Invest

Can shares be less risky than investing in residential property?

The Australian love of property has resulted in unrivalled growth in some cities, with the belief that real estate is a safe investment. But is residential property always safer than shares?

Can shares be less risky than investing in residential property?

The Australian love of property has resulted in unrivalled growth in some cities, with the belief that real estate is a safe investment. But is residential property always safer than shares?

Many Australian cities have enjoyed a prolonged period of house price increases. It is safe to say that a large number of Australians have fallen in love with residential investment property as an asset class. The housing price increases so many investors have enjoyed has also led to a popular perception that residential property is a relatively low risk way to invest.

However, is investing in residential property really that low risk, particularly if house prices start declining?

Let’s compare the risks involved when investing in residential property versus another popular asset class – listed shares. Since this analysis will be focused on risks, it will be looking at what could happen when things go wrong, especially when prices decline. It is not meant to be a pessimistic one-sided analysis of investment property versus shares. Rather, it will present some facts about downside risks not often mentioned in glossy marketing brochures.

Borrowing risks

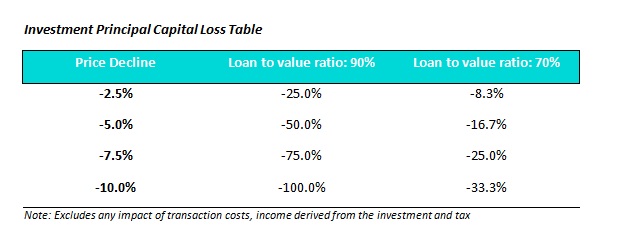

Borrowing money to buy an investment property has become a national pastime. While debt on an investment property can significantly increase investment returns when property prices are rising, the opposite is also true. The table below shows how much an investor would lose in principal capital value for a given level of decline in prices and loan-to-value ratio.

At a 90 per cent loan-to-value ratio, a house price decline of a mere 5 per cent would result in an investor losing 50 per cent of the equity they have in that investment. Is it possible Australian residential property prices can decline by 5 per cent?

The short answer is yes. In fact, in cities such as Perth and Darwin, the average house prices have already declined by this amount or more in the last 12 months.

Although it is also possible to borrow money for investing in listed shares, the maximum a bank will normally lend against listed shares is much lower than what they will lend against an investment property. For example, many banks will lend up to 90 per cent or more of the value of an investment property but will only lend up to 70 per cent against large blue chip shares. As a result, investors are not able to gear their share investments as much as property investments which leads to a measurably lower risk of suffering substantial losses on principal capital value if prices decline.

Liquidity risks

During a housing price downturn, it usually takes a longer period to sell a house. Again, let’s take Perth as an example where publicly available statistics show the average number of days for a house to sell has increased from under 50 days, when house prices were rising rapidly, to more than 70 days when house prices started to fall.

If you have an unexpected life event which requires access to cash at short notice, having the majority of your investments in residential property can be an issue. This is an even greater risk if the property has a high loan-to-value ratio in a declining house price environment as the banks are unlikely to lend any more money against that property.

In comparison, most listed shares (particularly blue chip shares) are highly liquid and can be sold for cash within a few days. Whether it is due to an unplanned need for cash or if you simply want to rapidly de-risk your investment portfolio during a market downturn, listed shares tend to have substantially less liquidity risk than a direct investment in residential investment properties.

Investment concentration risk

Do you know someone who owns a residential investment property in the same city or even suburb that they live in?

If that person’s only substantial investment is in one or two residential investment properties, they are likely to have significant investment concentration risk. For example, someone who works in Sydney, lives in in Sydney and invests only in residential property in Sydney is completely exposed to how the Sydney economy performs.

Let’s look at Detroit in the US as an example. The city suffered greatly during the depths of the global financial crisis when the unemployment rate more than doubled and house prices fell by approximately 50 per cent. Undoubtedly there would have been a lot of people in Detroit who lost the regular income from their job and also lost tremendous amounts of money on their Detroit investment properties.

Yes, Detroit is an extreme example and there are no suggestions what happened there could happen in Australia, but it does show the real danger of potential investment concentration risk.

Even if you decide only to invest in a handful of blue chip listed shares, you are likely to be much better diversified than buying one or two investment properties near where you live. Many large listed companies usually have operations across Australia, or even globally, with multiple revenue streams and provide a much better diversified investment compared to a concentrated investment property portfolio.

