Retirement

First home buyers using super may not be a scandalous idea

Given the ongoing concerns about housing affordability, the reaction to speculation that the government may allow Australians to use superannuation monies as a first home deposit should come as no surprise.

First home buyers using super may not be a scandalous idea

Given the ongoing concerns about housing affordability, the reaction to speculation that the government may allow Australians to use superannuation monies as a first home deposit should come as no surprise.

There have been numerous critics, including a handful of thoroughly researched and no doubt well-meaning economic commentators, who have flagged the risks in the Australian housing market, including our sky-high private debt levels.

Former prime minister Paul Keating stated that the idea was scandalous, and that only a reckless government would put the superannuation system at risk with such a policy.

His view is vastly at odds with the position of the Labor Party under then Prime Minister Keating, when they said, “a debt-free home is as important a part of retirement security as superannuation income” with a policy proposal from the party that would “permit part of the deposit on owner-occupied dwellings to be funded from the home buyers’ superannuation account”.

Before delving into my thoughts on the subject, I want to make three quick points:

1) From the point of view of making housing more affordable, freeing up superannuation so first home buyers can use it for a deposit won’t work, as it will only add to demand, not supply.

2) Even if it were made possible, and I didn’t already have an SMSF, I wouldn’t dream of using my superannuation to buy property today, as I think the Australian residential property market as a whole is at best exceptionally expensive, at worst grossly overvalued, with a handful of downside risks ahead.

3) I think both superannuation and the Australian housing market are far too big these days and, as currently structured, hold back productive enterprise, growth and the economic wellbeing of Australians as a whole.

Despite the above, on balance I support the idea for a handful of reasons.

Housing is a critical component of any retirement plan

One of the key arguments against allowing Australians to use superannuation for a home deposit is that it will reduce the value of their portfolio, leaving them with a smaller pool of capital they can draw down on in retirement.

This is, of course, true but it also misses two key points.

The first is that by buying a home, the superannuant is not engaging in a form of conspicuous consumption that leaves them with nothing to show for it at the end of the day.

They are still investing in an asset, with many in reality trading share and fixed income exposure for direct property, with the money able to be returned to their fund in the event of a sale.

Just as importantly, we cannot have a credible conversation about the retirement needs of Australians without focusing on the importance of owning the roof over their head.

This much was made clear in the latest ASFA retirement standard update that suggested a retired couple wanting to live comfortably and who rented in Sydney would need more than $1.15 million in their superannuation fund. Couples that own their home would need only $640,000, placing non-home owning retirees “at a distinct financial disadvantage”, according to ASFA CEO Martin Fahy.

That circa $500,000 difference is substantial at the best of times, and is all the evidence we need to understand why we simply can’t ignore the importance of home ownership when discussing retirement outcomes.

Superannuation is already invested in housing

The current superannuation system strongly encourages young Australians to invest in growth funds, with healthy allocations to shares. The shares owned by these funds include a large weighting to Australian bank stocks, whose business models are built around lending to fund our housing market, with a heavy focus on investor home loans.

