Resources

Is the impending doom of Amazon’s arrival overhyped?

Promoted by

Beyond near-term investment implications of Amazon’s arrival, what are some of the potential challenges the ‘Amazon effect’ will bring to everyday Australians?

Is the impending doom of Amazon’s arrival overhyped?

Promoted by

Beyond near-term investment implications of Amazon’s arrival, what are some of the potential challenges the ‘Amazon effect’ will bring to everyday Australians?

Implications for Everyday Australians

Much has been written about the impending arrival of Amazon in Australia and potential disruption across a range of domestic retail businesses. In business as in nature, continuing to thrive ultimately comes down to adaptation to the prevailing environment. The growing acceptance of technology has seen a marked increase in the rate of change across many industries. ‘Faster, cheaper, smarter, easier’ solutions leading to an improved customer experience are rapidly becoming available via cutting-edge technology.

Beyond the near-term investment implications, this article examines some of the potential structural challenges the ‘Amazon effect’ will bring to everyday Australians.

A Brave New World

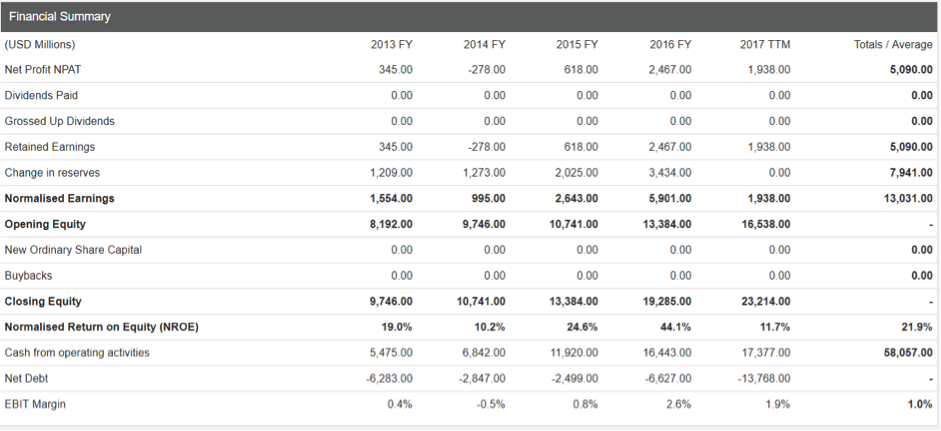

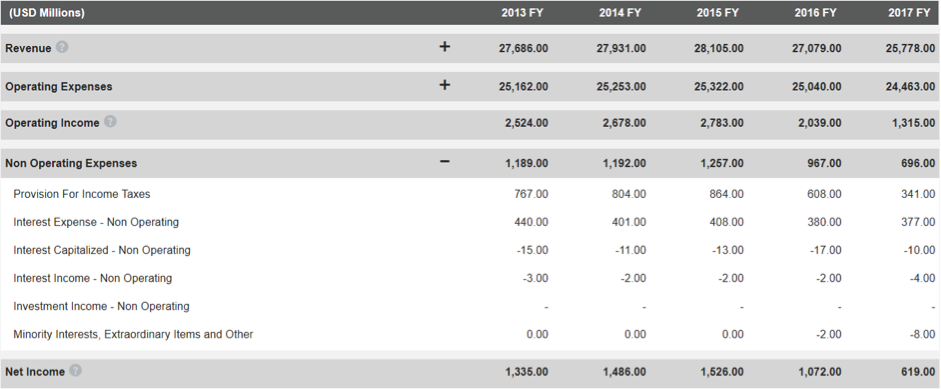

The financial summary of Amazon below demonstrates the strong cash flow, significant reinvestment and growth in equity value, net cash position, yet paltry EBIT margin of this extraordinary company. At the headline level, over the past five years, Amazon has generated USD $58bn in cash from operating activities, leading to USD $13bn in normalised earnings and USD $5bn in NPAT.

