Invest

Supplementing super with investment bonds

It’s no secret that Australia’s population is ageing and, at the same time, you’re likely to live a longer life than past generations thanks to advancements in healthcare and a higher standard of living.

Supplementing super with investment bonds

It’s no secret that Australia’s population is ageing and, at the same time, you’re likely to live a longer life than past generations thanks to advancements in healthcare and a higher standard of living.

This is great news – the opportunity to retire and have another 25 years or so of living ahead of you.

But… do you have sufficient retirement savings to see you through? While superannuation is arguably one of the most important investments you can make, recent changes to the superannuation system have far-reaching strategy implications for many. As a result, it’s important to consider tax effective strategies outside of superannuation that can be used to bolster your retirement savings.

From 1 July 2017, major changes to superannuation came into effect. These changes include:

- restrictions to the amounts that can be contributed into superannuation, both as concessional and non-concessional contributions;

- a $1.6 million superannuation transfer balance cap on the total amount of superannuation an individual can transfer into pension phase; and

- the removal of the tax exemption for transition-to-retirement.

The current tax position of an investment bond is not subject to any proposed change, other than a favourable tax rate reduction (from its current rate of 30 per cent) in the future.

The limitations of super

Superannuation can be a tax effective way to save for retirement. The maximum tax payable on superannuation is 15 per cent; low when compared to the highest personal marginal tax rate of 47 per cent (including the Medicare levy).

However, there are limits and constraints with super, and you may need complementary investments to supplement it as part of your overall retirement investment strategy.

1. Limited contributions

To contribute to superannuation, you must meet eligibility rules. Individuals under the age of 75 are permitted to claim a tax deduction for personal super contributions. If eligible, contribution caps will limit the amount you can contribute to your super fund.

Contributions from an employer, including amounts paid under a salary sacrifice agreement, and contributions for which a personal tax deduction is claimed cannot exceed $25,000 in a financial year.

Personal after-tax contributions are not taxed on amounts up to the non-concessional (personal after-tax) contributions cap, which is $100,000 in a financial year.

Under age 65, you may be able to combine the limits for three years to contribute up to $300,000 in a single year. This is subject to the new transfer balance cap of $1.6 million.

Superannuation receives tax concessions, but in exchange, access to money is restricted until a ‘condition of release’ is met. This generally means that you cannot access your superannuation until you reach ‘preservation age’ and have retired.

2. Access restrictions

If you were born before 1 July 1960, your preservation age is 55; it increases to age 60 for those born after this date. In some cases, such as permanent disability, earlier access may be allowed.

An alternative tax effective structure such as an investment bond can be used to supplement superannuation and provide you access to your savings at a time of your choosing.

How can investment bonds supplement super?

An investment bond is a tax effective structure. Like superannuation, tax is paid within the investment bond rather than personally by the investor. The maximum tax paid on the earnings and capital gains within an investment bond is 30 per cent, although franking credits and tax deductions can reduce this effective tax rate. This makes them an attractive investment option for high income earners.

A key feature of investment bonds is that if you hold the investment for 10 years, regardless of the amount invested, you pay no personal tax. None. If the investment is redeemed within the first 10 years, you will pay tax on the assessable portion of growth. On the upside, your savings are always available to you.

There are clear benefits of using investment bonds to supplement superannuation:

1. Contributions are not limited

There is no limit on the amount you can invest to establish an investment bond. In addition, you can make subsequent investments up to a maximum of 125 per cent of the previous year’s contribution without restarting the 10-year period. You can choose to start a new investment bond if higher amounts are to be subsequently invested.

2. Access restrictions

Unlike superannuation investments, investment bonds are not subject to preservation, so you can access your savings before age 55. This is ideal if you are looking to fund an early retirement.

3. Beneficiaries

Investment bonds provide you with the freedom to nominate anyone as a beneficiary in the event of your death. Beneficiaries are not limited to ‘dependants’, as is typically required for superannuation investments.

Investment bonds provide a tax effective means of investing and a whole lot more flexibility

Case study – what next once superannuation contributions have been maximised?

Anthony is 45 years old and has invested wisely in the property market. He believes property returns have plateaued and has sold his inner-city investment property, realising a healthy capital gain. He has paid off his mortgage and maximised his concessional and non–concessional contributions to superannuation.

Anthony is considering options to invest the surplus proceeds of $200,000 in a tax effective manner. Because he earns a good income and does not need access to his funds, Anthony can adopt a long-term investment time horizon of 10 years plus.

He first considers investing in Australian shares, either directly or through a managed fund. Franking credits are important to him as they can help him reduce the tax paid, given he is on the highest marginal tax rate.

