary table has been included below.

If the member does not fully use their bring-forward cap in year one (being the year during which the bring forward is triggered), their cap for year two will be the unused portion of their cap from year one, provided their total superannuation balance as at 30 June before the start of year two is below the general transfer balance cap.

A similar approach will be adopted in year three. In that year, the cap for year three will be the unused portion of the bring-forward cap from year two.

What if a member’s superannuation balance is over the general transfer balance cap at the beginning of year two?

If their balance is over the general transfer balance cap, the cap for year two is nil.

Provided the member is eligible to contribute again in year three (because their total superannuation balance has gone below the cap for instance), their cap available for year three is the unused portion of their cap from year one.

If the member is not eligible in year three, their cap for that year is nil and the member cannot make any non-concessional contribution in that financial year. The bring-forward cap and period will reset the following year.

What this means is that being ineligible to contribute in year two does not automatically mean that the member has lost the ability to access the unused portion from year one nor does it prematurely terminate the three-year bring-forward period.

What happens if a member has already triggered their bring forward in the 2015-16 or 2016-17 financial years?

Transitional arrangements will apply in the above circumstances.

If triggered in 2015-16 and not fully utilised by 30 June 2017:

According to the legislation, if the member brought forward their non-concessional cap in 2015-16, the cap available in year three is calculated in accordance with the new rules (i.e. unused portion of caps from year one and year two) as if the cap in year one was $460,000.

Example – Laura

Laura has a superannuation balance of $700,000. We assume she meets all eligibility criteria to trigger the bring forward in each of the three years of her bring-forward period.

She triggers the bring forward in 2015-16 (year one), with a $250,000 non-concessional contribution (the bring-forward cap in that year is $540,000).

• What is her cap for 2016-17 (year two)?

Her cap available in 2016-17 is $290,000 = $540,000 (current bring-forward cap) – $250,000 (contribution in year one).

In year two, she makes a non-concessional contribution of $100,000.

• What is her cap for 2017-18 (year three, being year of transitional rules)?

Cap available is $110,000 = $460,000 (the amended bring-forward cap as per legislation) – ($250,000 + $100,000) (being the total non-concessional contributions made in year one and year two).

If triggered in 2016-17 and not fully utilised by 30 June 2017:

For members who triggered the bring forward in 2016-17, it is both the caps for year two and year three which are calculated in accordance with the new rules (i.e. unused portion of cap from year one and year two) as if the cap in year one was $380,000.

Example – John

John has a superannuation balance of $600,000. We assume he meets all eligibility criteria to trigger the bring forward in each of the three years of his bring-forward period.

He triggers the bring forward in 2016-17 (year one) with a $250,000 non-concessional contribution (the bring-forward cap in that year is $540,000).

• What is his cap for 2017-18 (being year two, the year of transitional rules)?

His cap available in 2017-18 is $130,000 = $380,000 (the amended bring-forward cap as per legislation) – ($250,000) (the non-concessional contributions made in year one).

In year two, he makes a non-concessional contribution of $100,000.

• What is his cap for 2018-19?

Cap available is $30,000 = $380,000 (the amended bring-forward cap as per legislation) – ($250,000 + $100,000) (the total non-concessional contributions made in year one and year two).

The bring-forward cap and period reset in 2019-20.

Take away points

The 2016-17 financial year is the last year members can make a non-concessional contribution of up to $540,000, including in-specie contributions so, if possible, members should look at maximising their contributions to utilise any unused portion of their current cap by the end of the financial year.

As in-specie contributions take several months to complete, we strongly recommend that individuals who are considering undertaking such transactions proceed as soon as possible to ensure the contribution is effected in the current financial year to benefit from the higher non-concessional and bring-forward caps. Failure to do so may create excess contribution complications.

Concessional duty is available in certain states on the transfer of business real property from member(s) to their super fund. Please contact our office if you require assistance with these transactions and application for concessional duty.

