Resources

One simple way to add stability to your portfolio

Promoted by XTB.

Share markets are volatile. This brings opportunities, but also risks, and can leave you vulnerable to unpredictable market conditions. Having a stable, defensive core to your portfolio helps diversify and protect your wealth.

One simple way to add stability to your portfolio

Promoted by XTB.

Share markets are volatile. This brings opportunities, but also risks, and can leave you vulnerable to unpredictable market conditions. Having a stable, defensive core to your portfolio helps diversify and protect your wealth.

In uncertain times portfolio construction is more important than ever

Read on if you’re:

- Retired and want to protect the wealth you’ve built

- Have an SMSF you want to be more diversified

- Concerned about share market ups and downs

- Looking for a regular, predictable source of income from your investments

- Interested in trading 5 XTBs brokerage-free

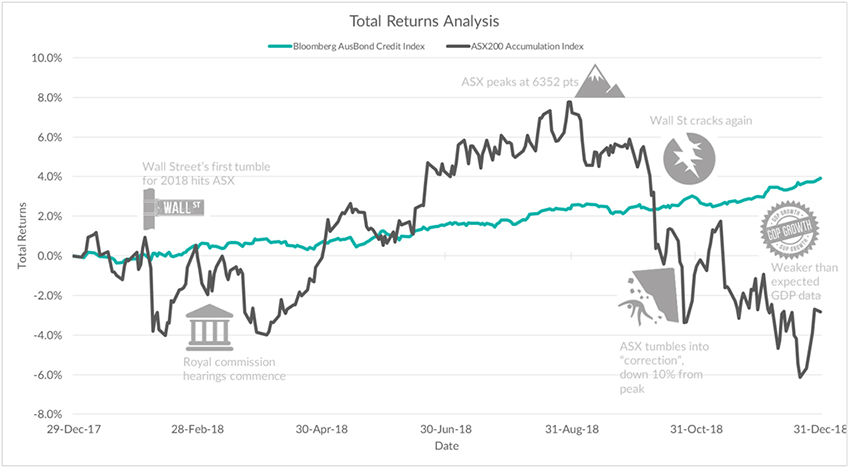

2018 was a bumpy year for shares. The Australian benchmark index the S&P/ASX200®finished down approximately 2.8% including dividends, 6.9% excluding them.

The main drivers of the downturn were geopolitical events, especially the threat of trade wars and rising US interest rates. The decline from September onwards effectively wiped out the year’s gains. A portfolio heavily weighted to growth-style stocks would have likely lost money. On the flip side, while corporate bonds suffered some losses the Bloomberg AusBond Credit Index finished up almost 4%.

Bonds help you sleep, whereas shares can cause restless nights

Corporate bonds were largely unaffected by the numerous events that impacted shares. When the share market seems to be going up and up, it’s easy to overlook the cushioning effect of a solid fixed income foundation. But, in volatile times it’s increasingly important to ensure you protect the wealth you’ve built up.

Investors with balanced portfolios (50:50 bonds and shares), may have found their share market losses balanced by their bond returns. It’s having a solid foundation of bonds that can help protect and stabilise most portfolios through volatile times.

A strong defence

Investment-grade bonds are a defensive asset class. The stability and diversification they can offer really shouldn’t be overlooked. With the prospect of more uncertainty ahead, defensive assets are increasingly on the radar of investors. So, now’s a good time to consider if they are right for you.

Corporate bonds – no longer just for the professionals

Corporate bonds have traditionally been popular among institutional investors. Most bonds are issued in $500,000 lots which means in the past, self-directed investors and SMSFs have largely been excluded.

But, that’s no longer the case. A broad range of bond ETFs and more than 50 different Exchange-Traded Bond units (XTBs), now provide access to the returns of bonds. All of them are available to trade on ASX.

Diversification and Simplification

Bond ETFs offer access to a very diverse range of bonds. They’ve helped open up access to bonds and are simple to buy and sell via ASX. But, there is one key feature that corporate bond XTBs have which ETFs don’t.

Let’s use a term deposit investment to illustrate this feature:

When you buy a term deposit, you know your return because you know the interest rate upfront AND when it matures (its end date). XTBs also have these ‘fixed’ features which provide you with comfort and predictability from day 1.

The downside of perpetuity

Bond ETFs are continual – they don’t have an end date. This means they can’t provide the same level of predictability of returns. Also, they are pooled products –new bonds are added or removed, sometimes on a daily basis and there could be hundreds of bonds included. That’s good for diversification, but perhaps more importantly, it means you don’t know what your return will be. It also means you lose the certainty of what you’ve invested in. Remember, knowing your cash flow before you invest is at the heart of fixed income.

Predictability of individual bonds

Another way to access the benefits of bonds which retains the core ‘fixed’ elements, is via XTBs (Exchange Traded Bond units). Just like ETFs, XTBs are also accessible on ASX, so can be bought and sold at visible prices at any time. But they have one key difference - each XTB mirrors a single, specific bond.

