Invest

An insider’s guide to REITs

With interest rates still at historic lows, investors continue to search for income alternatives to more traditional assets such as cash, term deposits and bonds.

An insider’s guide to REITs

With interest rates still at historic lows, investors continue to search for income alternatives to more traditional assets such as cash, term deposits and bonds.

Hamish Wehl, head of retail funds management at Cromwell Property Group explains how one alternative, Real Estate Investment Trusts (REITs), offer liquidity, a stable yield, the potential for capital growth over time, and access to a wide range of different asset types.

Investors need options in a world of low interest rates

At the outset of the global financial crisis it would have been hard to foresee a world nine years later where global interest rates, including Australia’s, were so low.

The Reserve Bank of Australia’s official cash rate is at a record low of 1.5 per cent, with the Bank of England’s at 0.5 per cent, and the US Federal Reserve’s at 1.25 — 1.5 per cent. These levels have sent investors who rely on regular income looking for new investment strategies.

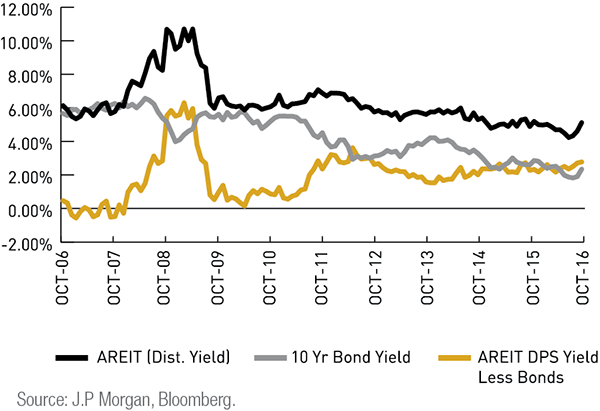

A-REITs’ distribution yield has achieved a consistent margin above the 10-year bond rate

Over the last 25 years, A-REIT dividend per unit (DPU) yields on average have been approximately 0.95 per cent in excess of the 10-year bond yield. Currently, that excess return is around 2.8 per cent. The margin above the bond rate is the reward that investors enjoy for taking on the additional risk of investing in REITs. The chart above illustrates the excess margin REITs yield (DPU) compared to the yield on government bonds.

Understanding the REIT Structure

As an investment class, listed REITs in Australia (sometimes called A-REITs) are 45 years old this year; the first, General Property Trust (GPT) was listed in 1971. Today, there are 38 REITs listed on the ASX All Ordinaries Index with a total market cap of some $125 billion.

REITs offer investors a simple way to invest in large commercial investment opportunities they would otherwise not be able to access. In turn, the rental yields delivered by these real estate assets both underpin the asset value of the REIT, and are also (due to the unique taxation structure of REITs) passed on as distributions to investors on a pre-tax basis.

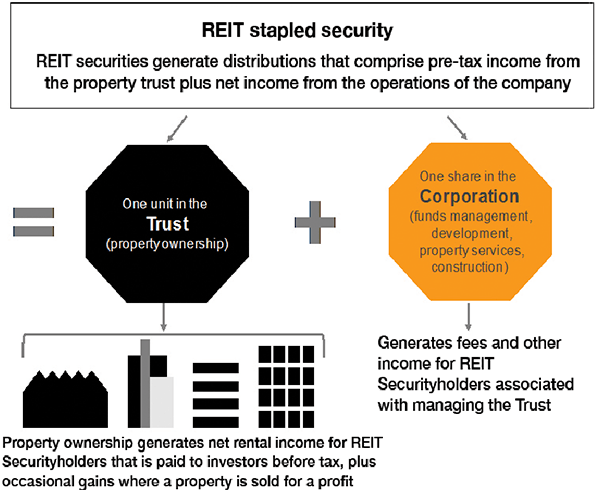

How a REIT stapled security works

Some REITs have a unique structure, called a “stapled security” where one security comprises a combination of ‘stapled’ assets: a unit in the managed investment trust (or trusts) that owns the real estate assets, and a share in the company that develops, maintains, manages and grows this asset base – see the illustration above.

