Resources

Three telling stories from reporting season

Promoted by

Company reports of three ASX retailers demonstrate that Australian households are currently suffering from excessive debt and their consumption patterns are unpredictable.

Three telling stories from reporting season

Promoted by

Company reports of three ASX retailers demonstrate that Australian households are currently suffering from excessive debt and their consumption patterns are unpredictable.

Company reports in recent weeks have confirmed that Australian households are suffering from excessive household debt and their consumption patterns are difficult to predict. This was indeed the observation from the directors of Nick Scali (ASX code: NCK) which produced a stellar FY 17 report.

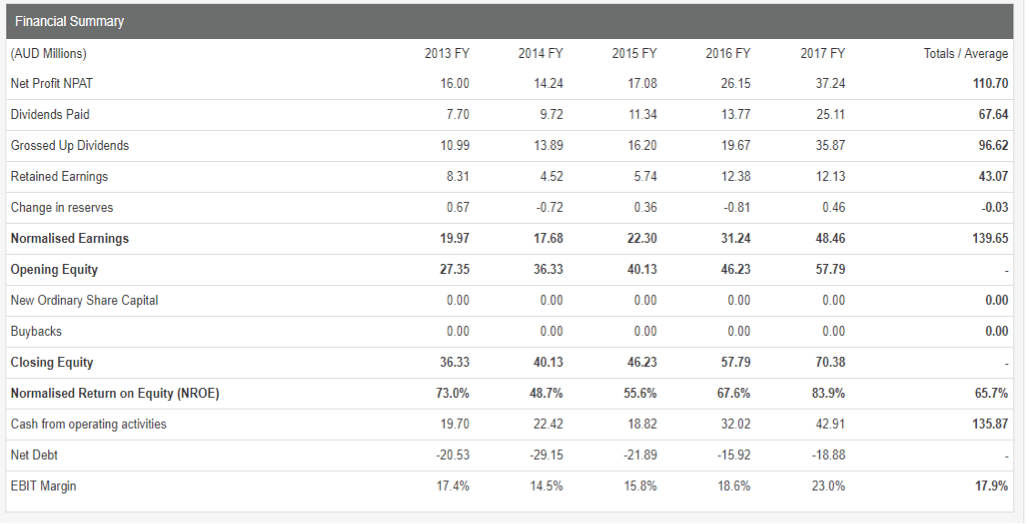

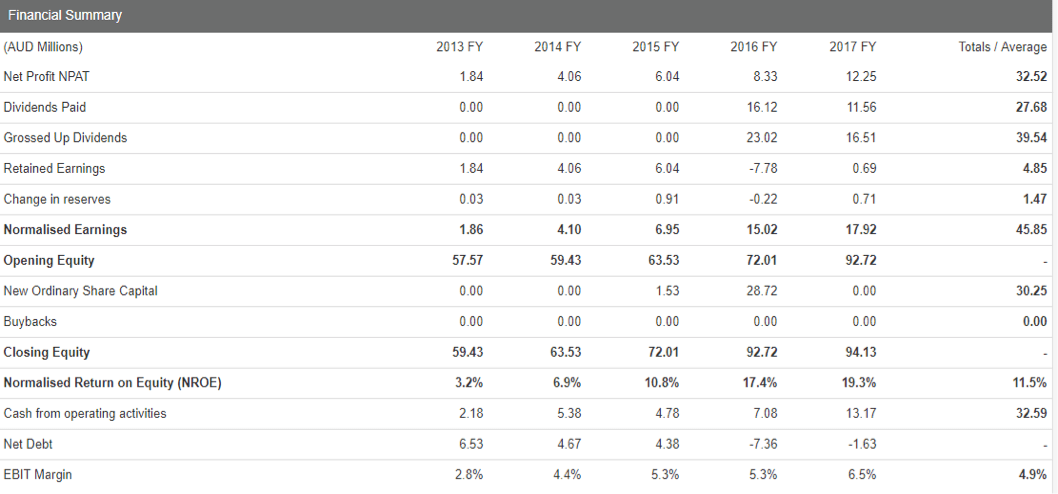

The table below shows the exceptional “self funded” growth achieved by NCK over the last five years. Earnings have grown by 135% without the requirement to raise capital and with net cash approximating $20 million throughout the period. Operating cashflow is 135% of reported profit and profitability (normalised Return On Equity) is amongst the very best in Australia.