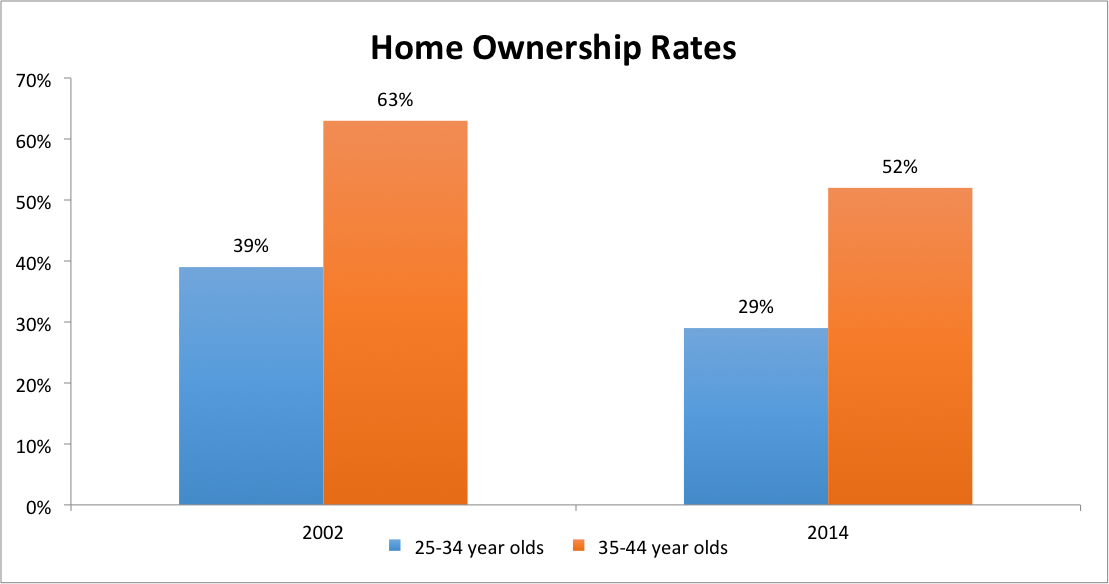

At the same time, the law also allows SMSF trustees to use their superannuation to invest in Australian residential housing directly, despite the fact that nearly 70 per cent of trustees already own their family home.

To put that 70 per cent in context, consider the chart below, which shows home ownership rates for 25-34 and 35-44 year olds, and what happened to them between 2002 and 2014.

Source: ABC Bullion, HILDA survey

If you really think superannuation monies shouldn’t be invested in housing, you could make an argument that given their housing-centric business models, retail and industry funds should reduce exposure to Australian banks, and SMSFs should be banned from investing in Australian residential property.

Note that I’m not advocating for that personally, but it should be obvious to anyone why the status quo is not fair in any way to young Australians, who today face record-low levels of wage growth and much higher rates of unemployment and underemployment, relative to the population as a whole.

At present, they are in effect banned from using their primary and fastest-growing financial asset as a deposit for a property, while being forced to fund the creation of home loans which help push housing prices even further beyond their reach.

Freedom, competition, innovation

By forcing Australians to consume compulsory superannuation, we are already, to some degree, limiting their financial freedom. Perhaps I’m showing my own libertarian bias here, but given this, surely it’s only fair that we give them maximum choice and freedom as to where that money is invested.

There are benefits on the competition front too, as opening a new and popular asset class to superannuation monies will put welcome pressure on existing fund managers and superannuation funds to improve their product offerings. After all, nobody is advocating that Australian superannuants be forced to invest their monies in Australian property. It will just be added to the product/asset class mix as it were.

Finally, we see considerable scope for innovation here. After all, Australians are required to put 9.5 per cent of their money into superannuation. Owning a family home is still the Australian dream for many, and as discussed earlier, a critical part of securing a comfortable retirement.

Given there are superannuation funds designed for specific and diverse target markets from tech-focused Millennials (spaceship) to vegans (cruelty-free super), is it really such a stretch to think that our superannuation funds, our banks and even our property developers might be able to come together to build innovative new products that target young Australians wanting to own their own family home?

I, for one, wouldn’t have thought so.

How safe is super anyway?

Another key argument against allowing younger Australians to access their superannuation for a home deposit is the potential risk in the residential property market now.

This is a risk I’m acutely aware of, having discussed it in a recent publication where we discussed the warning signs, “including the circa 10 per cent price declines seen in the Perth residential market in the last few years, the record levels of supply coming to the market on the east coast, and the uptick in vacancy rates we’re seeing in parts of the country”.

But it has to be noted that the average young Australian invested in growth superannuation funds already has their money at risk, and would likely see a serious fall in the value of their portfolio should our housing market decline meaningfully.

