Resources

New super structure prompts demand for alternative tax-effective investments

Resources

New super structure prompts demand for alternative tax-effective investments

Promoted by Centuria Capital Limited.

![]()

Recent changes to the superannuation system mean that what was once the most tax-effective savings system for all Australians is no longer so attractive to everyone. A raft of changes designed to stop the practice of using super for inter-generational wealth transfer and to ensure that it remains true to its purpose of helping Australians fund their own retirement, have seen some of the tax benefits lost.

New super structure prompts demand for alternative tax-effective investments

Promoted by Centuria Capital Limited.

![]()

Recent changes to the superannuation system mean that what was once the most tax-effective savings system for all Australians is no longer so attractive to everyone. A raft of changes designed to stop the practice of using super for inter-generational wealth transfer and to ensure that it remains true to its purpose of helping Australians fund their own retirement, have seen some of the tax benefits lost.

The major changes affecting super’s tax benefits are :

- Where previously there was no limit to the amount which could be held in a tax-free retirement account, there is now a maximum limit of $1.6 million, after which funds much be withdrawn from the super system, or transferred back into the accumulation phase to be taxed.

- Annual concessional (before tax) contributions to super are now limited to $25,000, down from $35,000. After this, tax of 30% rather than 15% will be charged.

- Annual non-concessional (after tax) contributions to super are limited to $100,000 per year, down from $180,000.

- Any Australian earning $250,000 or more pays an extra 15% tax (total of 30%) on all concessional contributions.

- Once your super balance reaches $1.6 million, no further contributions to super are allowed.

Potential for further changes

The Labor Party has put forward a different version of superannuation and contributions legislation, called its ‘Fairer Super Plan’. And debate,by politicians and social equity groups such as ACOSS, especially around the perceived generosity of super, will no doubt continue.

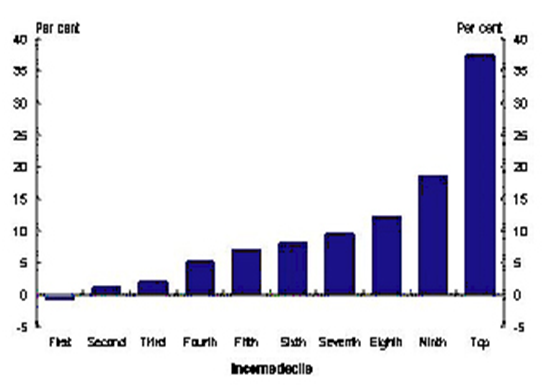

The most commonly-used data (from the Murray Report, as below), shows that about 38% of the tax advantages of super go to the top 10% of income earners. This will change under the new rules, but the shift will be slow.

Share of total superannuation tax concessions by decile

Source: Financial System Inquiry, Final Report, page 138

Investors seeking certainty and flexibility in a tax-effective environment will increasingly consider alternatives outside of super. There are various options that may assist in minimising or deferring tax – such as creating a private company to hold investments or forming a family trust – but for high-income earners, one of the more tax-effective, flexible, and cost-effective options, may be an investment bond.

Tax and flexibility of an investment bond

Investment bonds are technically life-insurance policies with a nominated life insured, and a beneficiary. In investment terms, they operate like a tax-paid managed fund. Investors choose from a range of investment options, depending on their goals. These range from growth portfolios (higher risk) which typically include more equities, to defensive portfolios (lower risk) which usually invest in cash and fixed interest.

An investment bond is tax-paid, because the earnings from the underlying investment portfolio are taxed at the company rate of 30% within the bond structure. Investors do not receive distributions as they are re-invested, and do not therefore need to declare the earnings from the bond in their personal tax returns. In the case of investment portfolios which contain equities, the tax rate may be further reduced by franking credits.

If an individual’s personal taxable income is at least $37,001 p.a. the tax paid on any additional personal income will be greater than on investment bond earnings rate. At this threshold, the marginal tax rate increases from 21% to 34.5%, higher than the 30% on investment bonds.

There is no limit to the amount which can be placed in an investment bond in the first year, and additional contributions can be made each year, at up to 125% of the previous year’s contribution.

Funds can be withdrawn at any time, however, if they are left in the investment bond structure for 10 years, the entire proceeds of the bond (original investment, additional contributions and earnings) are tax paid. The investor does not need to include them in their tax return, and they can be distributed as a lump sum, or as a tax-paid income over time. And because an investment bond is in fact an insurance policy, with a life insured (this can be the same person as the bond owner), on the death of the life insured, the beneficiary of the bond will receive all proceeds of the bond tax free, regardless of how long the bond has been held.