Isolating the trust allows net income derived from the property assets to be passed through to investors before tax. Conversely, the company pays tax on any net profit generated by the management of the assets under a company tax structure.

Cromwell Property Group is a good example of a REIT. A Cromwell stapled security consists of a share in Cromwell Corporation Limited (CCL) and a unit in the Cromwell Diversified Property Trust (CDPT). The two are contractually bound together so that they cannot be sold or transferred separately. CCL and the CDPT are treated separately for tax purposes. This means the CDPT can maintain the legal status needed to pass through pre-tax income to investors that it earns from its properties. In other words, income earned from REITs retains its tax characteristics which pass through to investors; whether it is capital gains that can be offset by losses, or the potential for tax deferred income if distributable income exceeds taxable income.

The components of a REIT’s returns

Performance of an REIT involves two components, the first being the capital value/price of the REIT and the second being the distributions paid to the investors.

Like any listed security, REITs can be bought and sold on the share market, and therefore the price can move about with market sentiment, including during market corrections. In theory, an investor would hope for capital growth over the long term, achieved by the successful growth and management of the underlying portfolio, but in practice, capital gains or losses are a function of the purchase and/or sale price.

As an income alternative to cash, term deposits and bonds, REITs are valued for their consistent distributions which are predominantly derived from the rental income earned on the trust’s properties. With the income coming from fixed, generally long-term rental contracts, the distributions are generally more predictable and stable than dividends payable from a listed company.

In addition, REITs commonly distribute tax deferred distributions, which occur when the property trust’s distributable income is higher than its taxable income, through deductions such as depreciation on plant and equipment, capital allowances on the building structure, interest and costs during construction or refurbishment periods, and costs of raising equity.

Receiving tax deferred distributions can benefit an investor in several ways, predominantly by managing the timing of when they pay tax on the income. In some cases, tax payable may be deferred until such time as the investor’s marginal tax rate is reduced (at retirement) or is nil (in pension phase).

The importance of asset backing

What is ultimately important is the quality of the properties (capital value) in the trust, and the quality of the rental stream they generate (income). These two things can be impacted by all sorts of economic, market, company, and tenant specific issues.

In assessing the asset quality of an REIT’s portfolio, potential investors should look at factors such as the location, age, and sector (such as office, retail, industrial) of the assets held:

- Location can impact the attractiveness of the building to potential tenants.

- Age of the building will determine what level of capital spending may be required over the life of the asset.

- Depending on the wider economy, varying sectors will be in favour at different times, impacting supply and demand and hence the valuation of the asset.

In assessing the income stream of a REIT, investors should look at factors such as the type and size of tenants the properties are leased to, the term of the leases, and the value of the lease in comparison to the wider rental market:

- Tenant type can impact on the security of the lease. For example, a government department or listed company potentially may offer greater security in terms of rental guarantees.

- The term of the lease (which over the whole portfolio is stated as Weighted Average Lease Expiry or WALE) can add value to the asset as it represents a secure income stream. However, in times of high demand, a longer lease may result in rental terms that are less favourable than the current market rents.

In addition, gearing can have an impact on REITs’ returns. Gearing (the amount of debt used to finance assets) can help to increase returns on investor equity, however gearing also magnifies losses when valuations fall.

Like any investment, diversification in terms of properties, tenants, leases, geographies and sectors can help to mitigate the risks discussed. Single sector REITs (for example, retail) will have a performance that rises and falls with that sector’s cycle, whereas a REIT with assets in office, retail and industrial sectors can provide a diversified return that softens the ups and downs of the cycle.

Most importantly, investing in property via REITs should be viewed as an investment to be held over the long term, one that can generate secure, stable, growing distributions with the long-term potential for capital growth.

