Invest

Exploring the Commonwealth Bank's performance

Though the Commonwealth Bank is facing a civil suit over a number of compliance breaches, its share price is unlikely to be affected. In this piece, John Abernethy explores the drivers behind the bank's performance over the past few years - Brought to you by Clime Asset Management.

Exploring the Commonwealth Bank's performance

Though the Commonwealth Bank is facing a civil suit over a number of compliance breaches, its share price is unlikely to be affected. In this piece, John Abernethy explores the drivers behind the bank's performance over the past few years - Brought to you by Clime Asset Management.

The revelations that the Commonwealth Bank of Australia (CBA) is being taken to court over alleged AUSTRAC reporting and compliance breaches will overshadow its annual result this week.

The action is a civil one and a massive penalty is likely. However, the monetary penalty is unlikely to affect the CBA share price. For instance, a theoretical but massive $1 billion fine is a mere 1/140th of the bank’s market capitalisation and would represent just 1.5 per cent of shareholder equity. Based on the 2017 financial year (FY17) reported net profit of $9.9 billion, it could be paid from bank pre-tax earnings in just one month!

Therefore the CBA’s intrinsic valuation will be hardly affected by this event but it may soon become clear that the premium rating by the market for CBA compared to its Australian peers (WBC, ANZ and NAB) must be challenged.

The CBA board released a statement whereby it wiped out short-term incentives that may have been payable to key executives for FY17 and declared it will reduce non-executive board fees by 20 per cent in FY18. While this is noble, it hardly addresses the damage done to the reputation of the bank. Further, the “give up” by directors and executives will be dwarfed by the fine that will be borne by shareholders.

The CBA board has noted the “risk and reputational issues” that are flowing from the alleged AUSTRAC reporting contraventions. This is important for CBA shareholders to understand because the relative rating of CBA shares on the stock market has consistently been at a premium to its peers. This premium is reflected in a higher multiple of its share price to its net tangible assets (NTA) per share.

This rating also reflects years of superior performance in terms of the return on shareholders’ equity.

Despite this premium rating, it has not resulted in a superior share price performance by CBA over the last three years. Indeed, the share price today is exactly the same as it was in August 2014. The big banks have been affected by a range of headwinds, but have all benefited from a surge in household debt that has helped grow their balance sheets and profits.

Figure 1. CBA Share price, 2012 – current

Source. ASX

CBA has seen a noticeable decline in normalised return on equity, from 29.8 per cent to 21.5 per cent, over five years. This is a measure of profitability and so while profits are rising, the profitability is falling.

This is important because it is profitability that mainly determines the multiple of equity (or NTA per share) that a company’s shares trade at.

To illustrate this point more clearly, we focus on the incremental returns coming from retained or raised equity. Over the last five years, CBA has grown equity by $18 billion (from $42 billion to $60 billion) and lifted earnings by $1.8 billion (from $7.6 billion to $9.4 billion).

The incremental return is thus averaging 10 per cent, or 15 per cent adjusted for franking credits.

The incremental returns on equity for CBA are falling and this has dragged down the overall return on equity. While this is concerning, the decline is actually more acute because of the massive amount of hybrid equity raised over the last five years.

These $5 billion of hybrid raisings have helped CBA (and all major banks) to meet the more stringent risk-adjusted capital ratio requirements set by APRA. However, while it is adding to tier 1 capital, it is generating a low return for the banks after the servicing of dividends to the hybrid owners.

While CBA is an exceptional bank, it has clearly benefited (like all the Australian banks) from an extraordinarily prolonged period of sustained economic growth, significant household debt creation and arguably lax capital regulation.

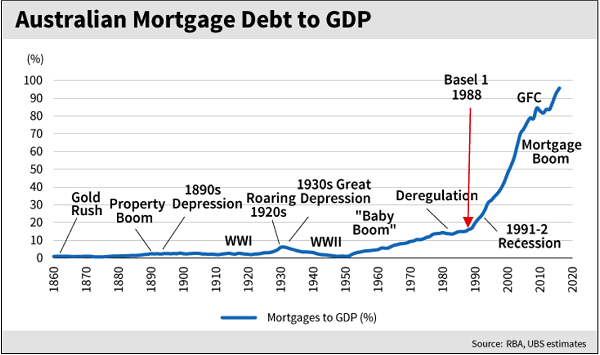

The sustained growth period has meant that the last 20 years have been a benign period for bad debts for Australian banks. This remarkable period of super-charged debt creation is shown in the following chart.

The banks grew their mortgage loan books funded by cheap deposits and equity grown via a range of hybrid capital raisings that super-charged the returns on ordinary equity. Arguably, there was no better bank at achieving this outcome than CBA.

Figure 2. Australian Mortgage Debt to GDP (%)

Source. RBA, UBS estimates

The growth in bank balance sheets over the last 20 years directly reflects the growth in household leverage; it is well documented that today, over 80 per cent of new loans written by banks are mortgage debt related.

