Resources

Give the greatest gift of all: Education

Promoted by Centuria Capital Limited.

![]()

If you want the best for your children or grandchildren, an education fund that will set them on the path for a happy and successful life is the best gift you could offer them. The problem is that a good education comes at considerable expense.

Give the greatest gift of all: Education

Promoted by Centuria Capital Limited.

![]()

If you want the best for your children or grandchildren, an education fund that will set them on the path for a happy and successful life is the best gift you could offer them. The problem is that a good education comes at considerable expense.

Every parent knows that the cost of a school education is high. Even in a ‘free’ government school, parent contributions add up quickly. Excursions, uniforms, books and extra-curricular activities all need to be paid for, and if you have more than one child, these costs can be substantial. If you choose a faith-based or private school the costs are even higher. In some private schools, tuition can be $30,000 or more, before extras like books and uniforms, and according to a recent article in the Australian Financial Review fees are rising annually at a rate which far exceeds inflation.

For parents or grandparent grappling with the cost of educating even one, let alone more than one child, regardless of the choice of school the total cost is likely to look, and feel overwhelming.

And in an environment where wage growth is stagnant and education expenses are increasing at a rate far greater than inflation, what steps can you take to provide the best education possible for your children or grandchildren?

Choosing the most tax-effective way to prepare for the future.

It would be a great relief to know that you have the school fees covered with an education fund? One less expense to worry about, and the confidence of knowing you can make the best choice of school for your child or grandchild, without being unduly influenced by the price tag.

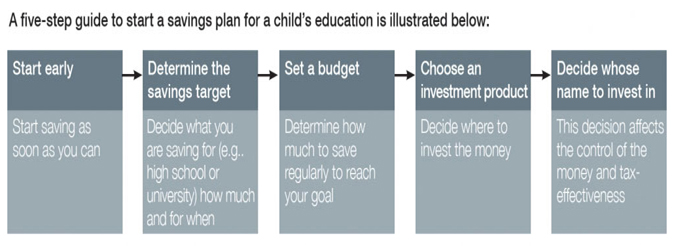

But not all investment structures are created equal, so making sure you choose a structure likely to leave you with the most money in your pocket is important. There are five simple steps to help you start – which we have outlined below.

Investment bonds – a tax effective structure

An investment bond is actually an insurance policy, with a life insured and a beneficiary, but in reality it operates like a tax-paid managed fund. And as with a managed fund, you can select from a range of underlying investment portfolios - from growth-oriented assets such as equities, through to defensive assets such as fixed interest. Portfolios can also include other asset classes and combinations of assets.

An investment bond has several advantages over other investment vehicles:

Tax effectiveness

Returns from an investment portfolio are taxed at the company tax rate (currently 30%) within the bond structure and are then re-invested. They are not distributed as income, so you do not need to include them in your annual tax return. If the bond is held for 10 years, all funds are distributed tax-free.

Depending on the investments in the underlying portfolio, dividend imputation credits may apply, making the effective tax rate less than the prevailing company tax rate. This compares very favourably with the top marginal tax rate of up to 49%.

Capital gains tax simplicity

As earnings are automatically reinvested in the bond, reinvestment dates do not need to be tracked for capital gains tax purposes. In addition, the bond holder can switch between investment options without triggering a capital gains tax liability.

Affordability

There is no limit on how much is invested in an investment bond – it may be as little as $500 or as much as $5,000,000. Importantly, you can make additional contributions every year, up to 125% of the previous year’s contribution – a terrific way to build up an education fund.

Flexibility

Investment bonds are most tax-effective when held for 10 years or more, but the funds can be withdrawn at any time as required. If the money saved is not in fact needed for education, it can be used for any other purpose.

Ownership and transfer

If saving for a child’s education, the investment can be held in the child’s name once the child is aged 10 or more. This means however, the child will gain full control to decide how to spend the money once he or she reaches age 16.

The preferred option in most cases is to hold the bond in the name of the parent or grandparent. This avoids penalty tax rates for children under 18 if they make withdrawals in the first 10 years, the adult stays in control, and the bond can be started for a child younger than age 10.

This is an option preferred by many grandparents putting money aside for a grandchild’s education. If ownership is transferred to the child, the original start date is retained for tax purposes.

Conclusion

Educations costs are rising, and the flexibility to choose the education you want for your children or grandchildren without worrying about the cost is something which can feel out of reach for many Australians. Over the past few years, the cost of education has risen more quickly than inflation and the cost of living, making the burden of educating children even more onerous for Australian families.

If you are thinking about preparing for the cost of educating your children –starting early is key, as is choosing the right structure, so you can reach your goal as quickly as possible.

RELATED ARTICLES

Sponsored features

Dissecting the Complexities of Cash Indices Regulations: An In-Depth Analysis

Introduction In recent years, the world of finance has seen a surge of interest in cash indices trading as investors seek potential returns in various markets. This development has brought increased ...Read more

Sponsored features

The Best Ways to Find the Right Trading Platform

Promoted by Animus Webs Read more

Sponsored features

How the increase in SMSF members benefits business owners

Promoted by ThinkTank Read more

Sponsored features

Thinktank’s evolution in residential lending and inaugural RMBS transaction

Promoted by Thinktank When Thinktank, a specialist commercial and residential property lender, recently closed its first residential mortgage-backed securitisation (RMBS) issue for $500 million, it ...Read more

Sponsored features

Investors tap into cyber space to grow their wealth

Promoted by Citi Group Combined, our daily spending adds up to opportunities for investors on a global scale. Read more

Sponsored features

Ecommerce boom as world adjusts to pandemic driven trends

Promoted by Citi Group COVID-19 has accelerated the use of technologies that help keep us connected, creating a virtual supply chain and expanded digital universe for investors. Read more

Sponsored features

Industrial property – the silver lining in the retail cloud

Promoted by ThinkTank Read more

Sponsored features

Why the non-bank sector appeals to SMSFs

Promoted by Think Tank Read more

Sponsored features

Dissecting the Complexities of Cash Indices Regulations: An In-Depth Analysis

Introduction In recent years, the world of finance has seen a surge of interest in cash indices trading as investors seek potential returns in various markets. This development has brought increased ...Read more

Sponsored features

The Best Ways to Find the Right Trading Platform

Promoted by Animus Webs Read more

Sponsored features

How the increase in SMSF members benefits business owners

Promoted by ThinkTank Read more

Sponsored features

Thinktank’s evolution in residential lending and inaugural RMBS transaction

Promoted by Thinktank When Thinktank, a specialist commercial and residential property lender, recently closed its first residential mortgage-backed securitisation (RMBS) issue for $500 million, it ...Read more

Sponsored features

Investors tap into cyber space to grow their wealth

Promoted by Citi Group Combined, our daily spending adds up to opportunities for investors on a global scale. Read more

Sponsored features

Ecommerce boom as world adjusts to pandemic driven trends

Promoted by Citi Group COVID-19 has accelerated the use of technologies that help keep us connected, creating a virtual supply chain and expanded digital universe for investors. Read more

Sponsored features

Industrial property – the silver lining in the retail cloud

Promoted by ThinkTank Read more

Sponsored features

Why the non-bank sector appeals to SMSFs

Promoted by Think Tank Read more