RELATED ARTICLES

Investment insights

APAC deal activity down by 3% in 2025 as China and India offset broader decline

The Asia-Pacific (APAC) region witnessed a moderation in deal activity in 2025, with a 3% decline in the total number of deals announced compared to the previous year. This downturn, encompassing ...Read more

Investment insights

Risk seeking among the noise: institutional investors shift strategies amid market fluctuations

In a landscape marked by evolving market dynamics, institutional investors are demonstrating a cautious yet strategic shift in their investment patterns. The latest State Street Institutional Investor ...Read more

Investment insights

2026 Portfolio Growth: Why Australia’s Savviest Investors Are Pausing Deals and Doubling Down on Operations

After a two-year sugar hit for property returns, multiple signals suggest 2026 is a danger year for buying sprees. Australian investors are being urged to slow acquisitions, protect balance sheets, ...Read more

Investment insights

Investors warn: AI hype is fuelling a bubble in humanoid robotics

The burgeoning field of humanoid robotics, powered by artificial intelligence (AI), is drawing significant investor interest, but experts warn that the hype might be creating a bubble. A recent report ...Read more

Investment insights

Australia emerges as key player in 2025 APAC private equity market

Australia has solidified its position as a significant player in the Asia-Pacific (APAC) private equity market, according to a new analysis by global private markets firm HarbourVest PartnersRead more

Investment insights

Global deal activity declines by 6% amid challenging market conditions, reports GlobalData

In a year marked by economic uncertainty and geopolitical tensions, global deal activity has experienced a notable decline, according to recent findings by GlobalData, a prominent data and analytics ...Read more

Investment insights

Furious five trends set to reshape the investment landscape in 2026

The investment landscape of 2026 is poised for transformation as five key trends, dubbed the "Furious Five" by CMC Markets, are set to dominate and disrupt markets. These trends encompass artificial ...Read more

Investment insights

Investors maintain cautious stance amid data uncertainty

Amidst the backdrop of a US government shutdown and lingering economic uncertainties, investors have adopted a neutral stance, as revealed by the latest State Street Institutional Investor IndicatorsRead more

Investment insights

APAC deal activity down by 3% in 2025 as China and India offset broader decline

The Asia-Pacific (APAC) region witnessed a moderation in deal activity in 2025, with a 3% decline in the total number of deals announced compared to the previous year. This downturn, encompassing ...Read more

Investment insights

Risk seeking among the noise: institutional investors shift strategies amid market fluctuations

In a landscape marked by evolving market dynamics, institutional investors are demonstrating a cautious yet strategic shift in their investment patterns. The latest State Street Institutional Investor ...Read more

Investment insights

2026 Portfolio Growth: Why Australia’s Savviest Investors Are Pausing Deals and Doubling Down on Operations

After a two-year sugar hit for property returns, multiple signals suggest 2026 is a danger year for buying sprees. Australian investors are being urged to slow acquisitions, protect balance sheets, ...Read more

Investment insights

Investors warn: AI hype is fuelling a bubble in humanoid robotics

The burgeoning field of humanoid robotics, powered by artificial intelligence (AI), is drawing significant investor interest, but experts warn that the hype might be creating a bubble. A recent report ...Read more

Investment insights

Australia emerges as key player in 2025 APAC private equity market

Australia has solidified its position as a significant player in the Asia-Pacific (APAC) private equity market, according to a new analysis by global private markets firm HarbourVest PartnersRead more

Investment insights

Global deal activity declines by 6% amid challenging market conditions, reports GlobalData

In a year marked by economic uncertainty and geopolitical tensions, global deal activity has experienced a notable decline, according to recent findings by GlobalData, a prominent data and analytics ...Read more

Investment insights

Furious five trends set to reshape the investment landscape in 2026

The investment landscape of 2026 is poised for transformation as five key trends, dubbed the "Furious Five" by CMC Markets, are set to dominate and disrupt markets. These trends encompass artificial ...Read more

Investment insights

Investors maintain cautious stance amid data uncertainty

Amidst the backdrop of a US government shutdown and lingering economic uncertainties, investors have adopted a neutral stance, as revealed by the latest State Street Institutional Investor IndicatorsRead more