Retirement

What are some of the biggest mistakes you see SMSF trustees make with their insurance?

Retirement

What are some of the biggest mistakes you see SMSF trustees make with their insurance?

While there are some significant benefits associated with holding insurance within a super fund, there are also many traps trustees must watch out for, particularly if the beneficiaries are non-tax dependants.

What are some of the biggest mistakes you see SMSF trustees make with their insurance?

While there are some significant benefits associated with holding insurance within a super fund, there are also many traps trustees must watch out for, particularly if the beneficiaries are non-tax dependants.

Life insurance

When we buy a life insurance policy we buy it with the intention that our loved ones will be financially cared for in a difficult time. We like to think that our dependants are taken care of, especially if our departure is sudden and even more so if it’s a traumatic event. However, did you know that the government may take an extra 15 per cent of the insurance payout at the time?

This comes about if deductions have been claimed on the premiums for a life policy and the lump sum insurance payout goes to a non-tax dependant. You might say, that’s OK, I only have dependants, but did you know that children can be classed as a non-tax dependant?

To claim or not to claim – this needs to be addressed now, not later!

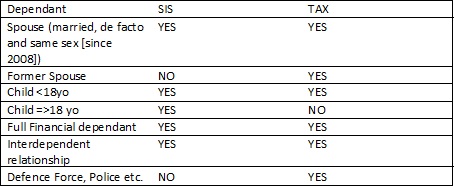

Now, this extra 15 per cent only occurs if the death benefit is paid to a non-tax dependant. So who is a dependant and who is a non-tax dependant? There is a slight difference in definitions between SIS legislation and tax legislation, remembering that the SIS legislation tells us who a death benefit can be paid to and the tax legislation tells us how it will be taxed.

So from the above table, an adult child who is not fully financially dependent on the deceased, ie, they would not be financially able to support their basic needs without the support of the deceased at the time of death, would not qualify for a tax-free lump sum death benefit.

How to avoid the non-tax dependant tax

If you only have tax dependants then a lump sum death benefit will be tax free.

If you have non-tax dependants:

• For cash flow reasons, you may still prefer your super fund to hold the life insurance policy, so that the premiums are not coming out of your everyday finances. Then if you wish to avoid the extra 15 per cent tax, don’t claim the tax deduction for the premiums.

• What if you have been claiming the deduction while your children are minors, then they turn 19 and are no longer financially dependent on you? Can you just stop claiming the deduction at that point? In a word, no. A new policy would need to be put in place and the deductions on the new policy not claimed.

• Hold the life insurance policy outside of super, the premiums will not be deductible, but the insurance payout is tax free to non-tax dependents.

• Discuss strategies with your qualified, licenced adviser as to how you can increase the tax exempt component of your super benefits for a possible pension payout, rather than a lump sum payout to a non-tax dependant.

Landlord insurance

There is increasing interest in SMSFs investing in property, especially from the younger generation who have the time to benefit from the potential capital gains over the longer term when they retire. However, many don’t take out landlord insurance to protect the super fund investment. We all sign the ATO Trustee Declaration, but have we really read it? Under trustee duties, it states, “I understand that by law I must: ... take appropriate action to protect the fund’s assets.” A prudent trustee would take out landlord insurance to meet this important obligation.

Who should own the landlord insurance?

The trustee of the super fund should be the owner of the landlord insurance policy. The ownership title should include ATF (As Trustee For) Jobloggs Super Fund to make it crystal clear that it’s a policy owned by the super fund, which is very important when there are individual trustees, or a corporate trustee who also trades.

Where there is a limited recourse borrowing arrangement (LRBA), people are often confused as to whether the super fund should hold the policy or the bare trustee, who is named on the purchase contract. If we think about the end payout, in a situation where we need to claim on the insurance policy, if the bare trustee holds the policy, it would need to open a bank account, have the insurance payout deposited to that bank account, pay for the repairs, etc, then close the bank account again. This scenario opens up Pandora’s box down the track when the property is transferred back to the super fund from the bare trust at nominal stamp duty rates. There may be a risk the office of state revenue (OSR) will argue that the bare trust was in fact an operating trust and apply a much larger stamp duty liability on the property transfer. Even if you or your accountant can argue that the trust is only a bare trust for the LRBA requirements, who wants to deal with the extra headache of providing the documentary evidence and the additional expense of the accountants’ time arguing with the OSR. To avoid this potential problem, the insurance policy for the property should be held by the trustee of the super fund.

