Invest

How to save thousands on home renovations

By smartly managing cash flow, a $40,000 kitchen renovation could cost just $33,300.

How to save thousands on home renovations

By smartly managing cash flow, a $40,000 kitchen renovation could cost just $33,300.

If our passion for television show The Block is anything to go by, Australians like to renovate (or watch other people renovate). Many of my clients are joining an army of renovators and I can sympathise as my wife and I have just completed a kitchen renovation while expecting our second child.

If you are wanting to make some serious changes to your house, what is the best strategy?

Borrow to build

While many people borrow money to renovate, it can increase non-deductible debt. Renovations on your home are not tax deductible. For example, if you were to re-draw $40,000 against your home loan at current interest rates of around 4.50 per cent and assuming there are 16 years left on your principle and interest home loan, the interest and principle loan repayments will total $56,185 and your $40,000 kitchen renovation will actually cost $56,185.

Save your pennies

You could save $40,000 and start your kitchen renovation when you have the cash. This is the obvious option but for many people it means having to wait quite some time to be able to save the necessary amount.

Use a loan offset account

The third option, and the one that I’ve gone with, is keeping my cash in my home loan offset account and taking advantage of the interest-free purchase plans offered by some kitchen manufacturers and appliance retailers.

I have the cash saved for a renovation through good budgeting and control of my cash flow using an automated budget software tracking program.

How does this work? For example, the kitchen manufacturer will provide a $30,000 interest-free loan with monthly repayments of $833 over 36 months. This does cost $540 more per month than borrowing money from a bank but it does result in an additional $30,000 sitting in the offset account.

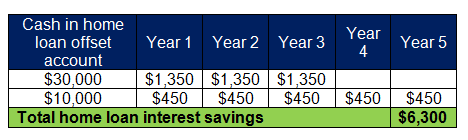

The appliance retailer will provide 50 months’ interest free with nothing payable until the end of the 50 months. Knowing that the monthly repayments can comfortably be paid to the kitchen manufacturer, having the $40,000 sitting in your offset account will save $6,300 in interest over the next five years assuming a constant interest rate of 4.50 per cent on an interest-only home loan.

At the end of the three years, all of the payments to the kitchen manufacturer are finished and after five years there is cash sitting there ready to pay the appliance retailer. There is still $30,000 cash available for something else.

To make this work, you need the discipline not to spend the $40,000 on something else, but it does mean that a $40,000 kitchen renovation is now costing $33,300 by smartly managing cash flow. It’s a nice balance to have the kitchen renovation now but still have a large cash buffer on hand. If need be, the cash can be used to pay the suppliers at any point in time.

Things you need to be aware of include missing a monthly payment or not paying out the amount in full at the end of the interest-free period. This will often result in high interest rates being applied to the balance due (up to 20 per cent interest rates). There may be penalties for early repayment and obtaining interest-free finance may restrict your capacity for other loan applications. You need to make sure you read the terms and conditions of the interest-free finance agreement. Also, some suppliers do provide a discount if you pay upfront in cash. Keep that in mind too.

To conclude, any home renovation involves a large commitment of money and time. Having a disciplined approach to how you manage your cash to fund a renovation, combined with the right use of loan products and purchase offers from suppliers, can achieve a smart financial result. For me, the above approach means we have more cash in our offset account against our home loan saving non-deductible interest repayments. We still have access to cash in case of an emergency.

The above strategies use these financial tools (interest-free purchase plans and offset accounts) to your advantage. Using financial tools such as interest-free purchase options on their own often ends in financial disaster for consumers. Ultimately, applying financial discipline and having a clear strategy will achieve better financial outcomes.