Julie Hartley, solicitor, Townsends Business & Corporate Lawyers

RELATED ARTICLES

Superannuation

Rest posts healthy returns following a positive end to 2025

Rest, one of Australia's largest profit-to-member superannuation funds, has reported impressive returns in its flagship MySuper Growth investment option for the year 2025. The fund is optimistic about ...Read more

Superannuation

Rest marks milestone with first private equity co-investment exit

In a significant development for Rest, one of Australia’s largest profit-to-member superannuation funds, the organisation has announced the successful completion of its first private equity ...Read more

Superannuation

Expanding super for under-18s could help close the gender super gap, says Rest

In a push to address the gender disparity in superannuation savings, Rest, one of Australia's largest profit-to-member superannuation funds, has called for a significant policy change that would allow ...Read more

Superannuation

Employment Hero pioneers real-time super payments with HeroClear integration

In a significant leap forward for Australia's payroll and superannuation systems, Employment Hero, in collaboration with Zepto and OZEDI, has successfully processed the country's first ...Read more

Superannuation

Rest launches Rest Pay to streamline superannuation payments and boost member outcomes

In a significant move aimed at enhancing compliance with upcoming superannuation regulations, Rest, one of Australia’s largest profit-to-member superannuation funds, has unveiled an innovative ...Read more

Superannuation

Rest appoints experienced governance expert to bolster superannuation fund

Rest, one of Australia's largest profit-to-member superannuation funds, has announced the appointment of Ed Waters as the new Company Secretary. Waters, who brings with him over 15 years of extensive ...Read more

Superannuation

Small businesses brace for cash flow challenges as Payday Super becomes law

With the new Payday Super legislation now enacted, small businesses across Australia are preparing for a significant shift in how they manage superannuation contributions. The law, which mandates a ...Read more

Superannuation

Rest launches Innovate RAP to support fairer super outcomes for First Nations members

In a significant move towards reconciliation and inclusivity, Rest, one of Australia's largest profit-to-member superannuation funds, has unveiled its Innovate Reconciliation Action Plan (RAP)Read more

Superannuation

Rest posts healthy returns following a positive end to 2025

Rest, one of Australia's largest profit-to-member superannuation funds, has reported impressive returns in its flagship MySuper Growth investment option for the year 2025. The fund is optimistic about ...Read more

Superannuation

Rest marks milestone with first private equity co-investment exit

In a significant development for Rest, one of Australia’s largest profit-to-member superannuation funds, the organisation has announced the successful completion of its first private equity ...Read more

Superannuation

Expanding super for under-18s could help close the gender super gap, says Rest

In a push to address the gender disparity in superannuation savings, Rest, one of Australia's largest profit-to-member superannuation funds, has called for a significant policy change that would allow ...Read more

Superannuation

Employment Hero pioneers real-time super payments with HeroClear integration

In a significant leap forward for Australia's payroll and superannuation systems, Employment Hero, in collaboration with Zepto and OZEDI, has successfully processed the country's first ...Read more

Superannuation

Rest launches Rest Pay to streamline superannuation payments and boost member outcomes

In a significant move aimed at enhancing compliance with upcoming superannuation regulations, Rest, one of Australia’s largest profit-to-member superannuation funds, has unveiled an innovative ...Read more

Superannuation

Rest appoints experienced governance expert to bolster superannuation fund

Rest, one of Australia's largest profit-to-member superannuation funds, has announced the appointment of Ed Waters as the new Company Secretary. Waters, who brings with him over 15 years of extensive ...Read more

Superannuation

Small businesses brace for cash flow challenges as Payday Super becomes law

With the new Payday Super legislation now enacted, small businesses across Australia are preparing for a significant shift in how they manage superannuation contributions. The law, which mandates a ...Read more

Superannuation

Rest launches Innovate RAP to support fairer super outcomes for First Nations members

In a significant move towards reconciliation and inclusivity, Rest, one of Australia's largest profit-to-member superannuation funds, has unveiled its Innovate Reconciliation Action Plan (RAP)Read more