Retirement

How should I adapt to the new age pension test?

On 1 January 2017, reductions to the assets test limits for the age pension will be introduced, with those who take on more risk likely to be rewarded.

How should I adapt to the new age pension test?

On 1 January 2017, reductions to the assets test limits for the age pension will be introduced, with those who take on more risk likely to be rewarded.

It is estimated that 300,0001 people will lose all or some of their pension. In the worst cases, singles will lose $9,721 per year and couples $14,002 per year.

Under the current rules, as your assets reduce, the age pension provides the equivalent of 3.9 per cent per year income. For example, if your assets fall in value by $10,000, your age pension entitlement increases by $390 per year.

From 1 January 2017, the asset test taper rate doubles. This means that as your assets reduce, the age pension will provide the equivalent of 7.8 per cent, which is nearly three times current term deposit rates. This, therefore, represents an increase in your entitlement of $780 per year for a $10,000 decline in the value of your assets.

The silver lining

The changes to the assets test are significant but one positive to flow from the changes is that you can take more risk with your investments by increasing your allocation to growth assets, such as shares and property. This could reward you over time as your long-term return could be higher.

If in the interim, share markets fall and the drop in your assets makes you eligible for the age pension, you will receive an effective age pension return of 7.8 per cent per year on top of your dividend income from your growth assets. The dividend yield on Australian shares is currently 4.6 per cent2 per year with imputation credits adding a further 1.7 per cent3 per year.

What could this investment strategy look like?

If you are currently in a defensive investment position, you should consider shares carefully. You need to ensure you have a high level of diversification and still have sufficient funds in low-risk assets (like cash and term deposits) to use when and if your growth assets fall. Holding seven years’ worth of living expenses, or 10 years if you are very conservative, in low-risk assets would substantially reduce the need to sell your shares before they recover their value.

It’s time to act now

A properly structured and monitored retirement plan can improve your ability to achieve your objectives. If you, your friends or family are aged 65-75, own your own home and have all your retirement savings in cash and term deposits, this type of strategy may help.

John and Patricia – a case study

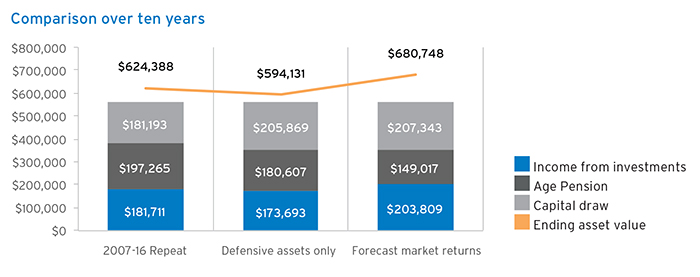

To test the effectiveness of this investment strategy and how it can work to your advantage, let’s look at John and Patricia. They are home owners, have $800,000 in counted investment assets and have living expenses of $50,000 per year. They currently receive an age pension of $14,746 per year, but after 1 January 2017, it is expected to fall to $1,248 per year.

Let’s take a look at the three options available:

1. Invest $800,000 (100 per cent) in low-risk term deposits and cash (defensive assets only).

2. Invest $500,000 in low risk/defensive investments and $300,000 in higher risk investments (shares and REITs) with long-term returns (forecast market returns).

3. Invest $500,000 in low risk/defensive investments and $300,000 in higher risk investments (shares and REITs) with a repeat of the past decade of actual returns, from 2007 to present (2007-16 repeat). Importantly this period includes the GFC4.

Assumptions:

• A 2.5 per cent interest rate per year on the low risk/defensive investments.

• Where there is a cash flow shortfall (that is, where interest income, dividend income and any age pension does not meet the living needs), the shortfall is drawn from the low risk/defensive investments, leaving the shares untouched.

• The higher risk investments are invested as follows:

o Fifty per cent Australian shares5, 40 per cent international shares6, 6 per cent international REITs7 and 4 per cent Australian REITs.

o Fees of 1.5 per cent per year are charged for product and advice.

• Options two and three retain the conservative ten years of annual expenses in low risk/defensive investments.

• Asset and income test calculations apply and assume full income testing applies to all assets (i.e. no grandfathering on any account based pensions).

The chart below shows the optimal outcome for John and Patricia is generated by using the forecast market return. The next optimal outcome is generated by using a repeat of the performance of assets during the period including the GFC. The worst ending asset value outcome is generated when John and Patricia do not allocate to any growth assets.

The case study demonstrates that John and Patricia could consider investing in some growth assets because they will ultimately end in a better position than if they were only invested in defensive assets.

