Invest

What's next for Chinese tech?

The entrepreneurial vision in China along with state-backed funding has led to one of the fastest growing and vibrant start up scenes in the world, rivaled only by that of Silicon Valley.

What's next for Chinese tech?

The entrepreneurial vision in China along with state-backed funding has led to one of the fastest growing and vibrant start up scenes in the world, rivaled only by that of Silicon Valley.

China's tech sector, under the government initiatives of “Internet Plus”, “Made in China 2025”, and “Outline on the National Information Technology Development Strategy”, is emerging as an innovation and technology powerhouse.

Year-to-date, however, the Chinese tech sector has significantly underperformed its US counterpart. At the beginning of the year, the biggest issue weighing on Chinese equities was the government’s financial de-risking campaign and quasi fiscal moderation. In order to try and de-risk its economy, China has been on strict path to deleverage, with stricter financial regulation and rules to curb shadow banking and misallocation of capital to non-productive areas of the economy. Add to this trade frictions, slowing economic growth, tightening US monetary policy, and a stronger dollar, and we see a perfect storm in Chinese equity markets that has sent them into a tailspin since the beginning of the year.

As economic data began to cool off and miss estimates, the Chinese government pre-empted a growth slowdown and stepped in in to ensure economic growth was not compromised. A double-barreled fiscal and monetary easing campaign has been enacted. There have already been three reserve ratio requirement cuts this year (with more expected), record medium-term lending facility liquidity injections, and a fiscal stimulus package including 65 billion yuan in tax cuts, expanding the preferential policy for small firms to all firms plus an infrastructure spending package all aimed at boosting domestic demand.

All this signals a policy shift towards easing, which is likely to support growth momentum in China for the time being – something that markets may be underestimating at the moment. Although the policy efforts introduced so far do not amount to broad-based easing as seen in 2009, these measures should not be underestimated.

The valuation of Chinese tech has been extreme relative to the US. As the graph below shows, historically a basket of Chinese tech companies trade at a valuation premium to US tech when comparing P/E ratios due to stellar growth. Now that actual growth is no longer meeting expectations, we are seeing a repricing across the sector as a whole. The market is revaluing Chinese tech stocks based on a slowing growth trajectory rather than a structural problem within the sector. For example, Tencent shares fell 6.67 per cent in the US after reporting weaker than expected numbers but it is still one of the fastest-growing technology companies in the world, as Saxo Bank head of equity strategy Peter Garnry recently pointed out.

Valuations have corrected significantly within the Chinese tech sector and the A-shares market. The valuation premium for Chinese tech is now the lowest since 2012 (see above graph), which may present an opportunity for long-term investors. As Mr Garnry notes, it’s often when others hesitate that one should act. When China’s stimulus begins to halt the weakness, the market will likely reprice the A-shares market as there remains attractive opportunities and even more so now at the current low valuation compared to developed markets.

Overall, the Chinese technology sector remains exciting in the longer term. The ecosystem contains a variety of interesting businesses with significant opportunities with the ability to drive growth and increase profitability for investors. Demographic shifts, with the rapid rise of the Chinese middle class and a burgeoning economy, have unleashed a wave of consumer engagement in China resulting in a decade of hyper-digitisation from which the tech sector can benefit from.

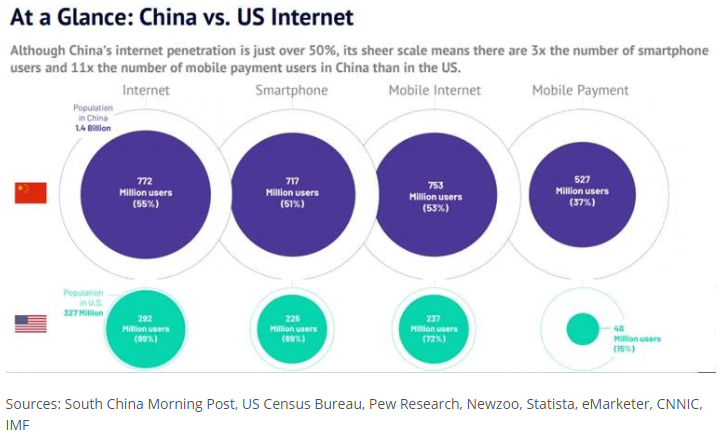

According to the China Internet Network Information Center, China’s online user base has increased to 800 million as at August 2018, double the population of the US – and it still has room to grow. According to Internet World Stats, only 54.6 per cent of the population in China is online compared with 89 per cent in the US.

We expect internet penetration and sector revenues to continue rising in the coming years due to the following:

1. China has a similar proportion of city dwellers as the US did in 1940 with a population approximately five times the size of the US, illustrating that there are still decades of above-average growth and urbanisation to come.

2. According to McKinsey & Company, China’s mobile payments ecosystem is already 11 times larger than the US; as these trends continue to emerge it will be critical for Chinese consumers to be online.

