Retirement

Why you should own your age in bonds

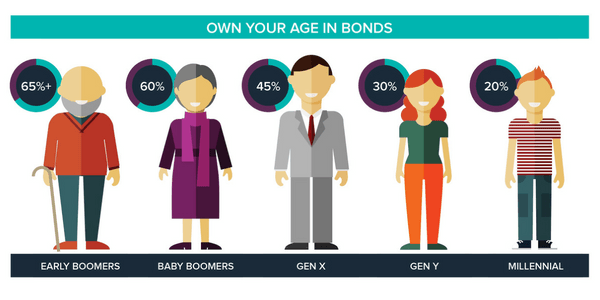

A rule of thumb coined by John Bogle, founder of global asset manager Vanguard, is that your bond allocation should roughly equal your age. While clearly not an exact science, it demonstrates the increasing need for fixed income as we move through life.

Why you should own your age in bonds

A rule of thumb coined by John Bogle, founder of global asset manager Vanguard, is that your bond allocation should roughly equal your age. While clearly not an exact science, it demonstrates the increasing need for fixed income as we move through life.

If, like me, you’re Gen X or a Baby Boomer, chances are you’ve worked hard and done your best to save for retirement. The great thing about retiring is the chance to move away from full-time work and finally enjoy the things you’ve never had time to. The downside is that you no longer receive a regular salary.

The challenge lies in creating predicable and regular income. Income that can weather difficult market conditions and meet the longevity test without adding risk to your capital. This challenge is top of mind for a growing number of Australians now.

For many retirees, term deposit (TD) income has become their ‘salary’. Australian household deposits just ticked over $810 billion dollars (according to APRA banking statistics Oct 2016), with a large part of this being TDs. TDs are popular because they offer savers less risk than many other investments.

For other investors, high-dividend yielding shares are a key source of income. While both are valuable assets in their own right, it’s important to recognise the limitations of eachm and how bonds can help deliver that stable, regular income your salary once did.

Shares – no longer the golden goose

Even for the most ardent equity investor, it has become clear that the halcyon days of the 1990s and early 2000s are over. Recent dividend cuts are not one-offs and Australian share dividends are on the decline. Australian companies have been paying out far more than in other countries and this doesn’t appear sustainable.

We shouldn’t overlook the volatility of shares and the intermittent post-GFC series of shock waves that cause fear and uncertainty every six months. With share markets, you could decide to wait and find out. If Aussie shares hold up, we’ll be the lucky country like we were post-GFC. But if Australian companies can’t sustain this level of dividends, your shares may tumble, along with the income you want.

The question for all of us is, “Do I want to take this risk?” Millennials may say yes but, if you’re a retiree, or close to it, you can’t afford to be cavalier with your future.

Don’t get me wrong. Well-selected shares represent a great investment and should form a component of most investment portfolios, regardless of age. But can they be relied upon for regular, long-term, stable income?

Term deposits – the search for stable income

You may not have the luxury of waiting for your savings to recover in five to 10 years. With dividends also at risk, waiting it out isn’t a sustainable proposition if your income relies on shares. Recognising this, many Australians have turned to the investments that sit below shares on the risk return spectrum.

If you have TDs, you already have a great start towards achieving a stable income. As per John Bogle’s words, the older we get, the greater our allocation to these sorts of investments should be. But the low rate economy is really hampering the returns TDs can offer. You would have watched your TD rates fall further over the past few years. I’m sure you’re now wondering if there is a way to increase your ‘salary’ without jumping onto the equity or hybrid roller-coaster.

Corporate bonds are worth a look

Fixed income generally provides investors with more secure and capital stable investments than shares, hybrids, property and other growth assets. But not all fixed income investments are equal.

Government bonds are lower yielding than TDs because they have an even lower investment risk. Investors have tended to bypass these, opting instead for higher yielding TDs. However, government bonds dominate key Australian indices that fixed income managed funds benchmark against and many fixed income ETFs track.

If you own fixed income managed funds or ETFs, chances are you are already invested in low-yield government bonds. The funds are safer for having government bonds in them as they are less likely to default, but this takes away from their yields.

Corporate bonds generally have higher yields than TDs. There are a number of ways to access corporate bonds, including bond ETFs and managed funds. However, both of these have a key limitation – they do not mature. They are perpetual investments so you cannot predict the future income and capital you will receive from them, which makes your retirement planning much harder.

If you want to control the timing and exact return on your savings, looking at individual bonds may be a better strategy. XTBs provide access to senior bonds of top 100 ASX companies and are traded on the ASX. This makes them a capital stable and relatively safe investment. Compared to government bonds, TDs or cash management accounts, XTBs provide the same steady and predictable income but also offer potentially higher returns. Sitting above cash, but lower than shares in the capital structure, corporate bonds can deliver greater returns than cash, with much lower risk than shares.

For example, you might be looking at a return of 2.2 per cent from the bank on your term deposits (Canstar November 2016), but you could get 3.5 per cent from a portfolio of XTBs. It might not look like much at first blush, but that is more than a 50 per cent increase in your ‘salary’.