Bundling multiple policies

Often insurance companies will offer discounts if you bundle multiple policies together. Where a super fund trustee is a corporate trustee which also trades, this can lead to problems when the insurance broker offers to bundle the business insurance with the landlord insurance. Again, take another look at the ATO Trustee Declaration – it is the duty of the SMSF trustee to ensure that “my money and other assets are kept separate from the money and other assets of the fund”. The trustee of the super fund should hold a separate landlord policy from the business insurance policy, to cover the property held by the super fund.

Catherine Price, principal auditor, TABS Super Fund Auditors

RELATED ARTICLES

Self managed super fund

Australia’s SMSF sector experiences record growth, driven by digital asset interest

The self-managed superannuation fund (SMSF) sector in Australia has experienced unprecedented growth, with a record 33,224 net new funds established in the 2024–25 financial year. This marks a ...Read more

Self managed super fund

Financial progress hinges on ambition, not income, says Stake Report

Australia faces a financial turning point, with new research from online investment platform Stake revealing a nation divided into two distinct groups: the 'Starters', who invest and feel in control ...Read more

Self managed super fund

OKX targets Australia's $1 trillion SMSF market with new crypto platform launch

In a significant move aimed at capitalising on Australia's burgeoning digital asset market, global onchain technology company OKX has unveiled a new Self-Managed Super Fund (SMSF) expansion on its ...Read more

Self managed super fund

Industry leaders launch SMSF Innovation Council to drive digital transformation

A consortium of finance industry leaders has launched an SMSF Innovation Council to help Australia's $1.02 trillion self-managed superannuation fund industry navigate digital transformation. Read more

Self managed super fund

Superannuation guarantee to be paid on government paid parental leave, says ASFA

The Association of Superannuation Funds of Australia (ASFA) has hailed the government's decision to include Superannuation Guarantee payments with its Paid Parental Leave policy as a critical step ...Read more

Self managed super fund

SMSF experts advise against hasty reactions to potential super tax changes

As the Australian Government proposes a new tax measure on superannuation earnings for balances exceeding $3 million, experts from the self-managed super funds (SMSF) sector are urging members not to ...Read more

Self managed super fund

Federal government announces changes to superannuation contribution caps

The Federal Government has announced changes to the superannuation contribution caps, impacting self-managed super funds (SMSFs) and their members from 1 July 2024. Read more

Self managed super fund

SMSF Association calls for joint effort to tackle early super access

The SMSF Association is calling on a collaborative approach including the Government, the Australian Taxation Office (ATO), the Australian Securities and Investments Commission (ASIC), and the ...Read more

Self managed super fund

Australia’s SMSF sector experiences record growth, driven by digital asset interest

The self-managed superannuation fund (SMSF) sector in Australia has experienced unprecedented growth, with a record 33,224 net new funds established in the 2024–25 financial year. This marks a ...Read more

Self managed super fund

Financial progress hinges on ambition, not income, says Stake Report

Australia faces a financial turning point, with new research from online investment platform Stake revealing a nation divided into two distinct groups: the 'Starters', who invest and feel in control ...Read more

Self managed super fund

OKX targets Australia's $1 trillion SMSF market with new crypto platform launch

In a significant move aimed at capitalising on Australia's burgeoning digital asset market, global onchain technology company OKX has unveiled a new Self-Managed Super Fund (SMSF) expansion on its ...Read more

Self managed super fund

Industry leaders launch SMSF Innovation Council to drive digital transformation

A consortium of finance industry leaders has launched an SMSF Innovation Council to help Australia's $1.02 trillion self-managed superannuation fund industry navigate digital transformation. Read more

Self managed super fund

Superannuation guarantee to be paid on government paid parental leave, says ASFA

The Association of Superannuation Funds of Australia (ASFA) has hailed the government's decision to include Superannuation Guarantee payments with its Paid Parental Leave policy as a critical step ...Read more

Self managed super fund

SMSF experts advise against hasty reactions to potential super tax changes

As the Australian Government proposes a new tax measure on superannuation earnings for balances exceeding $3 million, experts from the self-managed super funds (SMSF) sector are urging members not to ...Read more

Self managed super fund

Federal government announces changes to superannuation contribution caps

The Federal Government has announced changes to the superannuation contribution caps, impacting self-managed super funds (SMSFs) and their members from 1 July 2024. Read more

Self managed super fund

SMSF Association calls for joint effort to tackle early super access

The SMSF Association is calling on a collaborative approach including the Government, the Australian Taxation Office (ATO), the Australian Securities and Investments Commission (ASIC), and the ...Read more