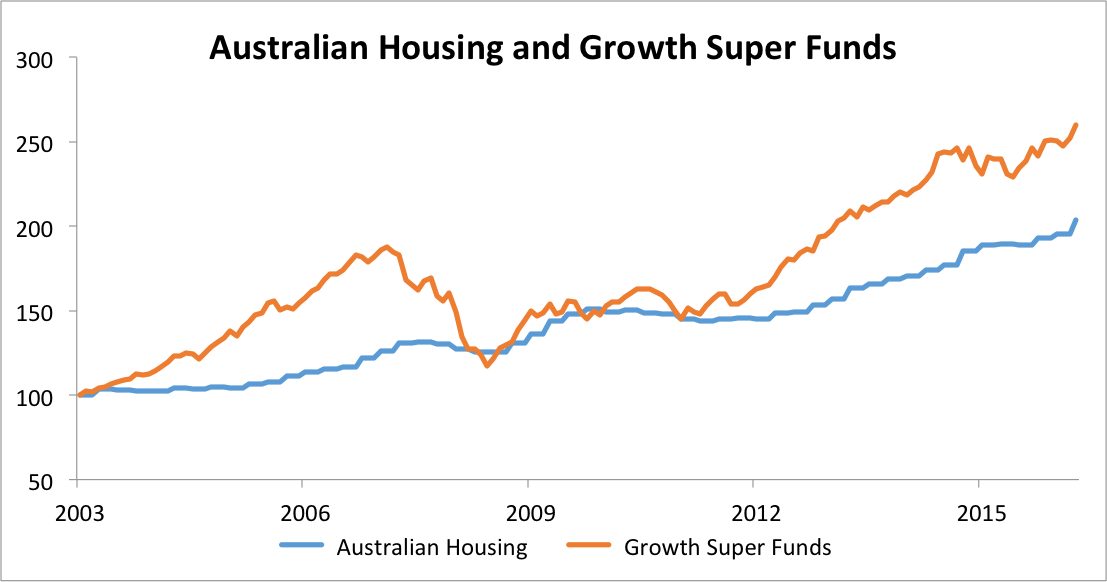

To give some context to this risk, consider the chart below, which shows returns for both Australian residential housing and growth superannuation funds going back to 2003, with both investments re-based to 100 for comparison promises.

Source: ABC Bullion, Australian Bureau of Statistics, Super Ratings SR25 High Growth

As you can see, there was a precipitous fall in the value of growth superannuation funds during the GFC, with a peak to trough drawdown of some 38 per cent between October 2007 and February 2009.

Young Australians investing in these funds did not recover their monies until July 2013, while property prices have continued on their primary uptrend for this entire period, despite the small decline suffered during the GFC.

That was then, this is now, one might argue, and while I would agree that Australian housing is on balance now a riskier investment proposition than it was 10 to 15 years ago, I’m not at all convinced the average growth fund is any safer today than it was back then.

After all, the vast majority of these portfolios are still invested in Australian and international equities, two asset classes that face no shortage of challenges in the years ahead.

If we look at international equities, using the S&P 500 as a proxy, the market is at best fully priced, if not outright expensive. This is based on a broad range of indicators, including cyclically adjusted price to earnings ratios, total market capitalisation to GDP, and Tobin’s Q ratio. Analyst Doug Short publishes a regular average of four valuation indicators for the S&P 500, with his March 2017 update suggesting they are some 84 per cent (no, that is not a misprint) above their long run averages.

The research team at 720 Global, who look at valuations and fundamentals (including GDP and productivity growth, government deficits, debt levels, earnings growth, etc) are even more concerned, with their analysis suggesting the market has not been this expensive since the 1930s.

While not all markets are expensive as the United States, it is still difficult to envisage investors achieving a positive overall return from international equities should the S&P 500 go through another major correction, given the weighting to US stocks in any global equity benchmark, and the correlation of developed market equity returns in this post-GFC environment.

On the domestic front, there is cause for concern too, especially with a local bourse dominated by financial stocks, including our banks, whose primary business is funding Australian residential home loans, as we discussed before.

During Australia’s last recession, bank dividends were cut by close to 35 per cent, with share prices falling across the board too. When the GFC hit, banks cut their dividends by over 20 per cent, while the value of their shares fell by closer to 50 per cent in some cases.

These brutal declines occurred despite the fact that the Australian residential housing market suffered a decline of less than 5 per cent during the GFC, with the overall economy continuing to grow.

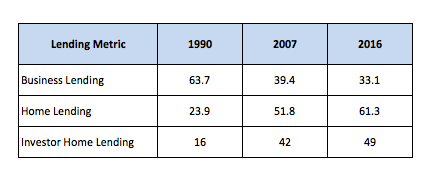

Now consider the table below, which plots the lending profiles for our banks at three points across the last quarter century.

Australian bank lending profiles (percentage of total loans)

Source: ABC Bullion, Reserve Bank of Australia, Australian Bureau of Statistics

As you can see, home loans now comprise more than 60 per cent of total loans, a number that is circa 10 per cent higher than when the GFC hit, and nearly 40 per cent higher than the situation back in the 1990s.

Loans to housing investors have tripled over the past 25 years.

It is painfully clear that Australian banks are far more exposed to Australian housing than they were both when the GFC hit, and especially relative to when our last recession struck. As such, I can’t help but worry about what might happen to these stocks were there to be a severe housing market downturn in the near future.

The bottom line here is simple. If you think our housing market is a high-risk investment today (an assertion I’d agree with fully), then so are our major banks, and therefore so too is the ASX and most growth superannuation funds younger Australians are steered toward with their compulsory 9.5 per cent contributions.

Frying pan or fire – take your pick.

