Invest

The secret asset class bigger than super

Appetite for alternative defensive allocations continues to grow as investors seek new ways to preserve capital and generate stable income.

The secret asset class bigger than super

Appetite for alternative defensive allocations continues to grow as investors seek new ways to preserve capital and generate stable income.

This is supported by a number of factors, such as the current low interest rate environment resulting in low absolute yields, as well as recent increases in public market volatility. Coupled with this, is the general acknowledgement that fixed income return drivers have changed and inflation concerns are increasing. These factors combine to create a compelling backdrop for investors to consider allocations to the Australian private debt sector.

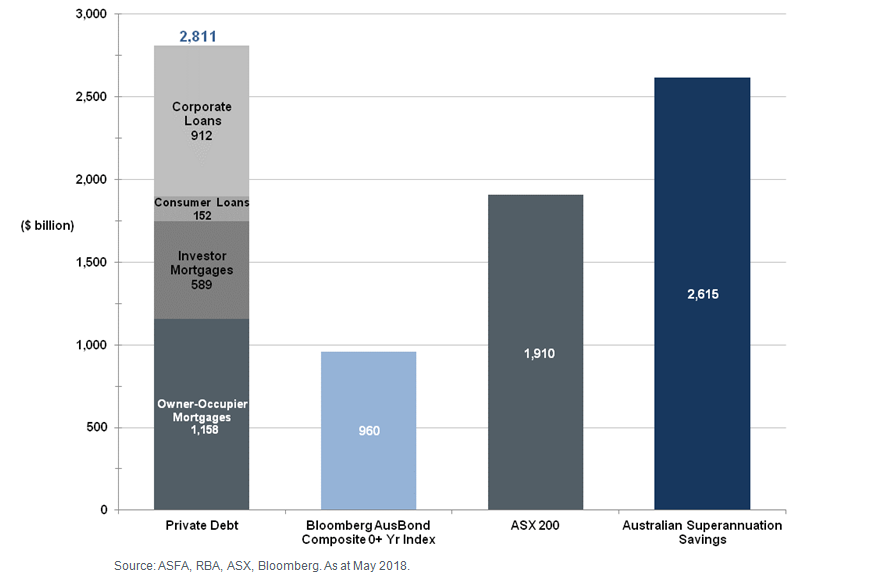

Private debt investments (or direct lending) involve the sourcing and managing of loan portfolios that help to fill the current financing gap created by the long-term decline in lending by Australian banks to Australian businesses. Australian private debt is not a new asset class, nor is it a small one. At over $2.8 trillion[1], it is larger than each of the Bloomberg AusBond Composite Index, the S&P/ASX200 Index and the Australian superannuation savings pool, and has been growing at a compound annual growth rate (CAGR) of 7.6 per cent[2] since 2003. The new and evolving aspect of Australian and New Zealand private debt is the ability for institutional investors and high-net-worth individuals to access a larger portion of this market that historically has been the domain of banks.

Relative size of the Australian private debt market – $2.8 trillion

Access to this market has traditionally been limited

Access to this market has traditionally been limited

Despite its relative size, Australian private debt has not experienced the same degree of institutional participation as has been experienced in other markets. The Australian private debt market has largely been dominated by domestic and to a lesser extent, offshore banks. Thus far, Australia’s largest banks have traditionally held a significant proportion of the private debt market on their own balance sheets and financed this with a combination of deposits and issuance of their bonds in domestic and global markets. In this way, the private debt market has almost been entirely intermediated by the big four Australian banks, with the only meaningful way for institutional investors to gain exposure to this space being through the purchase of bank issued bonds – which is an indirect and leveraged exposure.

Why is it gaining popularity now?

There are permanent structural and regulatory changes already underway in Australia that are leading to this current situation changing rapidly. Overseas in the US and Europe, private debt markets are much more accessible with a great deal of competition, about 90 per cent of the market participation is institutional. The local private debt market is expected to follow the lead of other developed offshore markets and open up a significant opportunity for domestic institutional and high-net-worth investors.

The effect of key announcements by APRA (Prudential Standard APS 120 Securitisation – announced in 2016 and came into force on 1 January 2018) have had significant impact on the four Australian banks. Given approximately two-thirds of the big four banks’ balance sheets are composed of mortgages, there has been a dramatic increase in the capital required to support this activity. This has had the effect of ‘starving’ other areas of capital required to support lending activities, attracting higher capital charges due to the rationing of a finite capital base.

As a result of these regulatory changes there is now a significant opportunity in the Australian private debt market, where the banks have been forced to retreat and where institutional investors have emerged to fill the void.

The most attractive sub-sectors

In looking at the spectrum of what is included in the private debt universe, the most attractive sub-sectors (identified against the current market backdrop) include leveraged buyout and private company debt (examples include Primo Smallgoods, Ticketek and Boost Juice), private and public asset-backed securities (ABS) and loans to stabilised commercial real estate assets. The relative attraction of these sub-sectors is driven by numerous factors, such as their size and the relative value on offer.

What role does it play in portfolio construction?