The proceeds fall outside of the bond owner’s estate, and pass directly to the beneficiary. This makes investment bonds ideal estate planning tools, or an effective way to transfer wealth from one generation to another.

Super remains the most tax-effective long-term investment structure for most Australians, but access to super money is restricted until a ‘condition of release’ is met. This generally means the investor can’t withdraw the money until they have reached a ‘preservation age’ and retired. Preservation age is 55 for an investor born before 1 July 1960 but increases up to age 60 for those born after this date. Earlier access may be allowed in exceptional circumstances, such as permanent disability.

Saving for education or estate planning purposes

By contrast, investment bonds can be used as savings for children or family members to fund education expenses or the cost of raising a child, and are often used by grandparents to finance the future needs of their grandchildren. The bonds bring simplicity in managing the tax that applies to a child’s income, and may be assigned to a child in the future (subject to parental or guardian consent) without tax or legal complications. The child has the option to continue holding the investment bond without affecting the original 10-year tax period start date.

An investment bond’s life insurance component enables tax-effective estate planning and simple wealth transfers external to a will. It gives the life insured significant flexibility and control in determining beneficiaries of any ‘death maturity’ payments.

In superannuation, death benefit tax concessions apply only to dependents of the life insured. However, an investment bond’s death benefits can be directed tax-free to any nominated beneficiary, including adult family members, or the estate. How long the bond has been held does not impact the tax-free status. This flexibility may reduce the risk of disputes over estates and enable benefits to be paid more quickly.

For more information about how investment bonds could form part of your investment strategy or to understand more about how they work and the options available, please contact Centuria on 1300 505 050

RELATED ARTICLES

Sponsored features

Dissecting the Complexities of Cash Indices Regulations: An In-Depth Analysis

Introduction In recent years, the world of finance has seen a surge of interest in cash indices trading as investors seek potential returns in various markets. This development has brought increased ...Read more

Sponsored features

The Best Ways to Find the Right Trading Platform

Promoted by Animus Webs Read more

Sponsored features

How the increase in SMSF members benefits business owners

Promoted by ThinkTank Read more

Sponsored features

Thinktank’s evolution in residential lending and inaugural RMBS transaction

Promoted by Thinktank When Thinktank, a specialist commercial and residential property lender, recently closed its first residential mortgage-backed securitisation (RMBS) issue for $500 million, it ...Read more

Sponsored features

Investors tap into cyber space to grow their wealth

Promoted by Citi Group Combined, our daily spending adds up to opportunities for investors on a global scale. Read more

Sponsored features

Ecommerce boom as world adjusts to pandemic driven trends

Promoted by Citi Group COVID-19 has accelerated the use of technologies that help keep us connected, creating a virtual supply chain and expanded digital universe for investors. Read more

Sponsored features

Industrial property – the silver lining in the retail cloud

Promoted by ThinkTank Read more

Sponsored features

Why the non-bank sector appeals to SMSFs

Promoted by Think Tank Read more

Sponsored features

Dissecting the Complexities of Cash Indices Regulations: An In-Depth Analysis

Introduction In recent years, the world of finance has seen a surge of interest in cash indices trading as investors seek potential returns in various markets. This development has brought increased ...Read more

Sponsored features

The Best Ways to Find the Right Trading Platform

Promoted by Animus Webs Read more

Sponsored features

How the increase in SMSF members benefits business owners

Promoted by ThinkTank Read more

Sponsored features

Thinktank’s evolution in residential lending and inaugural RMBS transaction

Promoted by Thinktank When Thinktank, a specialist commercial and residential property lender, recently closed its first residential mortgage-backed securitisation (RMBS) issue for $500 million, it ...Read more

Sponsored features

Investors tap into cyber space to grow their wealth

Promoted by Citi Group Combined, our daily spending adds up to opportunities for investors on a global scale. Read more

Sponsored features

Ecommerce boom as world adjusts to pandemic driven trends

Promoted by Citi Group COVID-19 has accelerated the use of technologies that help keep us connected, creating a virtual supply chain and expanded digital universe for investors. Read more

Sponsored features

Industrial property – the silver lining in the retail cloud

Promoted by ThinkTank Read more

Sponsored features

Why the non-bank sector appeals to SMSFs

Promoted by Think Tank Read more