Figure 1. NCK Financial Summary

Source. StocksInValue

Over the last year, NCK shares have traded from $5.82 to a high of $7.50. Today’s $6.00 share price represents a market capitalisation of $484 million, with the range of market values from a low of $470 million to a high of $600 million.

The current PER (based on FY17) is 13 times and earnings growth of between 5% and 10% suggests a forward PER of 12 times; this is hardly expensive for an outstanding business.

So why have the shares retreated on the result? Simply because management was guarded in their outlook statement and noted that the costs of store rollouts will slow earnings growth for the next year. This has led to a plethora of speculative activity by traders.

The Australian market is fickle at the best of times, but particularly so at present and has the myopic tendency to focus on the short-term while still demanding long-term growth. Shares are perpetual investments, but today’s Australian share market is dominated by day traders, index arbitrageurs, hedge funds and computer trading. This is a toxic mix of players that creates excess price volatility with little valuation framework. This will become more obvious as we review Dominos (ASX code: DMP).

In July 2016 we wrote in The View about Dominos as follows –

“Today DMP is capitalised at about $6.5 billion with current consensus forecast earnings in 2016/17 of $120 million. The PER is over 50 times earnings. Is this justified?

The five year performance … is impressive. Earnings and cash flow have tripled over five years, while equity has also tripled. So while DMP is growing at a dynamic rate, it is not getting economies of scale reflected in the incremental NROE. More importantly, the substantial capital raising in 2014 to buy the Japanese market franchise has yet to generate the returns of the Australian business.”

When DMP produced its results this week, its shares slumped by 20% having fallen from $80 on its FY16 release to $52 prior to the FY17 release. In terms of market capitalisation, the market value moved from $7.1 billion (August 16) to $4.6 billion (July 17) to $3.7 billion today.

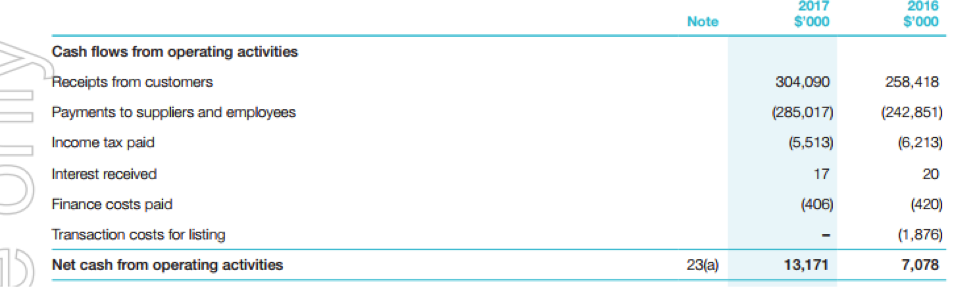

The result produced the following financial statements that show the $7 billion market value of a year ago was fantasy. First, operating cashflow of $132 million is good but hardly shows exciting growth from FY16 to FY17.

Figure 2. DMP Operating Cash Flows

Source. Annual Reports

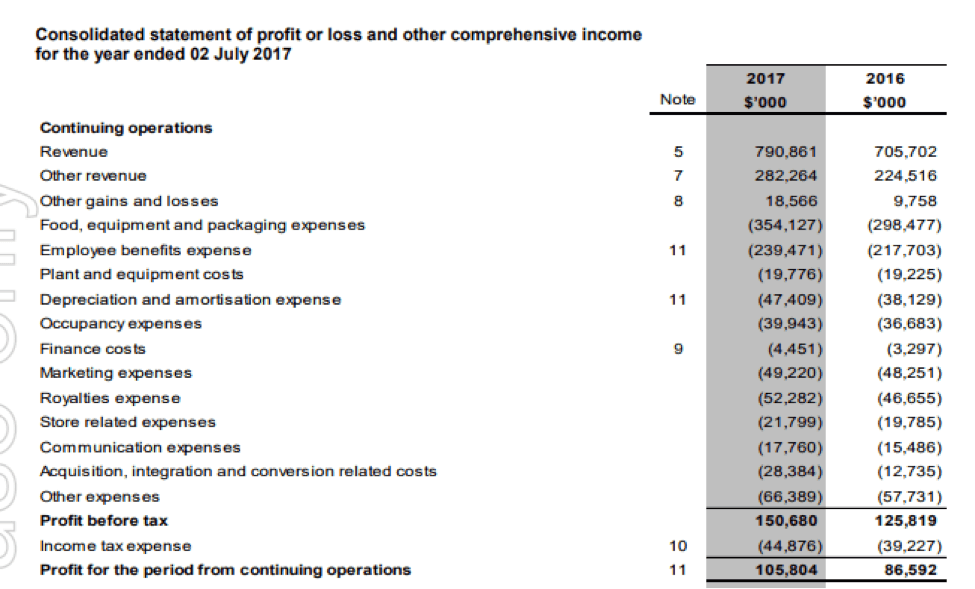

While the NPAT growth is more impressive at 22%, it came as a result of major offshore acquisitions and a significant increase in debt.