Andrew Zbik, senior financial planner, Omniwealth

RELATED ARTICLES

About the author

About the author

Property

Multigenerational living is moving mainstream: how agents, developers and lenders can monetise the shift

Australia’s quiet housing revolution is no longer a niche lifestyle choice; it’s a structural shift in demand that will reward property businesses prepared to redesign product, pricing and ...Read more

Property

Prestige property, precision choice: a case study in selecting the right agent when millions are at stake

In Australia’s top-tier housing market, the wrong agent choice can quietly erase six figures from a sale. Privacy protocols, discreet buyer networks and data-savvy marketing have become the new ...Read more

Property

From ‘ugly’ to alpha: Turning outdated Australian homes into high‑yield assets

In a tight listings market, outdated properties aren’t dead weight—they’re mispriced optionality. Agencies and vendors that industrialise light‑touch refurbishment, behavioural marketing and ...Read more

Property

The 2026 Investor Playbook: Rental Tailwinds, City Divergence and the Tech-Led Operations Advantage

Rental income looks set to do the heavy lifting for investors in 2026, but not every capital city will move in lockstep. Industry veteran John McGrath tips a stronger rental year and a Melbourne ...Read more

Property

Prestige property, precision choice: Data, discretion and regulation now decide million‑dollar outcomes

In Australia’s prestige housing market, the selling agent is no longer a mere intermediary but a strategic supplier whose choices can shift outcomes by seven figures. The differentiators are no longer ...Read more

Property

The new battleground in housing: how first-home buyer policy is reshaping Australia’s entry-level market

Government-backed guarantees and stamp duty concessions have pushed fresh demand into the bottom of Australia’s price ladder, lifting values and compressing selling times in entry-level segmentsRead more

Property

Property 2026: Why measured moves will beat the market

In 2026, Australian property success will be won by investors who privilege resilience over velocity. The market is fragmenting by suburb and asset type, financing conditions remain tight, and ...Read more

Property

Entry-level property is winning: How first home buyer programs are reshaping demand, pricing power and strategy

Lower-priced homes are appreciating faster as government support channels demand into the entry tier. For developers, lenders and marketers, this is not a blip—it’s a structural reweighting of demand ...Read more

Property

Multigenerational living is moving mainstream: how agents, developers and lenders can monetise the shift

Australia’s quiet housing revolution is no longer a niche lifestyle choice; it’s a structural shift in demand that will reward property businesses prepared to redesign product, pricing and ...Read more

Property

Prestige property, precision choice: a case study in selecting the right agent when millions are at stake

In Australia’s top-tier housing market, the wrong agent choice can quietly erase six figures from a sale. Privacy protocols, discreet buyer networks and data-savvy marketing have become the new ...Read more

Property

From ‘ugly’ to alpha: Turning outdated Australian homes into high‑yield assets

In a tight listings market, outdated properties aren’t dead weight—they’re mispriced optionality. Agencies and vendors that industrialise light‑touch refurbishment, behavioural marketing and ...Read more

Property

The 2026 Investor Playbook: Rental Tailwinds, City Divergence and the Tech-Led Operations Advantage

Rental income looks set to do the heavy lifting for investors in 2026, but not every capital city will move in lockstep. Industry veteran John McGrath tips a stronger rental year and a Melbourne ...Read more

Property

Prestige property, precision choice: Data, discretion and regulation now decide million‑dollar outcomes

In Australia’s prestige housing market, the selling agent is no longer a mere intermediary but a strategic supplier whose choices can shift outcomes by seven figures. The differentiators are no longer ...Read more

Property

The new battleground in housing: how first-home buyer policy is reshaping Australia’s entry-level market

Government-backed guarantees and stamp duty concessions have pushed fresh demand into the bottom of Australia’s price ladder, lifting values and compressing selling times in entry-level segmentsRead more

Property

Property 2026: Why measured moves will beat the market

In 2026, Australian property success will be won by investors who privilege resilience over velocity. The market is fragmenting by suburb and asset type, financing conditions remain tight, and ...Read more

Property

Entry-level property is winning: How first home buyer programs are reshaping demand, pricing power and strategy

Lower-priced homes are appreciating faster as government support channels demand into the entry tier. For developers, lenders and marketers, this is not a blip—it’s a structural reweighting of demand ...Read more