Figure 1. Amazon 5-Year History (August 2017), USD

Source. StocksInValue

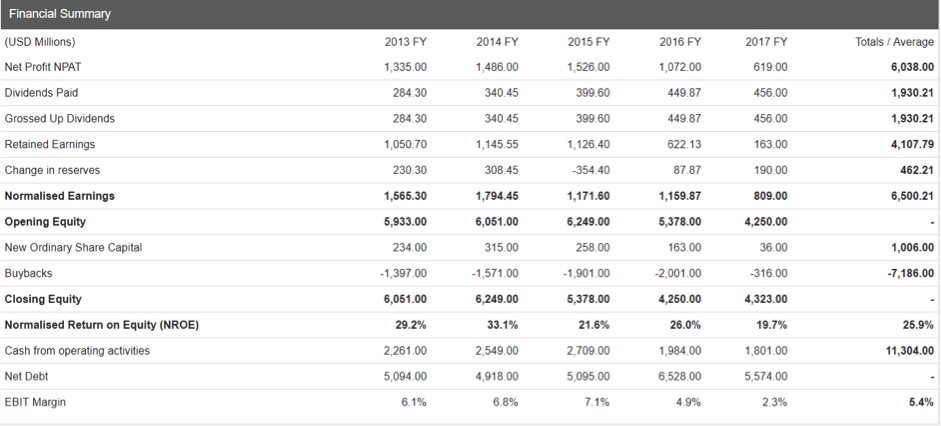

Contrasting this with the equivalent financial summary for Macy’s, which has been significantly disrupted by Amazon and challenged by consumer desire for more experiential shopping destinations, paints an interesting picture. At the headline level, over the past five years, Macy’s has generated USD $11bn in cash from operating activities, undertaken significant share buy-backs, delivered USD $6.5bn in normalised earnings and USD $6bn in NPAT. At the NPAT level, Macy’s has generated almost USD $1bn more than Amazon over the past five years.

Figure 2. Macy’s 5-Year History (August 2017), USD

Source. StocksInValue

Playing the Long Game

Clearly Amazon’s business model thus far has not been focused on traditional business outcomes such as generating profits. Rather Jeff Bezos has been building sizable market share, reinvesting to grow the business both vertically and horizontally, redefining the customer shopping experience to be primarily on-line and arguably significantly disrupting existing market participants, thus weakening competition. This has been Amazon’s strategy to date.

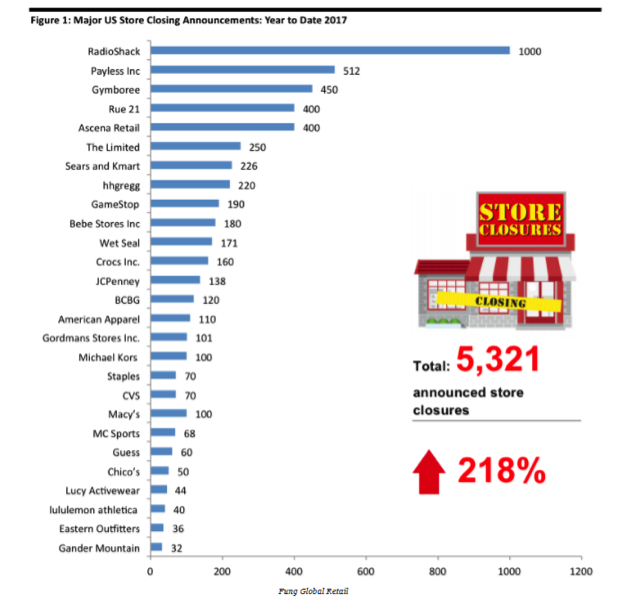

Around this time 12 months ago, Macy’s announced the closure of 100 stores across the United States. This represents approximately 1/7th of its full-line store footprint and directly affected around 10,000 staff. While representative in nature and not entirely attributable to Amazon, the below chart demonstrates the influence that the growth of e-commerce more broadly has had in disrupting traditional retailing. The flow-on effects to the displaced workers, local communities and the broader US economy are substantial. The planned closure of Macy’s 100 stores in the context of the below store closure announcements is staggering.

Figure 3. US Major Store Closures, YTD 2017

Source: Business Insider

(Deferred) Tax Revenues?

Traditional business principles suggest that at some stage in a company’s development, there will be a focus on generating profits. In the case of Amazon’s investment journey, reinvestment to grow the business and grow the value of equity has been the key priority. The implications for established taxation laws and resulting tax collection is at best a deferral of tax collection until future years and at worst, efficiently transferring eventual tax revenues to low / no tax paying jurisdictions. There are a number of high profile European examples to date of the latter including Apple, Google, Microsoft and … Amazon.