Anthony’s adviser suggests investing in an investment bond because he can benefit from franking credits from Australian shares within the investment bond. The investment bond pays tax at a maximum rate of 30 per cent per annum.

Anthony can also afford to invest additional amounts of $20,000 per annum into the investment bond for the first three years; he is unable to direct any surplus funds into superannuation without exceeding his contribution cap. In three years’ time, he plans to reduce the contribution he invests to $5,000 per year.

His adviser confirms he can redeem his investment bond and pay no additional tax after 10 years.

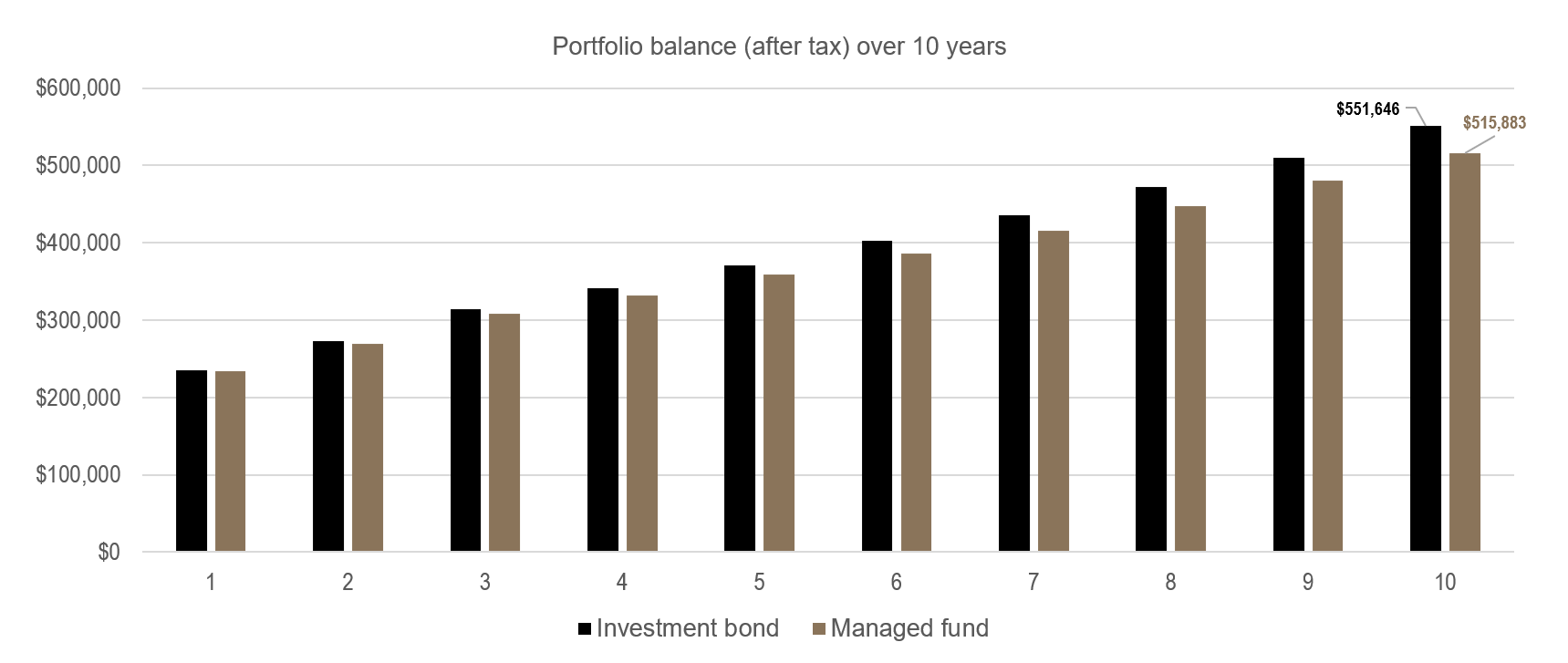

When Anthony reaches age 55, the investment bond has accumulated to approximately $551,646 (tax paid). This is estimated to be $35,763 higher than the alternative of investing at his personal marginal tax rate.

Portfolio balance (after tax) over 10 years ($35,763 higher than investing at his personal marginal tax rate)

Provided for illustrative example only based on the basic income and growth assumptions described above. This illustrative example does not purport to represent the actual return possible in any of Centuria Investment Bonds. An investment is subject to risk, the degree of which depends on the assets in which the bond invests. Assumptions: total returns of 8.5 per cent pa (4.5 per cent pa income (80 per cent franked), 4 per cent pa capital growth, 100 per cent annual turnover of the portfolio, 50 per cent CGT discount applies for managed funds).

