Invest

Price and yield: an inverse relationship for bonds

Fixed income is a major asset class which attracts numerous investors for a multitude of reasons, but understanding the relationship between a bond's price and its yield can be difficult for many. Richard Murphy from XTB explains how the two work and what a change in yield actually means.

Price and yield: an inverse relationship for bonds

Fixed income is a major asset class which attracts numerous investors for a multitude of reasons, but understanding the relationship between a bond's price and its yield can be difficult for many. Richard Murphy from XTB explains how the two work and what a change in yield actually means.

Rising share prices and property values make for happy investors. An increase in interest rates results in higher term deposit rates and again, investors are pleased. An increase in bond yields, however, can often leave investors confused and uncertain about the impact on their bond investments. So let’s look at the relationship between bond yields and prices.

The price is right

There are two components to be aware of when you buy a bond – its price and its yield.

When an investor buys a bond, they’re effectively making a loan to that government or corporation. In return for borrowing the investor’s capital, the bond is repaid in a specified time period and, for the duration of the loan, the investor is rewarded with regular coupon (or interest) payments.

Coupons are set with regard to the prevailing interest rates at the time, and for corporate bonds, the yield (or the amount an investor should realise on the bond) is generally higher than the cash rate.

This makes the bond a more attractive investment than a term deposit.

If you buy a bond at issue and hold it through to maturity, the investment will not be affected by changes to interest rates. As illustrated in Figure 1, coupon payments remain the same for the duration of the investment, and at maturity, the principal investment is repaid.

Figure 1: A bond bought at issue and held to maturity

Interest rates and bond prices

A buy and hold strategy is straightforward. However, if you wish to buy (or sell) a bond on the secondary market (i.e. after it has been issued), the relationship between the bond’s price and its yield becomes important.

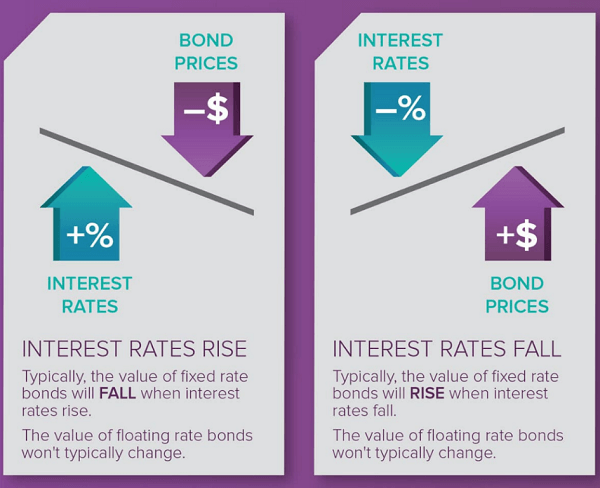

This relationship is sometimes depicted as a see-saw – as one rises, the other falls. As illustrated in Figure 2, the two factors have an inverse relationship; in other words, a bond’s price moves in the opposite direction of its yield.

This is no different to dividend yields on shares. If a $1 share pays a 5 cent dividend, then its dividend yield is 5 per cent. If the share price rises to $2, then the dividend yield for a 5 cent dividend becomes 2.5 per cent. Price and yield move in opposite directions.

Figure 2: the effect of interest rates on bond yields and bond prices

The price of a bond reflects the value today of the income it provides via regular coupon or interest payments and the repayment of the principal. When interest rates fall, bonds are still paying the same coupon rate, so they become more valuable and will generally trade at a higher price.

When interest rates rise, new term deposits and bonds issued after the rise will start paying investors higher rates than existing older bonds that are still paying the same coupon rate. Therefore the price of older bonds will generally fall.

How does this work in practice?

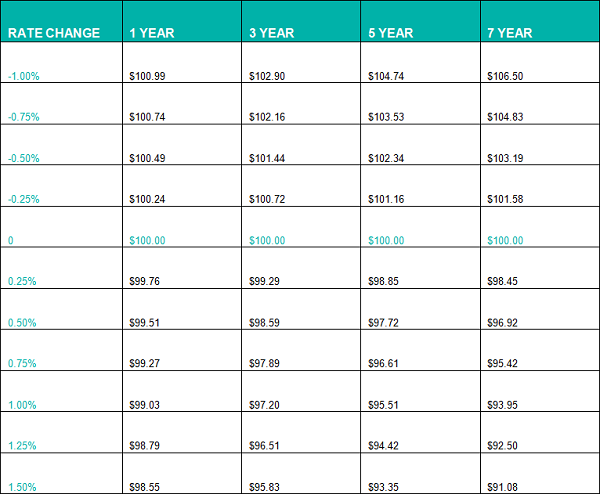

What is important to note is that fixed rate bonds are sensitive to changes in interest rates, while floating rate bonds do not have the same sensitivity. However, while equities and hybrid investments can move up or down by 5 per cent or more, senior corporate bonds from well-capitalised and creditworthy ASX top 100 listed companies are not as volatile, unless interest rates move very dramatically.