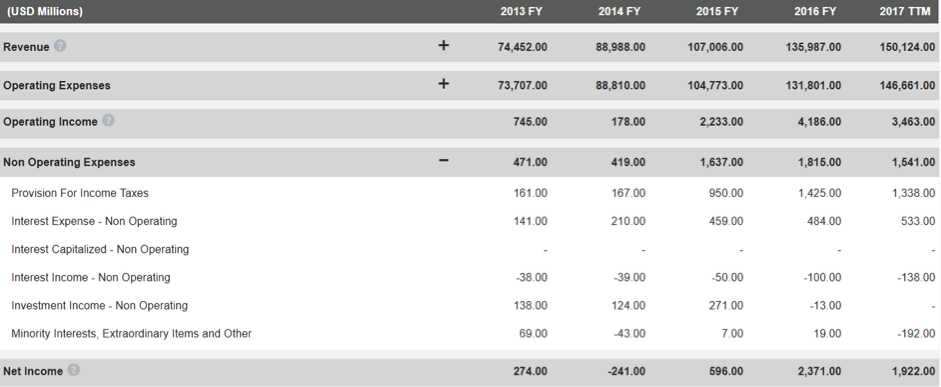

The 5-year history of Amazon’s high-level profit and loss statement below shows that over this period Amazon’s total revenues have more than doubled from USD $74bn to USD $150bn (total revenues of the 5 years of USD $557bn). Provisioning for Income Taxes over the 5-years on this $557bn of revenues is just over USD $4bn. By the nature of its business, Amazon has considerable R&D expenses, and also considerable administrative expenses.

Figure 4. Amazon 5-Year Profit & Loss History (August 2017), USD

Source: StocksInValue

In comparison, over the past 5 years, on USD $137bn in total revenues Macy’s has provisioned USD $3.4bn for income taxes. Over this time Macy’s annual revenue has declined by 7%. The divergence in strategy between the two businesses is apparent in Amazon’s USD $557bn in revenues over the 5 years being four times greater than Macy’s total revenues of USD $137bn over the same period. Yet Amazon’s total provisioning for income taxes of USD $4bn over the period is less than 20% higher than Macy’s at USD $3.4bn.

Figure 5. Macy’s 5-Year Profit & Loss History (August 2017), USD

Source: StocksInValue

Australian Implications

Amazon is estimated to have more than 350,000 employees globally. Via ‘Jobs Fairs’ and other hiring promotions this number is growing by the day. Returning to the Macy’s comparison, across Macy’s, Bloomingdale’s, Bluemercury and other affiliated stores, Macy’s has approximately 140,000 employees. These employees are primarily located across 45 of the states in the US.

Notwithstanding Amazon’s spread of employees across the US, employment is highly concentrated in Washington, California, Texas, New Jersey, Kentucky and Pennsylvania. This contrasts with Macy’s employment distribution which is more evenly spread right across the country. Being a traditional retailer, the flow-on effects of Macy’s employees spending their regular income in the local community keeps the ‘flywheel’ of spending, investment, employment (and tax revenue collection) spinning.

Interpolating the same likely retail disruption once Amazon is operational in Australia draws out a number of interesting implications.

Continuing Subdued Inflation & Wage Growth

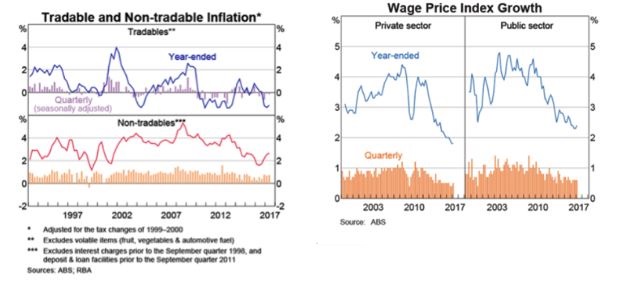

The below inflation chart shows a clear picture of subdued inflation, particularly in the tradables sector. Wage growth in both the private and public sector is declining. When combined with the improvement in Australia’s unemployment rate, this suggests a marked elongation in the Phillips curve inverse relationship between inflation and unemployment. These observations are not unique to Australia. They are also seen across much of the developed world. Amazon’s arrival in Australia is likely to see continuing downward pressure being applied to prices and the benign outlook for inflation and wages growth being prolonged.

