Invest

Predictions for the major asset classes

Equity markets have staged a rebound since the middle of February after one of the worst starts to a year, but what is still to come?

Predictions for the major asset classes

Equity markets have staged a rebound since the middle of February after one of the worst starts to a year, but what is still to come?

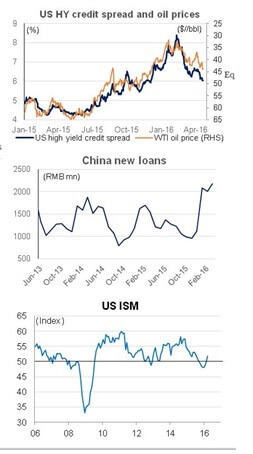

Two months ago, markets were concerned about China, oil prices and US manufacturing.

These fears have now largely dissipated, with the rally driven by supportive central bank actions, easing credit concerns and an improvement in macro data.

It is expected that these recent trends will continue and, in this environment, equities and property are preferable to fixed income and alternatives.

What a difference a couple of months can make.

The chart below shows that global equities have rebounded in March and April after falling precipitously earlier in the year.

In fact, most markets are now back where they were at the start of 2016. Commodity prices, particularly oil and iron ore, have also rallied sharply, while the Australian dollar is almost back at 80 cents.

So what was all the fuss about? Looking back, investors were concerned about a number of issues.

China’s decision to depreciate its currency in January raised questions about the state of its economy. There were fears that the sharp fall in oil prices could stir energy defaults and threaten the health of banks.

US economic data was weaker and investors were worried this would push the US economy back into recession.

More broadly, investors were questioning the effectiveness of central bank policies in further supporting growth, particularly following the poor response to Japan’s introduction of negative interest rates.

Fast forward to today, and there are several reasons why markets have rallied so handsomely:

The US Federal Reserve

The US Federal Reserve (Fed) has pulled back from its plan to raise interest rates multiple times in 2016. At its December meeting, the Fed projected that it would raise rates four times this year.

Last month, it lowered this forecast to two. Market pricing is even more conservative. This has put downward pressure on the US dollar.

China

China has signalled an intention to slow down its reform agenda and to stimulate its economy. Credit growth has picked up sharply and the central bank has been lowering reserve requirements, while fiscal spending has been ramped up.

These efforts are putting a floor under Chinese activity. Earlier concerns that China was on the brink of devaluing its currency to counter capital outflows have dissipated for now.

Recession fears easing

There has been an improvement in US macro data, helping to reduce recession fears. The manufacturing sector is expanding again, supported by rising oil prices and a lower US dollar. Labour market data has also continued to improve, while consumption has held up.

There has been easing in credit market concerns, partly due to the decision by the European Central Bank to begin purchasing corporate bonds as part of its quantitative easing (QE) program.

We do not think that the good times are over, retaining our relatively positive view on markets.

While we expect subdued economic activity to continue, it should be strong enough to ensure that Australian and international equities will outperform global bonds.

Meanwhile, property will deliver strong returns as income growth and yields remain healthy. Commodities returns will be modest but better than in recent years.

Here is an overview of our thoughts on the major asset classes:

- We have a preference for Australian equities primarily on valuations. Australia has lagged other markets during the bounce from market lows, and this is now reflected in better valuations. There is also some prospect for higher earnings as commodity prices stabilise.

- We also have a positive outlook on international equities through Europe in particular. We expect healthy earnings growth in Europe as their economic recovery progresses and the expansion of QE affects a broad range of asset classes. We are neutral on US equities, and have moved back to neutral on emerging markets, given the pick-up in Chinese activity.

- We are positive on property in Australia and internationally. Low bond yields could push capitalisation rates lower and income growth is steady in most markets.

- We are negative on fixed income, particularly international government bonds. While we don’t see rates rising sharply, coupons are so low that returns will be low. Domestic bonds should perform better than international bonds, as we assume the spread between the two will contract further.

- We are wary of alternatives. Hedge funds should continue to struggle with a reduced opportunity set from poor market liquidity and dampened volatility.

- We have a neutral view on commodities. We assume that the economic recovery in the Chinese economy provides a better backdrop for industrial metals and energy, while we forecast small positive returns from precious and agricultural commodities.

- The Australian dollar is currently trading around fair value, with the risks evenly balanced.

Tim Rocks, head of market strategy and research, BT Investment Solutions.