If your savings are invested too aggressively in the retirement phase and the share market drops, it will become extremely hard to rebuild your assets. Fixed income can play an important role in generating solid, regular income for investors. Offering strong capital preservation benefits, allocating some of your savings to corporate bonds can be a great way to safeguard your retirement savings.

Any interest rate increase will cause bond prices to fall, and bond funds and ETFs will drop in value. The corporate bonds covered by XTBs on the ASX have an average term of three to four years, so holding to maturity isn’t onerous and is often what investors intend to do. Whether bond prices fall or not, by holding to maturity you already know what return you’re going to get, which is the yield you bought at in the first place.

Bond price falls don’t impact you if you hold to maturity (assuming the bond issuer does not default). But if you own bonds in a fund or ETF, price falls do impact you because funds and ETFs are perpetual so the capital loss is locked in.

John Bogle’s rule of thumb is a great place to start. If you’re nudging retirement and are heavily weighted towards shares, it may be time to balance your portfolio out with a greater corporate bond allocation.

Richard Murphy, chief executive & co-founder, Australian Corporate Bond Company

RELATED ARTICLES

Retirement Planning

New digital platform revolutionises retirement planning for Aware Super members

A groundbreaking digital platform by Aware Super is transforming the way retirees plan and manage their pensions, with significant results already seen in the pilot phase. The tool, named Retirement ...Read more

Retirement Planning

The retirement mortgage squeeze: how one bank turned a demographic risk into a strategic edge

An increasing share of Australians are entering their 60s still paying off mortgages, just as living costs and interest charges stay stubbornly high. For banks, super funds, retailers and ...Read more

Retirement Planning

The retirement mortgage crunch: what it means for banks, retailers and policy in Australia

A growing share of Australians are carrying mortgages into their 60s and beyond, colliding with persistent cost-of-living pressures and a “slow grind” macro outlook. This isn’t just a social story; it ...Read more

Retirement Planning

Majority of Australians still unsure about their retirement prospects

A recent survey conducted by MFS Investment Management® has shed light on the ongoing uncertainty faced by many Australians regarding their retirement plans. Despite a slight increase in confidence ...Read more

Retirement Planning

Wage growth steadies as businesses navigate economic challenges

In a sign that the Australian labour market may be finding equilibrium, wage growth has stabilised this quarter, according to Employment Hero's latest data. This development comes as employers ...Read more

Retirement Planning

Simplified retirement advice: Key to overcoming behavioural biases, experts say

In a bid to enhance retirement outcomes for Australians, a recent whitepaper by Industry Fund Services, in collaboration with Challenger, has highlighted the importance of simplifying retirement ...Read more

Retirement Planning

Rest launches Retire Ready digital experience to empower members approaching retirement

Rest, one of Australia’s largest profit-to-member superannuation funds, has unveiled a new digital experience aimed at making retirement preparation simpler and more personalised for its members. Read more

Retirement Planning

New Framework Aims to Bridge Australia’s Financial Advice Gap

A ground-breaking framework introduced by the Actuaries Institute promises to revolutionise how Australians access financial support, potentially transforming the financial wellbeing of millionsRead more

Retirement Planning

New digital platform revolutionises retirement planning for Aware Super members

A groundbreaking digital platform by Aware Super is transforming the way retirees plan and manage their pensions, with significant results already seen in the pilot phase. The tool, named Retirement ...Read more

Retirement Planning

The retirement mortgage squeeze: how one bank turned a demographic risk into a strategic edge

An increasing share of Australians are entering their 60s still paying off mortgages, just as living costs and interest charges stay stubbornly high. For banks, super funds, retailers and ...Read more

Retirement Planning

The retirement mortgage crunch: what it means for banks, retailers and policy in Australia

A growing share of Australians are carrying mortgages into their 60s and beyond, colliding with persistent cost-of-living pressures and a “slow grind” macro outlook. This isn’t just a social story; it ...Read more

Retirement Planning

Majority of Australians still unsure about their retirement prospects

A recent survey conducted by MFS Investment Management® has shed light on the ongoing uncertainty faced by many Australians regarding their retirement plans. Despite a slight increase in confidence ...Read more

Retirement Planning

Wage growth steadies as businesses navigate economic challenges

In a sign that the Australian labour market may be finding equilibrium, wage growth has stabilised this quarter, according to Employment Hero's latest data. This development comes as employers ...Read more

Retirement Planning

Simplified retirement advice: Key to overcoming behavioural biases, experts say

In a bid to enhance retirement outcomes for Australians, a recent whitepaper by Industry Fund Services, in collaboration with Challenger, has highlighted the importance of simplifying retirement ...Read more

Retirement Planning

Rest launches Retire Ready digital experience to empower members approaching retirement

Rest, one of Australia’s largest profit-to-member superannuation funds, has unveiled a new digital experience aimed at making retirement preparation simpler and more personalised for its members. Read more

Retirement Planning

New Framework Aims to Bridge Australia’s Financial Advice Gap

A ground-breaking framework introduced by the Actuaries Institute promises to revolutionise how Australians access financial support, potentially transforming the financial wellbeing of millionsRead more