Resources

Are the super changes affecting your retirement planning?

Promoted by Centuria Capital Limited.

![]()

If they’re not, maybe they should be, says Neil Rogan, General Manager of Investment Bonds for Centuria. Investment bonds can be a tax-effective alternative to super for those Australians affected by last year’s changes.

Are the super changes affecting your retirement planning?

Promoted by Centuria Capital Limited.

![]()

If they’re not, maybe they should be, says Neil Rogan, General Manager of Investment Bonds for Centuria. Investment bonds can be a tax-effective alternative to super for those Australians affected by last year’s changes.

Major changes to the superannuation rules came into effect in mid-2017, and by now, many SMSFs,as well as Australians earning higher salaries, will have either made changes or be considering their alternatives.

New limits to contributions

Concessional contributions (pre-tax contributions such as those from your employer) are now limited to $25,000 per annum, down from $35,000 – for people 49 years and older, and $30,000 – for everyone else. If you do make more than $25,000 in concessional contributions, you will pay an extra 15% tax.

It isalso no longer possible to make more than $100,000 per annum of non-concessional (after tax) contributions. This is a reduction from $180,000 per annum, although Australians under the age of 65 will still have the opportunity to bring forward two years of concessional contributions, up to $300,000 in a single financial year, again subject to other caps.

In addition, anyone with a total superannuation balance (made up of super, pensions and/or retirement savings accounts) of $1.6 million or more can no longer make any non-concessional contributions to super at all. This includes the bring-forward rule which allowed for larger non-concessional contributions in one year.

New limit on tax-free retirement account

In addition, you can only have a maximum of $1.6 million in the tax-free retirement phase pension account, whereas previously there was no limit on the amount you could hold in a tax-free pension account. Anyone with more than $1.6 million in the tax-free retirement phase will have had to either move the excess back into the accumulation phase (where it is taxed) or out of the super system altogether.

The bad news is that the limits to superannuation (both in terms of your ability to contribute and tax-effectiveness)mean that it is more important than ever to inform yourself about tax-effective investment strategies outside of super. The good news is that investment bonds could be the effective strategy you need to invest in for retirement and grow your wealth,particularly when you consider that marginal tax rates on personal income can be as high as 45% (plus a Medicare levy of 2%), and interest rates on cash deposits are at historical lows. It makes good financial sense to look at tax-effective investment options.

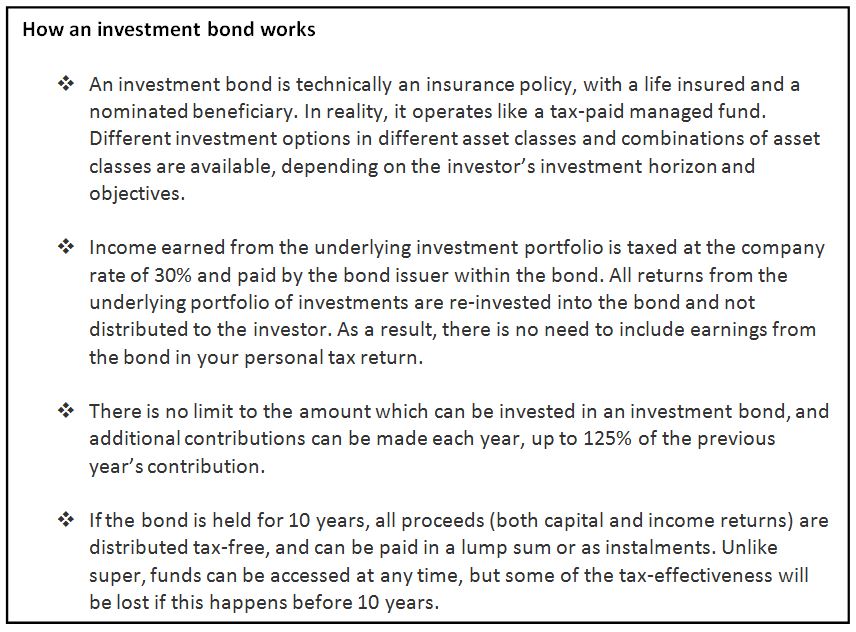

Investment bonds are simple and flexible, and offer investment options across a range of different asset classes and portfolio combinations. They are tax-free in the hands of the investor if held for 10 years, but funds can also be accessed at any time if required.

Investment bonds are a tax-effective, flexible option

- Returns from investments in the underlying portfolio are paid within the bond structure at the company rate of 30%. If the underlying portfolio contains equities with franking credits, the effective tax rate paid may be less.