The following table shows the price sensitivity of $100 Face Value bond units on ASX for a given interest rate change. It shows that long-dated corporate bonds are more sensitive to interest rate changes than short-dated ones (using data on exchange traded bond units, or XTBs).

In summary

While changes in interest rates may be a cause for concern for bondholders if they don’t hold to maturity, bonds do not exhibit the high levels of volatility seen in equities markets. Therefore corporate bonds remain a good source of both income and capital stability for investors seeking more defensive investments.

Richard Murphy is the co-founder and chief executive officer of XTB, a company which specialises in exchange-traded bonds.

RELATED ARTICLES

Investment insights

State Street Markets reveals a shift in investor risk appetite amid economic uncertainties

In a recent revelation by State Street Markets, the latest State Street Institutional Investor Indicators have showcased a notable shift in investor behaviour as uncertainty looms over global ...Read more

Investment insights

UniSuper welcomes back seasoned strategist Mark Himpoo as Senior Portfolio Manager

In a strategic move aimed at bolstering its in-house investment capabilities, UniSuper has announced the return of Mark Himpoo as Senior Portfolio Manager, Equities. Himpoo's return marks a ...Read more

Investment insights

Global M&A deal value surges 31% in 2025 as focus shifts to supply chain resilience

In a significant upswing, global mergers and acquisitions (M&A) deals reached an impressive $3 trillion in 2025, marking a 31% increase from the previous year. This surge was largely driven by a ...Read more

Investment insights

Emerging trends in wealth management: APAC leads the way in AI and diversification

In a rapidly evolving financial landscape, wealth managers across the Asia-Pacific (APAC) region are spearheading significant shifts in investment strategies, according to the latest "Emerging Trends ...Read more

Investment insights

Gold investment rockets in 2025, setting a new high as uncertainty bites

In a year marked by economic and geopolitical turbulence, gold investment reached unprecedented heights, according to the World Gold Council's Full-Year 2025 Gold Demand Trends report. The report, ...Read more

Investment insights

RBC Capital Markets and BMO Capital Markets lead 2025 M&A advisory in metals & mining sector

In a significant development within the metals and mining sector, RBC Capital Markets and BMO Capital Markets have emerged as the leading financial advisers for mergers and acquisitions (M&A) ...Read more

Investment insights

Orbis highlights key investment questions for 2026

Global markets have kicked off 2026 with a positive momentum carried over from last year, but Orbis Investments warns that investors should tread carefully. With valuations becoming increasingly ...Read more

Investment insights

APAC deal activity down by 3% in 2025 as China and India offset broader decline

The Asia-Pacific (APAC) region witnessed a moderation in deal activity in 2025, with a 3% decline in the total number of deals announced compared to the previous year. This downturn, encompassing ...Read more

Investment insights

State Street Markets reveals a shift in investor risk appetite amid economic uncertainties

In a recent revelation by State Street Markets, the latest State Street Institutional Investor Indicators have showcased a notable shift in investor behaviour as uncertainty looms over global ...Read more

Investment insights

UniSuper welcomes back seasoned strategist Mark Himpoo as Senior Portfolio Manager

In a strategic move aimed at bolstering its in-house investment capabilities, UniSuper has announced the return of Mark Himpoo as Senior Portfolio Manager, Equities. Himpoo's return marks a ...Read more

Investment insights

Global M&A deal value surges 31% in 2025 as focus shifts to supply chain resilience

In a significant upswing, global mergers and acquisitions (M&A) deals reached an impressive $3 trillion in 2025, marking a 31% increase from the previous year. This surge was largely driven by a ...Read more

Investment insights

Emerging trends in wealth management: APAC leads the way in AI and diversification

In a rapidly evolving financial landscape, wealth managers across the Asia-Pacific (APAC) region are spearheading significant shifts in investment strategies, according to the latest "Emerging Trends ...Read more

Investment insights

Gold investment rockets in 2025, setting a new high as uncertainty bites

In a year marked by economic and geopolitical turbulence, gold investment reached unprecedented heights, according to the World Gold Council's Full-Year 2025 Gold Demand Trends report. The report, ...Read more

Investment insights

RBC Capital Markets and BMO Capital Markets lead 2025 M&A advisory in metals & mining sector

In a significant development within the metals and mining sector, RBC Capital Markets and BMO Capital Markets have emerged as the leading financial advisers for mergers and acquisitions (M&A) ...Read more

Investment insights

Orbis highlights key investment questions for 2026

Global markets have kicked off 2026 with a positive momentum carried over from last year, but Orbis Investments warns that investors should tread carefully. With valuations becoming increasingly ...Read more

Investment insights

APAC deal activity down by 3% in 2025 as China and India offset broader decline

The Asia-Pacific (APAC) region witnessed a moderation in deal activity in 2025, with a 3% decline in the total number of deals announced compared to the previous year. This downturn, encompassing ...Read more