Summary

On affordability grounds alone, the idea of allowing Australians to use their superannuation for a house deposit would almost certainly be a failure. From a competition, engagement, innovation and freedom perspective, and from the point of view of social utility, it is definitely a win.

From a risk perspective, given the way superannuation money in growth funds is currently invested, I’d say it’s a toss of the coin, with the risk in both strategies undoubtedly high in the coming years.

As such, while it would be no panacea for our housing affordability crisis, and while I think there are a number of other more important policy changes the government and superannuation industry should look at, allowing young Australians to use their compulsory superannuation contributions for a housing deposit is not as scandalous as it might first appear.

Jordan Eliseo, chief economist, ABC Bullion

RELATED ARTICLES

Superannuation

Rest strengthens digital engagement with new leadership appointment

In a significant move to enhance its digital member services, Rest, one of Australia's largest profit-to-member superannuation funds, has appointed Darran Arnott as General Manager, DigitalRead more

Superannuation

Aware Super earns adviser-ready fund accreditation under new national framework

In a significant development for the financial advice sector, Aware Super has been awarded the prestigious Adviser-Ready Fund accreditation. This recognition comes under a new national framework ...Read more

Superannuation

Superannuation overhaul: Payday Super set to enhance retirement savings for millions

In a significant shift set to impact the retirement savings of millions of Australians, the way superannuation contributions are paid is about to undergo a major overhaul. However, despite the ...Read more

Superannuation

Rest expands retail property portfolio with US$250 million investment in US real estate fund

Rest, one of Australia's largest profit-to-member superannuation funds, has announced a substantial investment in a US-based real estate fund, marking a strategic expansion of its retail property ...Read more

Superannuation

TelstraSuper and Aware Super merger advances with key agreement

In a significant development for the Australian superannuation sector, TelstraSuper and Aware Super have reached a pivotal milestone in their merger journey by signing the Successor Fund Transfer ...Read more

Superannuation

Rest applauds legislative reforms to boost superannuation for low-income earners

In a landmark move, Rest has expressed strong approval following the successful passage of legislation aimed at enhancing the Low Income Superannuation Tax Offset (LISTO) through ParliamentRead more

Superannuation

Rest promotes Rachel O’Connor to head fixed income team

In a significant move within Australia's superannuation sector, Rest, one of the largest profit-to-member funds in the country, has announced the promotion of Rachel O'Connor to lead its Fixed Income ...Read more

Superannuation

Employment Hero raises concerns over superannuation bill's impact on small businesses

Employment Hero has raised significant concerns regarding the implementation of the proposed Supporting Choice in Superannuation and Other Measures Bill, which was recently recommended for passage by ...Read more

Superannuation

Rest strengthens digital engagement with new leadership appointment

In a significant move to enhance its digital member services, Rest, one of Australia's largest profit-to-member superannuation funds, has appointed Darran Arnott as General Manager, DigitalRead more

Superannuation

Aware Super earns adviser-ready fund accreditation under new national framework

In a significant development for the financial advice sector, Aware Super has been awarded the prestigious Adviser-Ready Fund accreditation. This recognition comes under a new national framework ...Read more

Superannuation

Superannuation overhaul: Payday Super set to enhance retirement savings for millions

In a significant shift set to impact the retirement savings of millions of Australians, the way superannuation contributions are paid is about to undergo a major overhaul. However, despite the ...Read more

Superannuation

Rest expands retail property portfolio with US$250 million investment in US real estate fund

Rest, one of Australia's largest profit-to-member superannuation funds, has announced a substantial investment in a US-based real estate fund, marking a strategic expansion of its retail property ...Read more

Superannuation

TelstraSuper and Aware Super merger advances with key agreement

In a significant development for the Australian superannuation sector, TelstraSuper and Aware Super have reached a pivotal milestone in their merger journey by signing the Successor Fund Transfer ...Read more

Superannuation

Rest applauds legislative reforms to boost superannuation for low-income earners

In a landmark move, Rest has expressed strong approval following the successful passage of legislation aimed at enhancing the Low Income Superannuation Tax Offset (LISTO) through ParliamentRead more

Superannuation

Rest promotes Rachel O’Connor to head fixed income team

In a significant move within Australia's superannuation sector, Rest, one of the largest profit-to-member funds in the country, has announced the promotion of Rachel O'Connor to lead its Fixed Income ...Read more

Superannuation

Employment Hero raises concerns over superannuation bill's impact on small businesses

Employment Hero has raised significant concerns regarding the implementation of the proposed Supporting Choice in Superannuation and Other Measures Bill, which was recently recommended for passage by ...Read more