Besides the three tech gaints – Baidu, Alibaba, and Tencent – there is an abundance of technology companies listed on Chinese, Hong Kong and US exchanges who benefit from state support due to Beijing's plans for the Chinese economy as well as demographic trends in the country. But despite government support, these firms operate with entrepreneurial drive in what Baidu's chief scientist described as a “permanent state of war”, driving consistent growth within China’s tech sector.

Top Chinese tech stocks by market capitalisation

Alibaba Group Holding

Tencent Holdings

Baidu Inc.

Hangzhou Hikvision Digital Tec

Netease Inc.

360 Security technology Inc.

Iqiyi Inc.

Hanergy Thin Film Power Group

Focus Media Information technology

Weibo Corp

Eleanor Creagh is Australian markets strategist at Saxo Bank.

RELATED ARTICLES

Investment insights

Financial markets focus on shareholder engagement as companies report results

In a week dominated by financial market developments and corporate announcements, companies are increasingly recognising the importance of shareholder engagement in driving market outcomesRead more

Investment insights

Future Generation Australia declares increased dividend amid strong investment performance

Future Generation Australia (ASX: FGX) has announced a significant outperformance against the S&P/ASX All Ordinaries Accumulation Index, reporting a 14.1% increase in its 12-month investment ...Read more

Investment insights

New business landscape shifts as regional areas and company setups gain traction

The latest data from the January 2026 Lawpath New Business Index reveals a dynamic shift in how Australians are choosing to embark on new business ventures. While the overall number of new Australian ...Read more

Investment insights

Good Return secures $1 million investment from Macquarie Group Foundation to boost women-led enterprises

In a significant development for women-led enterprises across the Asia-Pacific region, Good Return has announced a $1 million investment from the Macquarie Group Foundation into its Impact Investment ...Read more

Investment insights

Beyond the trophy: what the REB Awards 2026 reveal about real estate’s next competitive play

Nearly 900 submissions for just over 30 winning slots is more than a celebration—it’s a market signal. In Australia’s roughly $10 trillion residential property market, awards have become a strategic ...Read more

Investment insights

Parents are funding know‑how, not deposits: A case study in Australia’s new first‑home playbook

With listings tight and auctions unforgiving, a quiet shift is underway: parents are increasingly paying for professional buying expertise instead of topping up deposits. This case study unpacks the ...Read more

Investment insights

State Street Markets reveals a shift in investor risk appetite amid economic uncertainties

In a recent revelation by State Street Markets, the latest State Street Institutional Investor Indicators have showcased a notable shift in investor behaviour as uncertainty looms over global ...Read more

Investment insights

UniSuper welcomes back seasoned strategist Mark Himpoo as Senior Portfolio Manager

In a strategic move aimed at bolstering its in-house investment capabilities, UniSuper has announced the return of Mark Himpoo as Senior Portfolio Manager, Equities. Himpoo's return marks a ...Read more

Investment insights

Financial markets focus on shareholder engagement as companies report results

In a week dominated by financial market developments and corporate announcements, companies are increasingly recognising the importance of shareholder engagement in driving market outcomesRead more

Investment insights

Future Generation Australia declares increased dividend amid strong investment performance

Future Generation Australia (ASX: FGX) has announced a significant outperformance against the S&P/ASX All Ordinaries Accumulation Index, reporting a 14.1% increase in its 12-month investment ...Read more

Investment insights

New business landscape shifts as regional areas and company setups gain traction

The latest data from the January 2026 Lawpath New Business Index reveals a dynamic shift in how Australians are choosing to embark on new business ventures. While the overall number of new Australian ...Read more

Investment insights

Good Return secures $1 million investment from Macquarie Group Foundation to boost women-led enterprises

In a significant development for women-led enterprises across the Asia-Pacific region, Good Return has announced a $1 million investment from the Macquarie Group Foundation into its Impact Investment ...Read more

Investment insights

Beyond the trophy: what the REB Awards 2026 reveal about real estate’s next competitive play

Nearly 900 submissions for just over 30 winning slots is more than a celebration—it’s a market signal. In Australia’s roughly $10 trillion residential property market, awards have become a strategic ...Read more

Investment insights

Parents are funding know‑how, not deposits: A case study in Australia’s new first‑home playbook

With listings tight and auctions unforgiving, a quiet shift is underway: parents are increasingly paying for professional buying expertise instead of topping up deposits. This case study unpacks the ...Read more

Investment insights

State Street Markets reveals a shift in investor risk appetite amid economic uncertainties

In a recent revelation by State Street Markets, the latest State Street Institutional Investor Indicators have showcased a notable shift in investor behaviour as uncertainty looms over global ...Read more

Investment insights

UniSuper welcomes back seasoned strategist Mark Himpoo as Senior Portfolio Manager

In a strategic move aimed at bolstering its in-house investment capabilities, UniSuper has announced the return of Mark Himpoo as Senior Portfolio Manager, Equities. Himpoo's return marks a ...Read more