- There is no personal tax payable on withdrawals made from the investment bond after the bond is held for 10 years.

- Returns during the life of the bond do not need to be included in your personal tax return, because investment returns are re-invested and not distributed.

- Investment bonds do not form part of your estate and may be left to a nominated beneficiary (or beneficiaries), who will receive all proceeds tax free on the death of the life insured.

- Investment bonds may offer protection from creditors in the case of bankruptcy.

- Investment bonds are quick and easy to set up.

- There is no limit on the initial investment amount in the first year, although additional investments must not exceed 125% of the prior year’s contribution for the 10-year rule to apply.

Conclusion

Changes to the superannuation system have already affected many Australians, changing their retirement plans and limiting their ability to use super as the most tax-effective means of long term saving. Looking forward, there’s no question that super will remain in the political spotlight, and any further changes are likely to make it less, rather than more, generous. With that in mind, it is a good time to talk to your adviser about the possibility of using investment bonds to complement your superannuation, or for any number of long term financial goals.

Please note this is general information and does not consider the circumstances of any individual. It is based on an understanding of current legislation, but no warranty if given for its accuracy. Any person intending to act on this information should seek the assistance of a professional adviser.

For more information contact Centuria on 1300 50 50 50 or visit our website to download the Centuria Investment Bonds PDS.

Disclaimer: Suitability of a Centuria Investment Bond will depend on a person’s circumstances, financial objectives and needs, none of which have been taken into consideration in preparing this document. Prospective investors should obtain and read a copy of the Product Disclosure Statement (PDS) for any investment bond and consider the information in the PDS in light of their circumstances, objectives and needs before making a decision to invest. This document is not an offer to invest in any of Centuria’s Investment Bonds. An investment in any of Centuria’s Investment Bonds is subject to risk and Centuria will receive fees in relation to the management of its Investment Bonds as detailed in the PDS. Issued by Centuria Life Limited ABN 79 087 649 054 AFSL 230867.

RELATED ARTICLES

Sponsored features

Dissecting the Complexities of Cash Indices Regulations: An In-Depth Analysis

Introduction In recent years, the world of finance has seen a surge of interest in cash indices trading as investors seek potential returns in various markets. This development has brought increased ...Read more

Sponsored features

The Best Ways to Find the Right Trading Platform

Promoted by Animus Webs Read more

Sponsored features

How the increase in SMSF members benefits business owners

Promoted by ThinkTank Read more

Sponsored features

Thinktank’s evolution in residential lending and inaugural RMBS transaction

Promoted by Thinktank When Thinktank, a specialist commercial and residential property lender, recently closed its first residential mortgage-backed securitisation (RMBS) issue for $500 million, it ...Read more

Sponsored features

Investors tap into cyber space to grow their wealth

Promoted by Citi Group Combined, our daily spending adds up to opportunities for investors on a global scale. Read more

Sponsored features

Ecommerce boom as world adjusts to pandemic driven trends

Promoted by Citi Group COVID-19 has accelerated the use of technologies that help keep us connected, creating a virtual supply chain and expanded digital universe for investors. Read more

Sponsored features

Industrial property – the silver lining in the retail cloud

Promoted by ThinkTank Read more

Sponsored features

Why the non-bank sector appeals to SMSFs

Promoted by Think Tank Read more

Sponsored features

Dissecting the Complexities of Cash Indices Regulations: An In-Depth Analysis

Introduction In recent years, the world of finance has seen a surge of interest in cash indices trading as investors seek potential returns in various markets. This development has brought increased ...Read more

Sponsored features

The Best Ways to Find the Right Trading Platform

Promoted by Animus Webs Read more

Sponsored features

How the increase in SMSF members benefits business owners

Promoted by ThinkTank Read more

Sponsored features

Thinktank’s evolution in residential lending and inaugural RMBS transaction

Promoted by Thinktank When Thinktank, a specialist commercial and residential property lender, recently closed its first residential mortgage-backed securitisation (RMBS) issue for $500 million, it ...Read more

Sponsored features

Investors tap into cyber space to grow their wealth

Promoted by Citi Group Combined, our daily spending adds up to opportunities for investors on a global scale. Read more

Sponsored features

Ecommerce boom as world adjusts to pandemic driven trends

Promoted by Citi Group COVID-19 has accelerated the use of technologies that help keep us connected, creating a virtual supply chain and expanded digital universe for investors. Read more

Sponsored features

Industrial property – the silver lining in the retail cloud

Promoted by ThinkTank Read more

Sponsored features

Why the non-bank sector appeals to SMSFs

Promoted by Think Tank Read more