RELATED ARTICLES

-

Trust, technology and triage: what NSW’s ‘name and shame’ signals for real estate governance

-

Vacancy is rising, demand is resilient: A case study in defending yield as Australia’s rental cycle rebalances

-

Don’t lose the deposit: A case study in stopping real estate payment fraud — and the ROI for doing it

Property

Trust, technology and triage: what NSW’s ‘name and shame’ signals for real estate governance

NSW’s latest enforcement action on real estate trust accounts isn’t a one-off embarrassment; it’s a stress test of sector governance. With licences suspended and penalties applied, the message is ...Read more

Property

Vacancy is rising, demand is resilient: A case study in defending yield as Australia’s rental cycle rebalances

After a blistering run, Australia’s rental market is loosening at the edges. Vacancy is edging up off historic lows, rent inflation is set to moderate into 2026, yet underlying demand remains ...Read more

Property

Don’t lose the deposit: A case study in stopping real estate payment fraud — and the ROI for doing it

Deposit redirection scams are quietly eroding buyer savings and agency reputations in Australia’s property market. This case study unpacks how a mid-tier real estate group redesigned its settlement ...Read more

Property

The $12m threshold: Why portfolio value, not property count, now defines Australia’s investor elite

The old yardstick of six properties as shorthand for investment success has been overtaken by a harsher reality: in today’s market, elite status is defined by balance-sheet strength, not asset countRead more

Property

From intuition to instrumentation: How a "two-stakeholder" sales playbook lifted close rates and cut cycle times

High-stakes consumer purchases are increasingly joint decisions. When one partner is under-served, deals stall. This case study follows an Australian real estate group that rebuilt its sales motion ...Read more

Property

Selling in 2025: How to spot bad agents fast—and build an ROI-first vendor playbook

In Australia’s property market, choosing the wrong listing agent isn’t just inconvenient—it’s a textbook principal–agent failure that can wipe tens of thousands off your sale outcomeRead more

Property

Selling in 2026: How to de‑risk your agent choice and protect tens of thousands at settlement

Choosing the wrong selling agent isn’t just an inconvenience — it’s a balance‑sheet risk. In a market where digital discovery is concentrated and AI is recasting how listings are priced and promoted, ...Read more

Property

Rate resilience in Australian housing: why scarce supply is overpowering monetary tightening

Australia’s housing market is defying higher borrowing costs because the binding constraint isn’t demand—it’s supply. Brokers report persistent buyer competition and investor repositioning, while ...Read more

Property

Trust, technology and triage: what NSW’s ‘name and shame’ signals for real estate governance

NSW’s latest enforcement action on real estate trust accounts isn’t a one-off embarrassment; it’s a stress test of sector governance. With licences suspended and penalties applied, the message is ...Read more

Property

Vacancy is rising, demand is resilient: A case study in defending yield as Australia’s rental cycle rebalances

After a blistering run, Australia’s rental market is loosening at the edges. Vacancy is edging up off historic lows, rent inflation is set to moderate into 2026, yet underlying demand remains ...Read more

Property

Don’t lose the deposit: A case study in stopping real estate payment fraud — and the ROI for doing it

Deposit redirection scams are quietly eroding buyer savings and agency reputations in Australia’s property market. This case study unpacks how a mid-tier real estate group redesigned its settlement ...Read more

Property

The $12m threshold: Why portfolio value, not property count, now defines Australia’s investor elite

The old yardstick of six properties as shorthand for investment success has been overtaken by a harsher reality: in today’s market, elite status is defined by balance-sheet strength, not asset countRead more

Property

From intuition to instrumentation: How a "two-stakeholder" sales playbook lifted close rates and cut cycle times

High-stakes consumer purchases are increasingly joint decisions. When one partner is under-served, deals stall. This case study follows an Australian real estate group that rebuilt its sales motion ...Read more

Property

Selling in 2025: How to spot bad agents fast—and build an ROI-first vendor playbook

In Australia’s property market, choosing the wrong listing agent isn’t just inconvenient—it’s a textbook principal–agent failure that can wipe tens of thousands off your sale outcomeRead more

Property

Selling in 2026: How to de‑risk your agent choice and protect tens of thousands at settlement

Choosing the wrong selling agent isn’t just an inconvenience — it’s a balance‑sheet risk. In a market where digital discovery is concentrated and AI is recasting how listings are priced and promoted, ...Read more

Property

Rate resilience in Australian housing: why scarce supply is overpowering monetary tightening

Australia’s housing market is defying higher borrowing costs because the binding constraint isn’t demand—it’s supply. Brokers report persistent buyer competition and investor repositioning, while ...Read more