Invest

Dividends in Australian shares – is the COVID lockdown lifting?

What happened during reporting season? Andrew Zenonos asks.

Dividends in Australian shares – is the COVID lockdown lifting?

In many ways, FY20 reporting season was one of the most closely watched in recent memory as investors attempted to understand the true impact of the COVID-19 pandemic on company fundamentals. Going into the end of the financial year, expectations for earnings had been slashed significantly due to the level of uncertainty that remained in the outlook for the economy. While there was stock level volatility and divergence (as always), reporting season for FY20 was largely better than expected though FY21 earnings expectations were downgraded; the ASX 300 returned 3.05 per cent for the month of August.

Although results were better than expected at the aggregate level, many companies did not give guidance for FY21 due to the uncertainty that still looms over the next 12 months in the economy. Companies may provide updates during AGMs in Q4; however, it is difficult to know if additional clarity will be available at that point in time.

There were some notable themes at the sector level. The consumer discretionary sector was a notable space for earnings upgrades as the “work from home” theme drove strong increases in sales. JB Hi-Fi and Harvey Norman were beneficiaries of this, outperforming by 9.5 per cent and 15.8 per cent, respectively, through August. While bank results were mostly in line with expectations, FY21 earnings for the sector was downgraded on the back of net interest margin pressures, as well as uncertainty for the economy once fiscal stimulus has ended or is tapered significantly. Resources companies remain resilient and reported earnings upgrades in aggregate; iron ore miners remain well bid as the commodity market dynamics remain favourable.

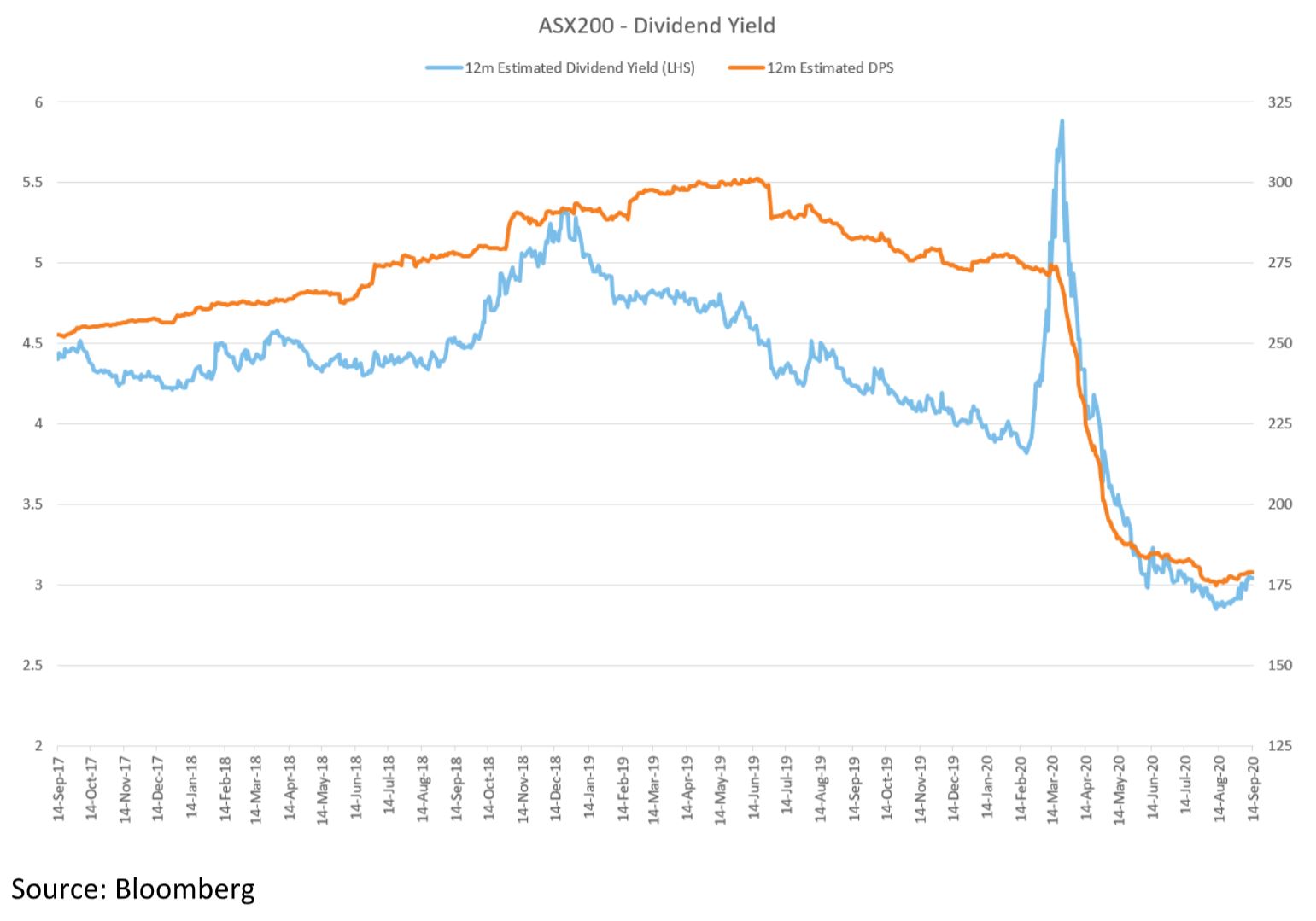

What happened to dividend expectations?

