Invest

The impact of low inflation on portfolios

With interest rates at historic lows, it’s prudent that investors understand the impact inflation has on their investment portfolios and superannuation balances.

The impact of low inflation on portfolios

With interest rates at historic lows, it’s prudent that investors understand the impact inflation has on their investment portfolios and superannuation balances.

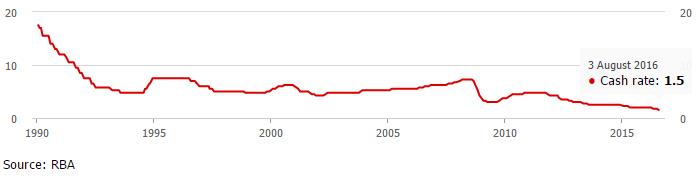

On 2 August, the Reserve Bank announced a cut to official interest rates from 1.75 per cent to a historic low of 1.50 per cent in an effort to stimulate our slowing economy and avoid the slowdown many commentators have been anxiously predicting and is now playing out in the results currently being reported by some of our largest companies such as the big banks, Wesfarmers and Telstra.

While inflationary pressures are currently lacking domestically and globally, it is important for Australian investors to avoid becoming complacent about the effects a shift in the economic climate could have on asset prices.

A lower inflationary environment means lower interest rates and income streams

Australia, like other major economies, has experienced a sustained period of disinflation, a term generally used to describe a reduction in the inflation rate. This has led the RBA and other central banks to progressively lower the cash rate to record lows to encourage investment and stimulate the economy.

Ironically, debt markets are now pricing in the prospect of deflation (falling prices) which is far worse than inflation. As an example, investors are prepared to lend their money to the Swiss government for 50 years knowing full well that they will get back less than they started with. Global growth is slowing and many investors are more concerned about getting their capital back rather than getting a return on their capital.

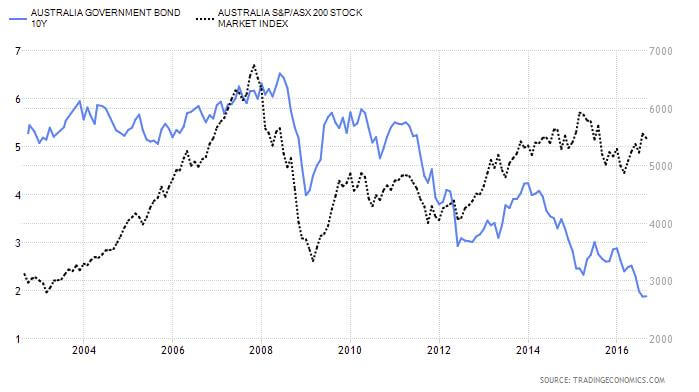

Investors seeking higher returns than those offered by bonds and cash are being forced to take on greater levels of risk to maintain income streams as returns on ‘safer assets’ such as bank term deposits continue to dwindle. Up until now (notwithstanding the associated risks), the domestic economic backdrop has been supportive for shares offering attractive and largely sustainable dividends and property (provided one has a secure tenant).

What are central banks around the world doing to counter a deflationary environment. These statistics are worth considering:

• There has been 637 interest rate cuts globally since the start of the Global Financial Crisis.

• US$12.3 trillion in asset purchases have been made by central banks through global quantitative easing (money-printing) programs.

• There is US$15 trillion in government debt returning less than zero per cent.

• There are 489 million people living in countries with official interest rates of less than zero.

Ask yourself – surely all this activity will lead to inflation at some point?

There is a commonly-held belief that investors should never try and ‘fight central banks’. In other words, if central banks want to stimulate the economy and create inflation they will succeed, and conversely if they want to slow things down and choke off inflation, they can. They have unlimited firepower – no individual, company or government can beat them.

Portfolio considerations during inflationary periods

While inflationary pressures in Australia are lacking, it is important for investors to be wary in the event of a shift in the economic climate. This is because we have experienced a sustained period of low interest rates, both domestically and globally, and investors have built up ‘safe’ assets with ‘bond-like’ characteristics to very hefty levels in the pursuit of greater income. This could unwind quickly, causing capital losses for investors, in particular those late to the party.

Assuming you are a believer in the ‘don’t fight the central bank’ theory, when inflation finally emerges, central banks will respond by raising interest rates. Provided this is done in a slow and steady fashion (which is likely) there are some assets and asset classes that are naturally expected to perform better than others.

Shares in companies that are rapidly growing their earnings should outperform the shares of more mature businesses. Additionally, companies that can pass on higher prices to their customers can be well insulated. Companies that deliver consistent earnings will do far better than those with more volatile earnings.

Listed property trusts and direct property with leases that are linked to inflation and regular market rent reviews should hold up better than those that don’t.

Commodities like gold are often considered attractive investments due to the commonly held belief that the metal acts as a hedge against inflation because it has inherent value.

Floating rate bonds (where the interest rate payable is typically a margin over the RBA cash rate or bank bill swap rate) are considered to be more attractive than fixed rate bonds, provided that the underlying issuer is not placed under undue pressure as a result of rising costs of funding.

Not surprisingly, those who have borrowed at fixed rates can also benefit, as inflation tends to erode the liability of their debt over time. Borrowers would be wise to adjust variable rate debt to a fixed rate option if possible.

Cash and shorter dated term deposits would also be attractive. Longer-dated bank deposits would not.