When looking at long-term investments to supplement your super, it’s important to ensure the investment meets your needs, your investment timeframe, has the flexibility to deal with unforeseen circumstances and, where possible, is tax effective. When compared to other investments, investment bonds are the ideal vehicle through which you can supplement your retirement savings.

Neil Rogan is the general manager of investment bonds at Centuria Investment Bonds.

RELATED ARTICLES

Investment insights

Financial markets focus on shareholder engagement as companies report results

In a week dominated by financial market developments and corporate announcements, companies are increasingly recognising the importance of shareholder engagement in driving market outcomesRead more

Investment insights

Future Generation Australia declares increased dividend amid strong investment performance

Future Generation Australia (ASX: FGX) has announced a significant outperformance against the S&P/ASX All Ordinaries Accumulation Index, reporting a 14.1% increase in its 12-month investment ...Read more

Investment insights

New business landscape shifts as regional areas and company setups gain traction

The latest data from the January 2026 Lawpath New Business Index reveals a dynamic shift in how Australians are choosing to embark on new business ventures. While the overall number of new Australian ...Read more

Investment insights

Good Return secures $1 million investment from Macquarie Group Foundation to boost women-led enterprises

In a significant development for women-led enterprises across the Asia-Pacific region, Good Return has announced a $1 million investment from the Macquarie Group Foundation into its Impact Investment ...Read more

Investment insights

Beyond the trophy: what the REB Awards 2026 reveal about real estate’s next competitive play

Nearly 900 submissions for just over 30 winning slots is more than a celebration—it’s a market signal. In Australia’s roughly $10 trillion residential property market, awards have become a strategic ...Read more

Investment insights

Parents are funding know‑how, not deposits: A case study in Australia’s new first‑home playbook

With listings tight and auctions unforgiving, a quiet shift is underway: parents are increasingly paying for professional buying expertise instead of topping up deposits. This case study unpacks the ...Read more

Investment insights

State Street Markets reveals a shift in investor risk appetite amid economic uncertainties

In a recent revelation by State Street Markets, the latest State Street Institutional Investor Indicators have showcased a notable shift in investor behaviour as uncertainty looms over global ...Read more

Investment insights

UniSuper welcomes back seasoned strategist Mark Himpoo as Senior Portfolio Manager

In a strategic move aimed at bolstering its in-house investment capabilities, UniSuper has announced the return of Mark Himpoo as Senior Portfolio Manager, Equities. Himpoo's return marks a ...Read more

Investment insights

Financial markets focus on shareholder engagement as companies report results

In a week dominated by financial market developments and corporate announcements, companies are increasingly recognising the importance of shareholder engagement in driving market outcomesRead more

Investment insights

Future Generation Australia declares increased dividend amid strong investment performance

Future Generation Australia (ASX: FGX) has announced a significant outperformance against the S&P/ASX All Ordinaries Accumulation Index, reporting a 14.1% increase in its 12-month investment ...Read more

Investment insights

New business landscape shifts as regional areas and company setups gain traction

The latest data from the January 2026 Lawpath New Business Index reveals a dynamic shift in how Australians are choosing to embark on new business ventures. While the overall number of new Australian ...Read more

Investment insights

Good Return secures $1 million investment from Macquarie Group Foundation to boost women-led enterprises

In a significant development for women-led enterprises across the Asia-Pacific region, Good Return has announced a $1 million investment from the Macquarie Group Foundation into its Impact Investment ...Read more

Investment insights

Beyond the trophy: what the REB Awards 2026 reveal about real estate’s next competitive play

Nearly 900 submissions for just over 30 winning slots is more than a celebration—it’s a market signal. In Australia’s roughly $10 trillion residential property market, awards have become a strategic ...Read more

Investment insights

Parents are funding know‑how, not deposits: A case study in Australia’s new first‑home playbook

With listings tight and auctions unforgiving, a quiet shift is underway: parents are increasingly paying for professional buying expertise instead of topping up deposits. This case study unpacks the ...Read more

Investment insights

State Street Markets reveals a shift in investor risk appetite amid economic uncertainties

In a recent revelation by State Street Markets, the latest State Street Institutional Investor Indicators have showcased a notable shift in investor behaviour as uncertainty looms over global ...Read more

Investment insights

UniSuper welcomes back seasoned strategist Mark Himpoo as Senior Portfolio Manager

In a strategic move aimed at bolstering its in-house investment capabilities, UniSuper has announced the return of Mark Himpoo as Senior Portfolio Manager, Equities. Himpoo's return marks a ...Read more