Phillip Gillard, private client adviser and principal, Shadforth Financial Group

1 Age Pension: 300,000 plus Australians lose entitlements from January 2017, 15 June 2016, SuperGuide.

2 ASX300 Ex-A REIT Index, weighted average dividend to price using 12 month historical net dividends per share.

3 Based on indicated dividend yield, dividend franking percentage and the current stock price.

4 Based on actual returns in the GFC, replicated. 2018 = 2008, 2019 = 2009, etc.

5 S&P/ASX 300.

6 MSCI World.

7 FTSE EPRA/NAREIT Developed TR Hdg AUD.

RELATED ARTICLES

Retirement Planning

The retirement mortgage squeeze: how one bank turned a demographic risk into a strategic edge

An increasing share of Australians are entering their 60s still paying off mortgages, just as living costs and interest charges stay stubbornly high. For banks, super funds, retailers and ...Read more

Retirement Planning

The retirement mortgage crunch: what it means for banks, retailers and policy in Australia

A growing share of Australians are carrying mortgages into their 60s and beyond, colliding with persistent cost-of-living pressures and a “slow grind” macro outlook. This isn’t just a social story; it ...Read more

Retirement Planning

Majority of Australians still unsure about their retirement prospects

A recent survey conducted by MFS Investment Management® has shed light on the ongoing uncertainty faced by many Australians regarding their retirement plans. Despite a slight increase in confidence ...Read more

Retirement Planning

Wage growth steadies as businesses navigate economic challenges

In a sign that the Australian labour market may be finding equilibrium, wage growth has stabilised this quarter, according to Employment Hero's latest data. This development comes as employers ...Read more

Retirement Planning

Simplified retirement advice: Key to overcoming behavioural biases, experts say

In a bid to enhance retirement outcomes for Australians, a recent whitepaper by Industry Fund Services, in collaboration with Challenger, has highlighted the importance of simplifying retirement ...Read more

Retirement Planning

Rest launches Retire Ready digital experience to empower members approaching retirement

Rest, one of Australia’s largest profit-to-member superannuation funds, has unveiled a new digital experience aimed at making retirement preparation simpler and more personalised for its members. Read more

Retirement Planning

New Framework Aims to Bridge Australia’s Financial Advice Gap

A ground-breaking framework introduced by the Actuaries Institute promises to revolutionise how Australians access financial support, potentially transforming the financial wellbeing of millionsRead more

Retirement Planning

The downsizer dividend: how Australia’s ageing shift will reshape property, finance and AI strategy

Downsizing is moving from a personal milestone to a system-level lever for Australia’s housing market. As policymakers court reforms and agents eye fresh listings, the real profit pools will accrue to ...Read more

Retirement Planning

The retirement mortgage squeeze: how one bank turned a demographic risk into a strategic edge

An increasing share of Australians are entering their 60s still paying off mortgages, just as living costs and interest charges stay stubbornly high. For banks, super funds, retailers and ...Read more

Retirement Planning

The retirement mortgage crunch: what it means for banks, retailers and policy in Australia

A growing share of Australians are carrying mortgages into their 60s and beyond, colliding with persistent cost-of-living pressures and a “slow grind” macro outlook. This isn’t just a social story; it ...Read more

Retirement Planning

Majority of Australians still unsure about their retirement prospects

A recent survey conducted by MFS Investment Management® has shed light on the ongoing uncertainty faced by many Australians regarding their retirement plans. Despite a slight increase in confidence ...Read more

Retirement Planning

Wage growth steadies as businesses navigate economic challenges

In a sign that the Australian labour market may be finding equilibrium, wage growth has stabilised this quarter, according to Employment Hero's latest data. This development comes as employers ...Read more

Retirement Planning

Simplified retirement advice: Key to overcoming behavioural biases, experts say

In a bid to enhance retirement outcomes for Australians, a recent whitepaper by Industry Fund Services, in collaboration with Challenger, has highlighted the importance of simplifying retirement ...Read more

Retirement Planning

Rest launches Retire Ready digital experience to empower members approaching retirement

Rest, one of Australia’s largest profit-to-member superannuation funds, has unveiled a new digital experience aimed at making retirement preparation simpler and more personalised for its members. Read more

Retirement Planning

New Framework Aims to Bridge Australia’s Financial Advice Gap

A ground-breaking framework introduced by the Actuaries Institute promises to revolutionise how Australians access financial support, potentially transforming the financial wellbeing of millionsRead more

Retirement Planning

The downsizer dividend: how Australia’s ageing shift will reshape property, finance and AI strategy

Downsizing is moving from a personal milestone to a system-level lever for Australia’s housing market. As policymakers court reforms and agents eye fresh listings, the real profit pools will accrue to ...Read more