From a portfolio construction perspective, Australian and New Zealand private debt exhibits several compelling characteristics. Most notably, it is not correlated to traditional asset classes and offers true portfolio diversification – offering investors exposure to sub-sectors, industries and companies that are not generally accessible, and provides diversification away from financial sector risk (where portfolios may have exposure through shares, hybrids and corporate credit).

Being floating rate and largely illiquid, private debt also exhibits lower volatility and stable returns, which results in a superior Sharpe ratio when incorporated into a portfolio of Australian equities and fixed income. Importantly, quarterly or monthly (in the case of ABS) coupons, provide portfolios with regular income streams, while their floating rate nature provides protection from inflation and future interest rate increases.

As the Australian private debt investment universe is large with low levels of institutional investor participation, and with certain sub-sectors offering strong relative value, it is an asset class that will continue evolving and gaining investor interest.

Bob Sahota is chief investment officer at Revolution Asset Management.

[1] Reserve Bank of Australia (RBA).

[2] Reserve Bank of Australia (RBA).

RELATED ARTICLES

Investment insights

Financial markets focus on shareholder engagement as companies report results

In a week dominated by financial market developments and corporate announcements, companies are increasingly recognising the importance of shareholder engagement in driving market outcomesRead more

Investment insights

Future Generation Australia declares increased dividend amid strong investment performance

Future Generation Australia (ASX: FGX) has announced a significant outperformance against the S&P/ASX All Ordinaries Accumulation Index, reporting a 14.1% increase in its 12-month investment ...Read more

Investment insights

New business landscape shifts as regional areas and company setups gain traction

The latest data from the January 2026 Lawpath New Business Index reveals a dynamic shift in how Australians are choosing to embark on new business ventures. While the overall number of new Australian ...Read more

Investment insights

Good Return secures $1 million investment from Macquarie Group Foundation to boost women-led enterprises

In a significant development for women-led enterprises across the Asia-Pacific region, Good Return has announced a $1 million investment from the Macquarie Group Foundation into its Impact Investment ...Read more

Investment insights

Beyond the trophy: what the REB Awards 2026 reveal about real estate’s next competitive play

Nearly 900 submissions for just over 30 winning slots is more than a celebration—it’s a market signal. In Australia’s roughly $10 trillion residential property market, awards have become a strategic ...Read more

Investment insights

Parents are funding know‑how, not deposits: A case study in Australia’s new first‑home playbook

With listings tight and auctions unforgiving, a quiet shift is underway: parents are increasingly paying for professional buying expertise instead of topping up deposits. This case study unpacks the ...Read more

Investment insights

State Street Markets reveals a shift in investor risk appetite amid economic uncertainties

In a recent revelation by State Street Markets, the latest State Street Institutional Investor Indicators have showcased a notable shift in investor behaviour as uncertainty looms over global ...Read more

Investment insights

UniSuper welcomes back seasoned strategist Mark Himpoo as Senior Portfolio Manager

In a strategic move aimed at bolstering its in-house investment capabilities, UniSuper has announced the return of Mark Himpoo as Senior Portfolio Manager, Equities. Himpoo's return marks a ...Read more

Investment insights

Financial markets focus on shareholder engagement as companies report results

In a week dominated by financial market developments and corporate announcements, companies are increasingly recognising the importance of shareholder engagement in driving market outcomesRead more

Investment insights

Future Generation Australia declares increased dividend amid strong investment performance

Future Generation Australia (ASX: FGX) has announced a significant outperformance against the S&P/ASX All Ordinaries Accumulation Index, reporting a 14.1% increase in its 12-month investment ...Read more

Investment insights

New business landscape shifts as regional areas and company setups gain traction

The latest data from the January 2026 Lawpath New Business Index reveals a dynamic shift in how Australians are choosing to embark on new business ventures. While the overall number of new Australian ...Read more

Investment insights

Good Return secures $1 million investment from Macquarie Group Foundation to boost women-led enterprises

In a significant development for women-led enterprises across the Asia-Pacific region, Good Return has announced a $1 million investment from the Macquarie Group Foundation into its Impact Investment ...Read more

Investment insights

Beyond the trophy: what the REB Awards 2026 reveal about real estate’s next competitive play

Nearly 900 submissions for just over 30 winning slots is more than a celebration—it’s a market signal. In Australia’s roughly $10 trillion residential property market, awards have become a strategic ...Read more

Investment insights

Parents are funding know‑how, not deposits: A case study in Australia’s new first‑home playbook

With listings tight and auctions unforgiving, a quiet shift is underway: parents are increasingly paying for professional buying expertise instead of topping up deposits. This case study unpacks the ...Read more

Investment insights

State Street Markets reveals a shift in investor risk appetite amid economic uncertainties

In a recent revelation by State Street Markets, the latest State Street Institutional Investor Indicators have showcased a notable shift in investor behaviour as uncertainty looms over global ...Read more

Investment insights

UniSuper welcomes back seasoned strategist Mark Himpoo as Senior Portfolio Manager

In a strategic move aimed at bolstering its in-house investment capabilities, UniSuper has announced the return of Mark Himpoo as Senior Portfolio Manager, Equities. Himpoo's return marks a ...Read more