It seems that the CBA (like its peers) has taken on the appearance of large building societies. They have done so with an excessive focus on asset growth that clearly benefited executive bonus payments.

After a long period of excessive market price to intrinsic value observations, we now see the share price correctly reflecting the lower return on equity. Subject to further negative news flow, CBA shares will start to look interesting at about $76 (ex dividend) or at a 10 per cent discount to 2018 value.

Why the discount?

We believe that the years of frantic loan growth and under-capitalised balance sheets are behind CBA. However, these same observations hold true for all the major banks.

So while the CBA has created its own unique set of problems, we perceive that slower asset growth, lower ROEs and higher retained earnings will be a common feature of all banks in the next few years.

What is unknown is the work-through of the excessive level of household debt that prevails across the Australian economy and within bank balance sheets. So long as bad debts don’t rise, the banks will drift through this cycle; but any significant lift in interest rates or unexpected “black swan” international event could have serious consequences. Indeed, more serious than those proposed for senior CBA executives.

John Abernethy is the managing director and chief investment officer of the Clime Group.

RELATED ARTICLES

Investment insights

Payday Super could prompt a wave of business sales in Australia

As Australian small business owners brace for the introduction of Payday Super on 1 July 2026, industry experts are sounding alarms about the potential impact on the nation's business landscapeRead more

Investment insights

Value stocks back in favour as federal budget bolsters income investing

The recent federal budget, coupled with shifting macroeconomic conditions, is casting a spotlight on the appeal of value stocks and income-generating businesses. This trend is being observed as a ...Read more

Investment insights

A fortnight of flux: Australian investors brace for economic shifts and corporate updates

The past fortnight has been marked by a whirlwind of developments in the financial markets, with investor attention riveted on both domestic and international fronts. From the looming tax policy ...Read more

Investment insights

Shifting global conditions and policy changes shape Australian investment landscape

In a series of events held across Australia last week, Shadforth Financial Group's annual State of the Nation gatherings brought together industry experts to discuss the evolving investment ...Read more

Investment insights

European start-ups demand faster funding and reduced red tape amid new Chips Act proposal

As the European Commission prepares to unveil its Chips Act II proposal on May 27, the spotlight turns to the challenges faced by European start-ups in the semiconductor and deep tech sectorsRead more

Investment insights

New business registrations rise in April, but GST drop points to more cautious founders

In a testament to the enduring entrepreneurial spirit in Australia, new business registrations surged in April 2026, marking a 6.41% increase compared to the same period last year. According to the ...Read more

Investment insights

Investors face mixed outcomes in latest budget, say industry leaders

In the wake of the recent budget announcements, industry leaders from Spaceship Financial Services and eToro Australia have expressed their views on the implications for investors, highlighting a mix ...Read more

Investment insights

Changes to CGT rules spark concern among Australian startup founders

The recent announcement of changes to the Capital Gains Tax (CGT) in the 2026-27 budget has sent ripples of concern through Australia's startup community. Founders and investors alike are expressing ...Read more

Investment insights

Payday Super could prompt a wave of business sales in Australia

As Australian small business owners brace for the introduction of Payday Super on 1 July 2026, industry experts are sounding alarms about the potential impact on the nation's business landscapeRead more

Investment insights

Value stocks back in favour as federal budget bolsters income investing

The recent federal budget, coupled with shifting macroeconomic conditions, is casting a spotlight on the appeal of value stocks and income-generating businesses. This trend is being observed as a ...Read more

Investment insights

A fortnight of flux: Australian investors brace for economic shifts and corporate updates

The past fortnight has been marked by a whirlwind of developments in the financial markets, with investor attention riveted on both domestic and international fronts. From the looming tax policy ...Read more

Investment insights

Shifting global conditions and policy changes shape Australian investment landscape

In a series of events held across Australia last week, Shadforth Financial Group's annual State of the Nation gatherings brought together industry experts to discuss the evolving investment ...Read more

Investment insights

European start-ups demand faster funding and reduced red tape amid new Chips Act proposal

As the European Commission prepares to unveil its Chips Act II proposal on May 27, the spotlight turns to the challenges faced by European start-ups in the semiconductor and deep tech sectorsRead more

Investment insights

New business registrations rise in April, but GST drop points to more cautious founders

In a testament to the enduring entrepreneurial spirit in Australia, new business registrations surged in April 2026, marking a 6.41% increase compared to the same period last year. According to the ...Read more

Investment insights

Investors face mixed outcomes in latest budget, say industry leaders

In the wake of the recent budget announcements, industry leaders from Spaceship Financial Services and eToro Australia have expressed their views on the implications for investors, highlighting a mix ...Read more

Investment insights

Changes to CGT rules spark concern among Australian startup founders

The recent announcement of changes to the Capital Gains Tax (CGT) in the 2026-27 budget has sent ripples of concern through Australia's startup community. Founders and investors alike are expressing ...Read more