Figure 3. DMP Consolidated P&L Statement

Source. Annual Reports

At 35 times earnings for FY17, DMP does not present as value even after a 50% fall in price. What was the market thinking 12 months ago? Further, how could DMP justify a share buyback of $300 million today?

Another retail stock that has been battered back to reality on its FY 17 result is Baby Bunting (ASX code: BBN). On sober reflection, it is clear that its market value was simply too high.

The following tables put everything into perspective. As BBN transitioned from a private company to a public listed company on the ASX in October 2015, it did so with a $28 million capital raising. Notably it had 125.7 million shares on issue and apparently the market forgot this in determining its value.

Figure 4. BBN Operating Cash Flows

Source. Annual Reports

From Oct 2015 (share price $1.80), the market revalued BBN to $3.15 in August 2016. The market capitalisation ballooned from about $220 million to $396 million. In August 2016, the cash flow multiple was 30 times forward 12 month earnings. Today the price is lower than October 2015 and yet the company has achieved what was essentially expected by any rational investor.

To reiterate that performance has been solid, we observe from below that over the last 2 years the company has maintained solid growth and actually improved profitability. Shareholders would be happy if there wasn’t a share price to watch.

Figure 5. BBN Financial Summary

Source. StocksInValue

Clime is an independent, highly esteemed Australian fund manager specialising in value investing and focused on delivering absolute returns. To access Investing Reports and exclusive white papers, click here.

RELATED ARTICLES

Sponsored features

Dissecting the Complexities of Cash Indices Regulations: An In-Depth Analysis

Introduction In recent years, the world of finance has seen a surge of interest in cash indices trading as investors seek potential returns in various markets. This development has brought increased ...Read more

Sponsored features

The Best Ways to Find the Right Trading Platform

Promoted by Animus Webs Read more

Sponsored features

How the increase in SMSF members benefits business owners

Promoted by ThinkTank Read more

Sponsored features

Thinktank’s evolution in residential lending and inaugural RMBS transaction

Promoted by Thinktank When Thinktank, a specialist commercial and residential property lender, recently closed its first residential mortgage-backed securitisation (RMBS) issue for $500 million, it ...Read more

Sponsored features

Investors tap into cyber space to grow their wealth

Promoted by Citi Group Combined, our daily spending adds up to opportunities for investors on a global scale. Read more

Sponsored features

Ecommerce boom as world adjusts to pandemic driven trends

Promoted by Citi Group COVID-19 has accelerated the use of technologies that help keep us connected, creating a virtual supply chain and expanded digital universe for investors. Read more

Sponsored features

Industrial property – the silver lining in the retail cloud

Promoted by ThinkTank Read more

Sponsored features

Why the non-bank sector appeals to SMSFs

Promoted by Think Tank Read more

Sponsored features

Dissecting the Complexities of Cash Indices Regulations: An In-Depth Analysis

Introduction In recent years, the world of finance has seen a surge of interest in cash indices trading as investors seek potential returns in various markets. This development has brought increased ...Read more

Sponsored features

The Best Ways to Find the Right Trading Platform

Promoted by Animus Webs Read more

Sponsored features

How the increase in SMSF members benefits business owners

Promoted by ThinkTank Read more

Sponsored features

Thinktank’s evolution in residential lending and inaugural RMBS transaction

Promoted by Thinktank When Thinktank, a specialist commercial and residential property lender, recently closed its first residential mortgage-backed securitisation (RMBS) issue for $500 million, it ...Read more

Sponsored features

Investors tap into cyber space to grow their wealth

Promoted by Citi Group Combined, our daily spending adds up to opportunities for investors on a global scale. Read more

Sponsored features

Ecommerce boom as world adjusts to pandemic driven trends

Promoted by Citi Group COVID-19 has accelerated the use of technologies that help keep us connected, creating a virtual supply chain and expanded digital universe for investors. Read more

Sponsored features

Industrial property – the silver lining in the retail cloud

Promoted by ThinkTank Read more

Sponsored features

Why the non-bank sector appeals to SMSFs

Promoted by Think Tank Read more