Figure 6a & 6b. Tradable & Non-tradable Inflation and Wage Price Index Growth, Public & Private Sector

Source: RBA Chart Pack (data updated to 27 July 2017)

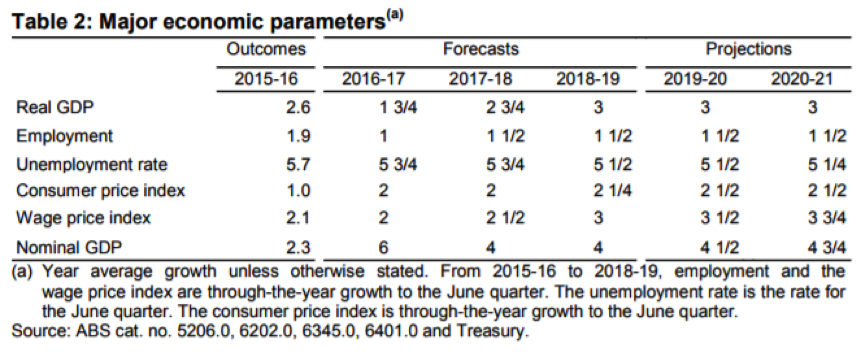

Heroic Assumptions in 2017-18 Budget Projections

Within the context of a subdued inflation and wages growth outlook, the 2017-18 Budget Paper projections of a return to 3%, 3.5% and 3.75% p.a. wages growth over the coming years seem increasingly improbable. The implication is that PAYG bracket creep will be less than budget estimates and as a result the federal government will need to find tax revenues from other sources.

Figure 7.

Source: Budget Paper No.1: Budget Strategy and Outlook 2017-18

Logical Sources for Increased Taxation Revenue

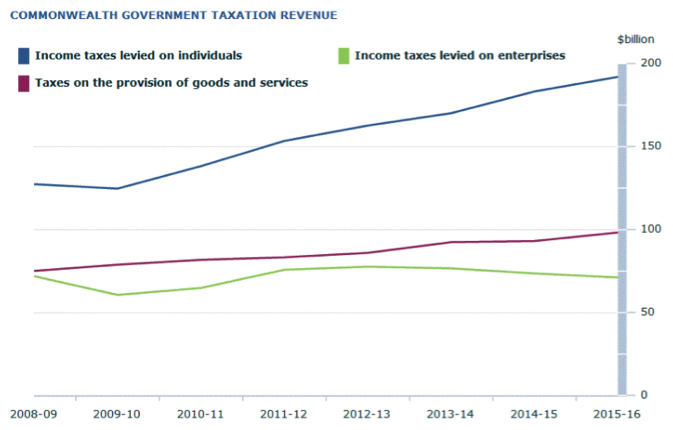

As shown in the chart below, income taxes levied on individuals remain the largest (and increasing) source of federal government tax revenue. The Labor Opposition’s plans to make the temporary Budget repair levy more permanent and result in a marginal tax rate of 49.5% for high income earners signals a clear intention in their strategy to increase tax revenues. At circa AUD $2.3 trillion, the Australian Superannuation system represents another prospective area for indirectly and directly garnering tax revenue. Effective July 2017, the reduction of concessional contributions cap to $25,000 p.a., the reduction of non-concessional contributions cap to $100,000 p.a. and the $1.6m lifetime superannuation transfer balance cap into retirement phase all clearly signal an intention to increase tax revenues from the broader superannuation system.

Figure 8. Taxation Revenue, Australia 2015-16

Source: ABS

Beyond these measures, a globally co-ordinated revenue / turnover based tax applied to disruptive technology businesses at the country level is another potential source of additional domestic tax revenue. There is somewhat of a precedent in targeting specific companies via the recently announced Australian major bank levy. Taking on the likes of Amazon would require enormous political will and global cooperation, something seen as unlikely at this time.

