Retirement

How the new contribution rules could boost your super

By utilising the new deductible contribution rules and committing to tipping money into super early, plenty of Australians can achieve a balance of $1 million by age 65, says HLB Mann Judd.

How the new contribution rules could boost your super

By utilising the new deductible contribution rules and committing to tipping money into super early, plenty of Australians can achieve a balance of $1 million by age 65, says HLB Mann Judd.

The rule changes to super on 1 July 2017 have made it much easier to make additional contributions to super, says HLB Mann Judd wealth management partner Jonathan Philpot.

One of the pivotal changes has been to deductible contributions to super. Before 1 July 2017, only self-employed people could claim personal super contributions as a tax deduction.

But according to the Australian Taxation Office, "most people under under 75 years old will [now] be able to claim a tax deduction on personal superannuation contributions".

Mr Philpot says that means Australians can use personally deductible contributions to start building their super balances from a much younger age.

"In the past, employees had to elect to salary-sacrifice in order to make additional superannuation contributions and receive the associated tax savings. Now, people earning salary and wages are able to make voluntary contributions to superannuation on their own behalf and claim a tax deduction in their personal tax return," Mr Philpot said.

"In fact, people will need to start consciously building their superannuation in their 40s, and should be trying to contribute as close to the maximum of $25,000 a year as they can, as their main form of long-term savings.

"By making additional deductible contributions through to age 65, people can significantly grow their super balance and potentially get it well above a million dollars," he said.

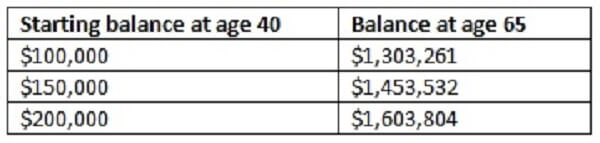

Mr Philpot gave an example of a 40-year-old with a super balance of $100,000 who commits to making the maximum concessional contribution of $25,000 a year, laid out in the table below.

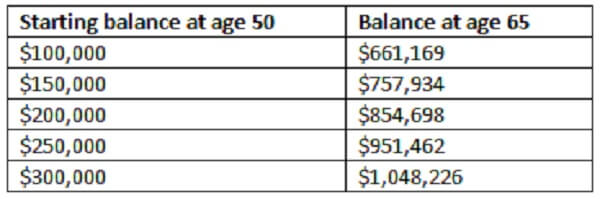

In contrast, he said, a 50-year-old with the same opening balance would be significantly worse off:

"For most people in their 40s, repaying the home mortgage is — understandably — the main focus. While this should continue to a be a focus, once people have their mortgage under control, it is worth considering using the offset account to make additional concessional contributions to super," Mr Philpot said.

"Relying solely on the superannuation guarantee contribution of 9.5 per cent is unlikely to allow most people to save enough for a comfortable retirement – something that many people still seem to be unaware of."

He added that the new changes to superannuation contributions doesn’t automatically spell the end of salary sacrifice arrangements.

"The changes don’t necessarily mean people should cease their salary sacrifice arrangements, as they have two main benefits.

"Firstly, it is an automated savings option, making it easier for people to chip away at growing their wealth as it can be a struggle to come up with funds at year end to contribute to superannuation.

"Secondly the tax benefit is immediate, as it is pre-tax dollars that are salary sacrificed, whereas when using the personal contribution method people have to wait until lodging their tax return for the tax refund," Mr Philpot said.

RELATED ARTICLES

Superannuation

Rest strengthens digital engagement with new leadership appointment

In a significant move to enhance its digital member services, Rest, one of Australia's largest profit-to-member superannuation funds, has appointed Darran Arnott as General Manager, DigitalRead more

Superannuation

Aware Super earns adviser-ready fund accreditation under new national framework

In a significant development for the financial advice sector, Aware Super has been awarded the prestigious Adviser-Ready Fund accreditation. This recognition comes under a new national framework ...Read more

Superannuation

Superannuation overhaul: Payday Super set to enhance retirement savings for millions

In a significant shift set to impact the retirement savings of millions of Australians, the way superannuation contributions are paid is about to undergo a major overhaul. However, despite the ...Read more

Superannuation

Rest expands retail property portfolio with US$250 million investment in US real estate fund

Rest, one of Australia's largest profit-to-member superannuation funds, has announced a substantial investment in a US-based real estate fund, marking a strategic expansion of its retail property ...Read more

Superannuation

TelstraSuper and Aware Super merger advances with key agreement

In a significant development for the Australian superannuation sector, TelstraSuper and Aware Super have reached a pivotal milestone in their merger journey by signing the Successor Fund Transfer ...Read more

Superannuation

Rest applauds legislative reforms to boost superannuation for low-income earners

In a landmark move, Rest has expressed strong approval following the successful passage of legislation aimed at enhancing the Low Income Superannuation Tax Offset (LISTO) through ParliamentRead more

Superannuation

Rest promotes Rachel O’Connor to head fixed income team

In a significant move within Australia's superannuation sector, Rest, one of the largest profit-to-member funds in the country, has announced the promotion of Rachel O'Connor to lead its Fixed Income ...Read more

Superannuation

Employment Hero raises concerns over superannuation bill's impact on small businesses

Employment Hero has raised significant concerns regarding the implementation of the proposed Supporting Choice in Superannuation and Other Measures Bill, which was recently recommended for passage by ...Read more

Superannuation

Rest strengthens digital engagement with new leadership appointment

In a significant move to enhance its digital member services, Rest, one of Australia's largest profit-to-member superannuation funds, has appointed Darran Arnott as General Manager, DigitalRead more

Superannuation

Aware Super earns adviser-ready fund accreditation under new national framework

In a significant development for the financial advice sector, Aware Super has been awarded the prestigious Adviser-Ready Fund accreditation. This recognition comes under a new national framework ...Read more

Superannuation

Superannuation overhaul: Payday Super set to enhance retirement savings for millions

In a significant shift set to impact the retirement savings of millions of Australians, the way superannuation contributions are paid is about to undergo a major overhaul. However, despite the ...Read more

Superannuation

Rest expands retail property portfolio with US$250 million investment in US real estate fund

Rest, one of Australia's largest profit-to-member superannuation funds, has announced a substantial investment in a US-based real estate fund, marking a strategic expansion of its retail property ...Read more

Superannuation

TelstraSuper and Aware Super merger advances with key agreement

In a significant development for the Australian superannuation sector, TelstraSuper and Aware Super have reached a pivotal milestone in their merger journey by signing the Successor Fund Transfer ...Read more

Superannuation

Rest applauds legislative reforms to boost superannuation for low-income earners

In a landmark move, Rest has expressed strong approval following the successful passage of legislation aimed at enhancing the Low Income Superannuation Tax Offset (LISTO) through ParliamentRead more

Superannuation

Rest promotes Rachel O’Connor to head fixed income team

In a significant move within Australia's superannuation sector, Rest, one of the largest profit-to-member funds in the country, has announced the promotion of Rachel O'Connor to lead its Fixed Income ...Read more

Superannuation

Employment Hero raises concerns over superannuation bill's impact on small businesses

Employment Hero has raised significant concerns regarding the implementation of the proposed Supporting Choice in Superannuation and Other Measures Bill, which was recently recommended for passage by ...Read more