Save

The ATO has released new LRBA guidance. What does it mean for me?

The ATO has released new LRBA guidance. What does it mean for me?

One of the major issues with LRBAs has been around the terms of loans from related parties.

In December 2014, the ATO confirmed that in its view, all loans by related parties to trustees of SMSFs must be on terms that are consistent with an arm’s length dealing (see ATO IDs 2014/39 and 2014/40). If the loan terms were not, then the income from the LRBA is non-arm’s length income to the SMSF and taxed at the top marginal tax rate in the SMSF (instead of the normal rate of 15 per cent, or no tax for income from assets supporting an income stream or pension).

This meant that the trustees of SMSFs who had borrowed from a related party must review the terms of their loan arrangements to ensure they on the same terms as what an arm’s length lender would require.

The ATO provided an effective deadline of 30 June 2016 for trustees of SMSFs to get their loan arrangements in order.

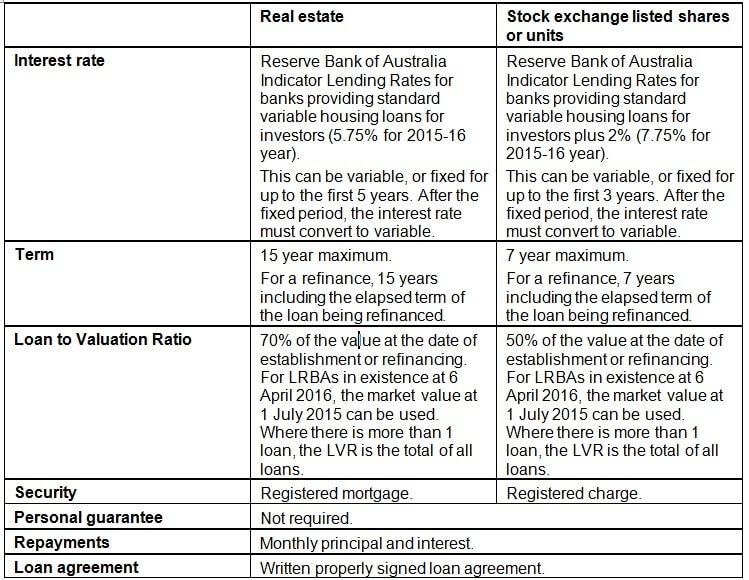

To provide certainty around what the ATO considers arm’s length terms, in April 2016 the ATO released PCG 2016/5. It contains safe harbour terms that the ATO will accept are arm’s length, so if followed, the income from the LRBA will not be considered non-arm’s length income to the SMSF purely because of the terms of the borrowing.

What are the safe harbour rules?

This is a summary of the key safe harbour rules:

When must the LRBA comply by?

The safe harbour rules apply both to existing LRBAs and those established after the release of PCG 2016/5.

In PCG 2016/5, the ATO confirms it will not select an SMSF for an income tax review for the 2014-15 or earlier years purely because the SMSF has entered into an LRBA if by 30 June 2016:

• all loans are on terms consistent with an arm’s length dealing, or the LRBA is wound up; and

• the SMSF trustee has made principal and interest payments for the 2015-16 year that are consistent with an arm’s length dealing.

Are there other options?

The ATO accepts that alternative loan terms can be consistent with an arm’s length dealing, but the onus will be on the trustees of the SMSF to establish they are consistent with an arm’s length dealing.

This means the options for trustees of SMSFs with LRBAs that have loans from related parties are to:

1. ensure the terms of the related party loan comply with the safe harbour rules by 30 June 2016 (including making principal and interest payments for the 2015-16 year consistent with an arm’s length dealing);

2. wind up the LRBA by 30 June 2016 (for example, by selling the asset or paying out the debt and transferring it to the SMSF), having made principal and interest payments for the 2015-16 year consistent with an arm’s length dealing; or

3. ensure they have extrinsic evidence that the terms of the existing arrangement are consistent with an arm’s length dealing (for example, because they are substantially the same as an offer of finance from a bank).

Is it just the loan terms to worry about?