Due to the level of uncertainty that remains for the coming 12 months and the hesitation from companies to give guidance, it is not surprising that we did not see much in terms of news flow around dividends relative to expectations. At the end of July, APRA eased restrictions around paying dividends for banks however payout ratios for authorised deposit-taking institutions (ADIs) will be maintained below 50 per cent for this year. While this is a small positive, the outlook for bank dividends remains significantly below what investors have come to expect. ANZ, CBA and NAB announced dividends; however, Westpac confirmed that an interim dividend will not be paid. Once factoring in reporting season, approximately 35 per cent of companies in the ASX 200 have deferred, cancelled, suspended or declared no final dividend. The outlook for dividends at the aggregate market level remains subdued and shrouded in uncertainty, i.e. not dissimilar to the environment before reporting season. In saying that, however, alongside the thematic that earnings were better than feared, it appears that the outlook for dividends has potentially seen a bottom – at least for now.

The expected dividend yield for the Australian market, which has historically been viewed as a high dividend yield market, is now around 3 per cent. This is significantly lower than the 20-year average dividend yield of 4.3 per cent.

How did our ETFs perform?

Through August, both our Russell Investments High Dividend Australian Shares ETF (RDV) and our Russell Investments Responsible Investment ETF (RARI) outperformed relative to the broad market.

RDV benefitted from exposure to retail and the “work from home” theme noted above via overweight positions in Harvey Norman and JB Hi-Fi. Exposure to a number of companies that reported “better than feared results also added value, particularly in tourism-related parts of the market. Star Entertainment and Flight Centre outperformed the broad market on the back of their results.

RARI also benefitted from exposure to strong retail names such as Super Retail group and Premier Investments, as well as “better than feared” results in Qantas and Stockland Group. Rio Tinto is excluded from RARI’s holdings due to its involvement in, and risk attributable to, mining activities. This benefited performance over the month of August, as controversy related to the company’s blasting of indigenous sites weighed on the share price. This caused significant shareholder backlash, and exposed some questionable, if not poor, governance practices within the company. Subsequently, the CEO and a number of senior executives have departed. We continue to see strong demand for ESG-related products and growing concern around active ownership and governance.

Andrew Zenonos is an associate portfolio manager, equity, at Russell Investments.

RELATED ARTICLES

Investment insights

Payday Super could prompt a wave of business sales in Australia

As Australian small business owners brace for the introduction of Payday Super on 1 July 2026, industry experts are sounding alarms about the potential impact on the nation's business landscapeRead more

Investment insights

Value stocks back in favour as federal budget bolsters income investing

The recent federal budget, coupled with shifting macroeconomic conditions, is casting a spotlight on the appeal of value stocks and income-generating businesses. This trend is being observed as a ...Read more

Investment insights

A fortnight of flux: Australian investors brace for economic shifts and corporate updates

The past fortnight has been marked by a whirlwind of developments in the financial markets, with investor attention riveted on both domestic and international fronts. From the looming tax policy ...Read more

Investment insights

Shifting global conditions and policy changes shape Australian investment landscape

In a series of events held across Australia last week, Shadforth Financial Group's annual State of the Nation gatherings brought together industry experts to discuss the evolving investment ...Read more

Investment insights

European start-ups demand faster funding and reduced red tape amid new Chips Act proposal

As the European Commission prepares to unveil its Chips Act II proposal on May 27, the spotlight turns to the challenges faced by European start-ups in the semiconductor and deep tech sectorsRead more

Investment insights

New business registrations rise in April, but GST drop points to more cautious founders

In a testament to the enduring entrepreneurial spirit in Australia, new business registrations surged in April 2026, marking a 6.41% increase compared to the same period last year. According to the ...Read more

Investment insights

Investors face mixed outcomes in latest budget, say industry leaders

In the wake of the recent budget announcements, industry leaders from Spaceship Financial Services and eToro Australia have expressed their views on the implications for investors, highlighting a mix ...Read more

Investment insights

Changes to CGT rules spark concern among Australian startup founders

The recent announcement of changes to the Capital Gains Tax (CGT) in the 2026-27 budget has sent ripples of concern through Australia's startup community. Founders and investors alike are expressing ...Read more

Investment insights

Payday Super could prompt a wave of business sales in Australia

As Australian small business owners brace for the introduction of Payday Super on 1 July 2026, industry experts are sounding alarms about the potential impact on the nation's business landscapeRead more

Investment insights

Value stocks back in favour as federal budget bolsters income investing

The recent federal budget, coupled with shifting macroeconomic conditions, is casting a spotlight on the appeal of value stocks and income-generating businesses. This trend is being observed as a ...Read more

Investment insights

A fortnight of flux: Australian investors brace for economic shifts and corporate updates

The past fortnight has been marked by a whirlwind of developments in the financial markets, with investor attention riveted on both domestic and international fronts. From the looming tax policy ...Read more

Investment insights

Shifting global conditions and policy changes shape Australian investment landscape

In a series of events held across Australia last week, Shadforth Financial Group's annual State of the Nation gatherings brought together industry experts to discuss the evolving investment ...Read more

Investment insights

European start-ups demand faster funding and reduced red tape amid new Chips Act proposal

As the European Commission prepares to unveil its Chips Act II proposal on May 27, the spotlight turns to the challenges faced by European start-ups in the semiconductor and deep tech sectorsRead more

Investment insights

New business registrations rise in April, but GST drop points to more cautious founders

In a testament to the enduring entrepreneurial spirit in Australia, new business registrations surged in April 2026, marking a 6.41% increase compared to the same period last year. According to the ...Read more

Investment insights

Investors face mixed outcomes in latest budget, say industry leaders

In the wake of the recent budget announcements, industry leaders from Spaceship Financial Services and eToro Australia have expressed their views on the implications for investors, highlighting a mix ...Read more

Investment insights

Changes to CGT rules spark concern among Australian startup founders

The recent announcement of changes to the Capital Gains Tax (CGT) in the 2026-27 budget has sent ripples of concern through Australia's startup community. Founders and investors alike are expressing ...Read more