This means each XTB has two known features:

- The coupon amount and

- The maturity date when the face value of the bond is paid back (subject to no default by the bond issuer).

Retaining this one-to-one relationship of an XTB with its underlying bond keeps all of the ‘fixed’ or predictable elements. Just like in our Term Deposit example.

As with all ASX investments, you can invest as much or as little as you like with XTBs (starting from $500 with most brokers). So you can:

- Buy as many units as you wish, or cherry pick specific XTBs to deliver a specific cash flow,

- Pick an XTB which returns its face value on a specific date, or

- Select specific companies you know and trust.

Choosing exactly what you want to invest in keeps you in control, rather than leaving the decisions to a fund or ETF manager.

What about performance?

Fixed income is a defensive asset class, so you don’t expect it to deliver the same returns as your growth investments. However, it’s also important to make sure that all of your investments work as hard as they can for you.

By selecting specific individual corporate bond XTBs, it’s possible to out-perform major bond indices. In 2018, the key corporate bond index (AusBond Credit Index)returned close to 4%. Over this same period, a portfolio of 5 of the highest yielding XTBs delivered a total return of 5.5%.

Give XTBs a try with brokerage-free trading from Bell Direct

Complete the form to receive a pack of the income and returns available from a choice of XTB portfolios. And access a link to try XTBs brokerage-free with Bell Direct.

Find out more about XTBs

Web: https://xtbs.com.au/

Email:

Tel: 1800 995 993

Disclaimer: The information in this article is general in nature. It should not be the sole source of information. It does not take into account the investment objectives or circumstances of any particular investor. You should consider, with or without advice from a professional adviser, whether an investment is appropriate to your circumstances. Past performance is not a guarantee of future performance.

Terms of the Bell Direct free-brokerage offer

This special offer is open to Nest Egg readers who are new to Bell Direct. Joining Bell Direct is easy and all online. When your account is open, you can start trading XTBs straight away. The brokerage will be refunded on your first 5 XTB trades. Simply place your trades online before COB 30 June 2019. Brokerage will be refunded at the beginning of the month following the order being executed. If you are trading more than five XTBs, brokerage will apply to your subsequent trades.

RELATED ARTICLES

Sponsored features

Dissecting the Complexities of Cash Indices Regulations: An In-Depth Analysis

Introduction In recent years, the world of finance has seen a surge of interest in cash indices trading as investors seek potential returns in various markets. This development has brought increased ...Read more

Sponsored features

The Best Ways to Find the Right Trading Platform

Promoted by Animus Webs Read more

Sponsored features

How the increase in SMSF members benefits business owners

Promoted by ThinkTank Read more

Sponsored features

Thinktank’s evolution in residential lending and inaugural RMBS transaction

Promoted by Thinktank When Thinktank, a specialist commercial and residential property lender, recently closed its first residential mortgage-backed securitisation (RMBS) issue for $500 million, it ...Read more

Sponsored features

Investors tap into cyber space to grow their wealth

Promoted by Citi Group Combined, our daily spending adds up to opportunities for investors on a global scale. Read more

Sponsored features

Ecommerce boom as world adjusts to pandemic driven trends

Promoted by Citi Group COVID-19 has accelerated the use of technologies that help keep us connected, creating a virtual supply chain and expanded digital universe for investors. Read more

Sponsored features

Industrial property – the silver lining in the retail cloud

Promoted by ThinkTank Read more

Sponsored features

Why the non-bank sector appeals to SMSFs

Promoted by Think Tank Read more

Sponsored features

Dissecting the Complexities of Cash Indices Regulations: An In-Depth Analysis

Introduction In recent years, the world of finance has seen a surge of interest in cash indices trading as investors seek potential returns in various markets. This development has brought increased ...Read more

Sponsored features

The Best Ways to Find the Right Trading Platform

Promoted by Animus Webs Read more

Sponsored features

How the increase in SMSF members benefits business owners

Promoted by ThinkTank Read more

Sponsored features

Thinktank’s evolution in residential lending and inaugural RMBS transaction

Promoted by Thinktank When Thinktank, a specialist commercial and residential property lender, recently closed its first residential mortgage-backed securitisation (RMBS) issue for $500 million, it ...Read more

Sponsored features

Investors tap into cyber space to grow their wealth

Promoted by Citi Group Combined, our daily spending adds up to opportunities for investors on a global scale. Read more

Sponsored features

Ecommerce boom as world adjusts to pandemic driven trends

Promoted by Citi Group COVID-19 has accelerated the use of technologies that help keep us connected, creating a virtual supply chain and expanded digital universe for investors. Read more

Sponsored features

Industrial property – the silver lining in the retail cloud

Promoted by ThinkTank Read more

Sponsored features

Why the non-bank sector appeals to SMSFs

Promoted by Think Tank Read more