Amazon’s Australian Arrival

While lower prices are clearly a win for consumers, beyond the near-term one needs to consider the likely longer-term consequences of Amazon (and other e-commerce businesses) on everyday Australians. Amazon’s arrival will likely magnify the pressures on Australian bricks and mortar retailers and have flow-on effects for displaced workers, local communities and the broader economy. It raises the question,

By operating in the Australian retailing ecosystem, what (if any) are a disruptive global powerhouse’s obligations to pay tax in this jurisdication, and thus fund a broader framework to support potentially displaced workers?

Existing businesses have severance obligations which can extend to outplacement support. Beyond this, the obligation ultimately moves to government to provide support to these everyday Australians and their families. In the case of store closures, the impact will extend beyond the individual to the community and exert a slowing of the ‘flywheel’ of spending, investment, employment (and tax revenue collection).

Summary

The future of ‘bricks and mortar’ retailing is being challenged by the prevailing environment of technological innovation and disruption. Traditional retailers must adapt to changing consumer behaviours and refresh their offering to be more experienced-based. Whether the future physical in-store experience incorporates elements such as a whole food offering with pre-packaged easy meals, an increased luxury brand presence, an interactive fitness, lifestyle and technology experience or showcases local artists and local designers, traditional retailing must evolve its consumer offering. So next time you click to purchase an item(s) on Amazon’s or an equivalent e-commerce retailer’s website, be aware of the implications of today’s lower prices / delivery convenience and the potential future impact this may have on your journey to a secure retirement.

Clime is an independent, highly esteemed Australian fund manager specialising in value investing and focused on delivering absolute returns. To access Investing Reports and exclusive white papers, click here.

RELATED ARTICLES

Sponsored features

Dissecting the Complexities of Cash Indices Regulations: An In-Depth Analysis

Introduction In recent years, the world of finance has seen a surge of interest in cash indices trading as investors seek potential returns in various markets. This development has brought increased ...Read more

Sponsored features

The Best Ways to Find the Right Trading Platform

Promoted by Animus Webs Read more

Sponsored features

How the increase in SMSF members benefits business owners

Promoted by ThinkTank Read more

Sponsored features

Thinktank’s evolution in residential lending and inaugural RMBS transaction

Promoted by Thinktank When Thinktank, a specialist commercial and residential property lender, recently closed its first residential mortgage-backed securitisation (RMBS) issue for $500 million, it ...Read more

Sponsored features

Investors tap into cyber space to grow their wealth

Promoted by Citi Group Combined, our daily spending adds up to opportunities for investors on a global scale. Read more

Sponsored features

Ecommerce boom as world adjusts to pandemic driven trends

Promoted by Citi Group COVID-19 has accelerated the use of technologies that help keep us connected, creating a virtual supply chain and expanded digital universe for investors. Read more

Sponsored features

Industrial property – the silver lining in the retail cloud

Promoted by ThinkTank Read more

Sponsored features

Why the non-bank sector appeals to SMSFs

Promoted by Think Tank Read more

Sponsored features

Dissecting the Complexities of Cash Indices Regulations: An In-Depth Analysis

Introduction In recent years, the world of finance has seen a surge of interest in cash indices trading as investors seek potential returns in various markets. This development has brought increased ...Read more

Sponsored features

The Best Ways to Find the Right Trading Platform

Promoted by Animus Webs Read more

Sponsored features

How the increase in SMSF members benefits business owners

Promoted by ThinkTank Read more

Sponsored features

Thinktank’s evolution in residential lending and inaugural RMBS transaction

Promoted by Thinktank When Thinktank, a specialist commercial and residential property lender, recently closed its first residential mortgage-backed securitisation (RMBS) issue for $500 million, it ...Read more

Sponsored features

Investors tap into cyber space to grow their wealth

Promoted by Citi Group Combined, our daily spending adds up to opportunities for investors on a global scale. Read more

Sponsored features

Ecommerce boom as world adjusts to pandemic driven trends

Promoted by Citi Group COVID-19 has accelerated the use of technologies that help keep us connected, creating a virtual supply chain and expanded digital universe for investors. Read more

Sponsored features

Industrial property – the silver lining in the retail cloud

Promoted by ThinkTank Read more

Sponsored features

Why the non-bank sector appeals to SMSFs

Promoted by Think Tank Read more