The terms of the loan are an important part of an LRBA, but there are many other rules that are just as important. A breach of any of the rules can result in compliance issues for the SMSF or for the income from the LRBA to be non-arm’s length income to the SMSF (and taxed at the top marginal tax rate).

Now is a good opportunity for trustees of SMSFs to review their LRBAs, particularly where the lender is a related party, not only for the loan terms, but also for compliance with all the other rules as well.

Scott Hay-Bartlem, partner, Cooper Grace Ward

RELATED ARTICLES

Tax saving

Investor tax shifts squeeze borrowing power: what boards, lenders and developers need to do next

Australia’s proposed changes to capital gains tax concessions and negative gearing are already flowing through lender calculators, shaving investor serviceability at the margins that matterRead more

Tax saving

Budget relief now, capital friction later: what SMEs should really plan for

The Federal Budget hands small businesses short‑term relief, but looming changes to investment and trust taxation could reshape capital flows, risk appetite and valuations across Australia’s SME ...Read more

Tax saving

Clarity as capital: why the ATO’s rental deduction guidance is now a business strategy issue

The Tax Institute’s push for plainer, more practical ATO guidance on rental property deductions is not a semantic debate; it’s a capital allocation problem. Ambiguous rules inflate compliance costs, ...Read more

Tax saving

$20,000 instant asset write-off extension welcomed, but calls for broader support grow

The Australian government's decision to extend the $20,000 instant asset write-off into the next financial year has been met with approval from business leaders. However, there are growing calls for ...Read more

Tax saving

The downsizer dividend: How targeted tax levers could unlock housing supply in Australia

A call by Raine & Horne to incentivise seniors to move to smaller homes has kicked off a wider policy conversation that reaches well beyond real estate. If designed well, a targeted package could ...Read more

Tax saving

Raine & Horne's bold move could unlock housing supply but what are the hidden risks

Raine & Horne’s call for targeted tax incentives to encourage empty nesters to ‘rightsize’ isn’t just another sector wish list; it’s a potential lever to free up family homes, ease rental ...Read more

Tax saving

From annual check-ups to always‑on: how modern portfolio reviews unlock after‑tax alpha

The era of once‑a‑year portfolio check‑ins is over. Continuous, tech‑enabled reviews now drive returns through tax efficiency, risk control and behavioural discipline—especially in a high‑rate ...Read more

Tax saving

Navigating tax laws for capital gains in 2023

The landscape of Australian tax laws surrounding capital gains is ever-changing, with 2023 being no exception. Read more

More articles

OUR PLATFORMS AND BRANDS

EVENTS AND SUMMITS

- ACE25 The Accounting Conference and Exhibition

- Australian Accounting Awards

- Australian AI Awards

- Australian Aviation Awards

- Australian Aviation Summit

- Australian Broking Awards

- Australian Cyber Awards

- Australian Cyber Summit

- Australian Defence Industry Awards

- Australian Law Awards

- Australian Law Forum

- Australian Space Awards

- Australian Space Summit

- Better Business Awards

- Better Business Summit

- Broker Innovation Awards

- Broker Innovation Summit

- Budget Summit

- Corporate Counsel Summit

- Defence & National Security Workforce Awards

- Lawyers Weekly 30 Under 30 Awards

- Commerical Finance Awards

- New Broker Academy

- Partner of the Year Awards

- Partner Summit

- REB Awards

- Rising Star Awards

- SME Bootcamp

- Women in Finance Awards

- Women in Finance Summit

- Women in Law Awards

- Women in Law Forum

PODCASTS

- Accountants Daily Podcast Network

- Australian Aviation Podcast Network

- Broker Daily Podcast Network

- Defence Connect Podcast Network

- HR Leader Podcast Network

- REB Podcast Network

- Space Connect Podcast

- The Adviser Podcast Network

- The ifa Show

- The Lawyers Weekly Show

- The Smart Property Investment Show

LEARNING AND EDUCATION

MOMENTUM MARKETS NETWORK

STAY CONNECTED

Make your nest egg grow. Register now for nestegg updates.