In all cases, it would be wise to avoid holding investments in companies and securities with high debt levels as funding costs will rise, reducing profit margins. Reduced exposure to shares and property more broadly would be prudent as safer alternatives, such as bank deposits, become relatively more attractive.

Factors to ponder before investment markets deteriorate

No trend is permanent. While it might not seem likely right now, low inflation and interest rates and rising asset prices will not last forever. With this in mind, it is extremely important to employ an investment strategy that is appropriate for your risk profile, objectives and ability to tolerate market volatility.

It would be fair to say that the longer the current environment continues, the further out the risk curve investors will go to sustain their income and the greater the pain they will experience when interest rates and asset prices eventually normalise.

Before moving your funds out of government guaranteed bank deposits into long dated property developments offering eye-watering returns, it would be wise to give serious thought to the volatility in prices you are really prepared to accept.

Retirees will likely have far less tolerance than those younger and employed. Those with more capital can afford to ride out the cycle if a downturn emerges.

Portfolio diversification is one way to minimise investment risk by spreading your wealth across a variety of different asset classes (i.e. cash, bonds, domestic and international shares, and property). Managed funds and listed investment companies that are highly diversified provide very useful roles.

Timing and identifying high-quality businesses and assets are also critical factors in achieving appropriate investment returns and protecting your capital over the longer term.

Lastly, and most importantly, it would be prudent to ensure investment and superannuation portfolios are highly liquid to ensure there is the ability to reposition your assets and/or raise cash at short notice.

David Alder, director, Alder & Partners Private Wealth Management

RELATED ARTICLES

Stock market

ASX companies make strides amidst federal budget chatter

In a week dominated by discussions surrounding the recently released FY27 federal budget, the financial landscape witnessed significant activity, particularly among ASX-listed companiesRead more

Stock market

ASX small caps report mixed results amid market optimism

The latest flurry of quarterly activities reports from ASX-listed small cap companies has provided a snapshot of the diverse and dynamic landscape of Australia's financial market. As April came to a ...Read more

Stock market

Adisyn Limited and Brazilian Critical Minerals make significant strides in their respective sectors

In a landscape where Australia's Information Technology sector often plays second fiddle to global giants, Adisyn Limited (ASX: AI1) is making waves with its innovative advancements in graphene ...Read more

Stock market

Australia's ASX 200 Energy Index surges amid Iran conflict

Australia's ASX 200 Energy Index has surged nearly 20% since the onset of the Iran conflict, marking its highest level in three months. This development positions Australia as the only developed ...Read more

Stock market

Webull launches Webull Connect, revolutionising access for Australian financial advisers

In a significant move that marks its entry into the Australian wealth management sector, Webull Securities (Australia) Pty Ltd, a subsidiary of the Nasdaq-listed Webull Corporation, has unveiled its ...Read more

Stock market

Future Generation Global boosts dividends with special payout, marking significant yield increase

Future Generation Global (ASX: FGG) has announced a significant boost to its dividend offerings for the year 2025, delighting shareholders with an increased fully franked full-year dividend and an ...Read more

Stock market

6K Additive secures A$48 million through initial public offering on the Australian Stock Exchange

6K Additive, a prominent player in the advanced metal powders and alloy additions market, has made a significant stride by successfully completing its Initial Public Offering (IPO) on the Australian ...Read more

Stock market

Institutional investors increase stock allocations to 18-year high amid cautious market shifts

In a recent development, State Street Markets unveiled the findings of its latest State Street Institutional Investor Indicators, revealing intriguing shifts in institutional investor behaviourRead more

Stock market

ASX companies make strides amidst federal budget chatter

In a week dominated by discussions surrounding the recently released FY27 federal budget, the financial landscape witnessed significant activity, particularly among ASX-listed companiesRead more

Stock market

ASX small caps report mixed results amid market optimism

The latest flurry of quarterly activities reports from ASX-listed small cap companies has provided a snapshot of the diverse and dynamic landscape of Australia's financial market. As April came to a ...Read more

Stock market

Adisyn Limited and Brazilian Critical Minerals make significant strides in their respective sectors

In a landscape where Australia's Information Technology sector often plays second fiddle to global giants, Adisyn Limited (ASX: AI1) is making waves with its innovative advancements in graphene ...Read more

Stock market

Australia's ASX 200 Energy Index surges amid Iran conflict

Australia's ASX 200 Energy Index has surged nearly 20% since the onset of the Iran conflict, marking its highest level in three months. This development positions Australia as the only developed ...Read more

Stock market

Webull launches Webull Connect, revolutionising access for Australian financial advisers

In a significant move that marks its entry into the Australian wealth management sector, Webull Securities (Australia) Pty Ltd, a subsidiary of the Nasdaq-listed Webull Corporation, has unveiled its ...Read more

Stock market

Future Generation Global boosts dividends with special payout, marking significant yield increase

Future Generation Global (ASX: FGG) has announced a significant boost to its dividend offerings for the year 2025, delighting shareholders with an increased fully franked full-year dividend and an ...Read more

Stock market

6K Additive secures A$48 million through initial public offering on the Australian Stock Exchange

6K Additive, a prominent player in the advanced metal powders and alloy additions market, has made a significant stride by successfully completing its Initial Public Offering (IPO) on the Australian ...Read more

Stock market

Institutional investors increase stock allocations to 18-year high amid cautious market shifts

In a recent development, State Street Markets unveiled the findings of its latest State Street Institutional Investor Indicators, revealing intriguing shifts in institutional investor behaviourRead more