For all the reasons above, investing in a diversified portfolio of shares can be less risky than buying one or two investment properties, particularly during periods of price declines.

Kent Kwan, cofounder, AtlasTrend

RELATED ARTICLES

Property

Multigenerational living is moving mainstream: how agents, developers and lenders can monetise the shift

Australia’s quiet housing revolution is no longer a niche lifestyle choice; it’s a structural shift in demand that will reward property businesses prepared to redesign product, pricing and ...Read more

Property

Prestige property, precision choice: a case study in selecting the right agent when millions are at stake

In Australia’s top-tier housing market, the wrong agent choice can quietly erase six figures from a sale. Privacy protocols, discreet buyer networks and data-savvy marketing have become the new ...Read more

Property

From ‘ugly’ to alpha: Turning outdated Australian homes into high‑yield assets

In a tight listings market, outdated properties aren’t dead weight—they’re mispriced optionality. Agencies and vendors that industrialise light‑touch refurbishment, behavioural marketing and ...Read more

Property

The 2026 Investor Playbook: Rental Tailwinds, City Divergence and the Tech-Led Operations Advantage

Rental income looks set to do the heavy lifting for investors in 2026, but not every capital city will move in lockstep. Industry veteran John McGrath tips a stronger rental year and a Melbourne ...Read more

Property

Prestige property, precision choice: Data, discretion and regulation now decide million‑dollar outcomes

In Australia’s prestige housing market, the selling agent is no longer a mere intermediary but a strategic supplier whose choices can shift outcomes by seven figures. The differentiators are no longer ...Read more

Property

The new battleground in housing: how first-home buyer policy is reshaping Australia’s entry-level market

Government-backed guarantees and stamp duty concessions have pushed fresh demand into the bottom of Australia’s price ladder, lifting values and compressing selling times in entry-level segmentsRead more

Property

Property 2026: Why measured moves will beat the market

In 2026, Australian property success will be won by investors who privilege resilience over velocity. The market is fragmenting by suburb and asset type, financing conditions remain tight, and ...Read more

Property

Entry-level property is winning: How first home buyer programs are reshaping demand, pricing power and strategy

Lower-priced homes are appreciating faster as government support channels demand into the entry tier. For developers, lenders and marketers, this is not a blip—it’s a structural reweighting of demand ...Read more

Property

Multigenerational living is moving mainstream: how agents, developers and lenders can monetise the shift

Australia’s quiet housing revolution is no longer a niche lifestyle choice; it’s a structural shift in demand that will reward property businesses prepared to redesign product, pricing and ...Read more

Property

Prestige property, precision choice: a case study in selecting the right agent when millions are at stake

In Australia’s top-tier housing market, the wrong agent choice can quietly erase six figures from a sale. Privacy protocols, discreet buyer networks and data-savvy marketing have become the new ...Read more

Property

From ‘ugly’ to alpha: Turning outdated Australian homes into high‑yield assets

In a tight listings market, outdated properties aren’t dead weight—they’re mispriced optionality. Agencies and vendors that industrialise light‑touch refurbishment, behavioural marketing and ...Read more

Property

The 2026 Investor Playbook: Rental Tailwinds, City Divergence and the Tech-Led Operations Advantage

Rental income looks set to do the heavy lifting for investors in 2026, but not every capital city will move in lockstep. Industry veteran John McGrath tips a stronger rental year and a Melbourne ...Read more

Property

Prestige property, precision choice: Data, discretion and regulation now decide million‑dollar outcomes

In Australia’s prestige housing market, the selling agent is no longer a mere intermediary but a strategic supplier whose choices can shift outcomes by seven figures. The differentiators are no longer ...Read more

Property

The new battleground in housing: how first-home buyer policy is reshaping Australia’s entry-level market

Government-backed guarantees and stamp duty concessions have pushed fresh demand into the bottom of Australia’s price ladder, lifting values and compressing selling times in entry-level segmentsRead more

Property

Property 2026: Why measured moves will beat the market

In 2026, Australian property success will be won by investors who privilege resilience over velocity. The market is fragmenting by suburb and asset type, financing conditions remain tight, and ...Read more

Property

Entry-level property is winning: How first home buyer programs are reshaping demand, pricing power and strategy

Lower-priced homes are appreciating faster as government support channels demand into the entry tier. For developers, lenders and marketers, this is not a blip—it’s a structural reweighting of demand ...Read more