Invest

Plenty of value outside of the big end of town

While investors are naturally attracted to large caps, it’s smaller companies that offer the best value.

Plenty of value outside of the big end of town

While investors are naturally attracted to large caps, it’s smaller companies that offer the best value.

The point of investing in global equities is to exploit the full breadth of opportunities the equity universe has on offer, not to be dominated by exposure to companies whose market caps are larger than the GDP of most African nations.

The 10 largest companies in the MSCI World Index make up 11 per cent of the total index weight. This time last year, in the State Street Global Equity Fund we held none of the ten largest, but today we hold two of them. For example, some large banks have become more attractive on valuation and risk characteristics.

The 50 largest companies in the MSCI World Index, the smallest of which is US$105 billion in market cap, make up almost 30 per cent of the weight of the index. We have found eight worth investing in, amounting to around 10 per cent of the fund’s weight. Staples and healthcare have been the dominant exposures in this capitalisation segment.

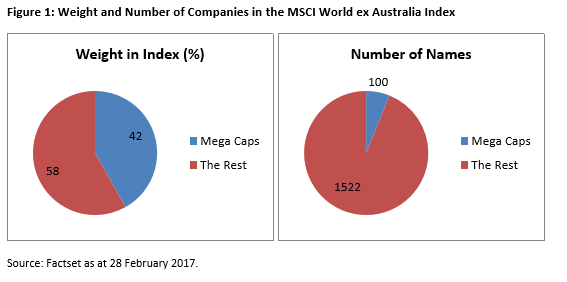

The 100 largest companies make up more than 42 per cent of the market cap of the MSCI World Index, and we have found 11 companies attractive enough to include in the fund, but which only amount to 13 per cent of the fund weight. That leaves the other 87 per cent of the fund to invest in companies outside of the big brands.

What is there beyond the mega caps?

While SSGA’s expected return on the mega cap stocks as a group (the largest 100 companies) is better than average, there are still 550 companies in the universe that have a higher expected return by our estimate. It’s not about avoiding large companies, it’s about opening up the opportunity set.

Smaller companies are fertile ground for finding greater inefficiencies in the equity market. There are 55 analysts providing Bloomberg with earnings estimates for Apple Inc, but only 16 analysts covering Waste Management Inc, the 246th largest company in the benchmark universe with a market cap of US$30 billion. The opportunities to find mispriced stocks are greater when fewer market participants are scrutinising them.

Less regulation in the US under the new administration could level the playing field for smaller companies, which previously would have been disadvantaged by fewer resources to allocate to lobbying for exemptions from taxation. A new corporate tax environment could be good for smaller companies in the US.

What’s the catch? Transaction costs.

Selling one stock to buy another involves trading costs. Not just explicit costs like brokerage or GST. These costs are tiny compared with the potential market impact associated with trading if seeking to transact on a large amount of a small company.

That’s why it is so important to understand with granularity what it costs to trade, and incorporate that into the portfolio construction decision.

In fact, we consider the expected return of every company in the market and weigh that against the expected volatility impact of including that stock in the portfolio and net of the expected cost to transact that stock. We demand a higher expected return or lower risk from smaller companies to include them because they typically incur higher market impact costs when trading. We also limit the portfolio’s position in any company relative to how much trading volume of that stock regularly goes through the market to ensure we are not left with a position that cannot be sold without too much market impact incurring too high a cost.

In today’s environment where breadth in portfolios helps to insulate against extreme outcomes from concentrated positions, investing beyond mega caps is an important ingredient in the pursuit of strong risk adjusted returns through active management.

Olivia Engel, chief investment officer global active quantitative equities deputy, State Street Global Advisors

RELATED ARTICLES

-

Trust, technology and triage: what NSW’s ‘name and shame’ signals for real estate governance

-

Vacancy is rising, demand is resilient: A case study in defending yield as Australia’s rental cycle rebalances

-

Don’t lose the deposit: A case study in stopping real estate payment fraud — and the ROI for doing it

Property

Trust, technology and triage: what NSW’s ‘name and shame’ signals for real estate governance

NSW’s latest enforcement action on real estate trust accounts isn’t a one-off embarrassment; it’s a stress test of sector governance. With licences suspended and penalties applied, the message is ...Read more

Property

Vacancy is rising, demand is resilient: A case study in defending yield as Australia’s rental cycle rebalances

After a blistering run, Australia’s rental market is loosening at the edges. Vacancy is edging up off historic lows, rent inflation is set to moderate into 2026, yet underlying demand remains ...Read more

Property

Don’t lose the deposit: A case study in stopping real estate payment fraud — and the ROI for doing it

Deposit redirection scams are quietly eroding buyer savings and agency reputations in Australia’s property market. This case study unpacks how a mid-tier real estate group redesigned its settlement ...Read more

Property

The $12m threshold: Why portfolio value, not property count, now defines Australia’s investor elite

The old yardstick of six properties as shorthand for investment success has been overtaken by a harsher reality: in today’s market, elite status is defined by balance-sheet strength, not asset countRead more

Property

From intuition to instrumentation: How a "two-stakeholder" sales playbook lifted close rates and cut cycle times

High-stakes consumer purchases are increasingly joint decisions. When one partner is under-served, deals stall. This case study follows an Australian real estate group that rebuilt its sales motion ...Read more

Property

Selling in 2025: How to spot bad agents fast—and build an ROI-first vendor playbook

In Australia’s property market, choosing the wrong listing agent isn’t just inconvenient—it’s a textbook principal–agent failure that can wipe tens of thousands off your sale outcomeRead more

Property

Selling in 2026: How to de‑risk your agent choice and protect tens of thousands at settlement

Choosing the wrong selling agent isn’t just an inconvenience — it’s a balance‑sheet risk. In a market where digital discovery is concentrated and AI is recasting how listings are priced and promoted, ...Read more

Property

Rate resilience in Australian housing: why scarce supply is overpowering monetary tightening

Australia’s housing market is defying higher borrowing costs because the binding constraint isn’t demand—it’s supply. Brokers report persistent buyer competition and investor repositioning, while ...Read more

Property

Trust, technology and triage: what NSW’s ‘name and shame’ signals for real estate governance

NSW’s latest enforcement action on real estate trust accounts isn’t a one-off embarrassment; it’s a stress test of sector governance. With licences suspended and penalties applied, the message is ...Read more

Property

Vacancy is rising, demand is resilient: A case study in defending yield as Australia’s rental cycle rebalances

After a blistering run, Australia’s rental market is loosening at the edges. Vacancy is edging up off historic lows, rent inflation is set to moderate into 2026, yet underlying demand remains ...Read more

Property

Don’t lose the deposit: A case study in stopping real estate payment fraud — and the ROI for doing it

Deposit redirection scams are quietly eroding buyer savings and agency reputations in Australia’s property market. This case study unpacks how a mid-tier real estate group redesigned its settlement ...Read more

Property

The $12m threshold: Why portfolio value, not property count, now defines Australia’s investor elite

The old yardstick of six properties as shorthand for investment success has been overtaken by a harsher reality: in today’s market, elite status is defined by balance-sheet strength, not asset countRead more

Property

From intuition to instrumentation: How a "two-stakeholder" sales playbook lifted close rates and cut cycle times

High-stakes consumer purchases are increasingly joint decisions. When one partner is under-served, deals stall. This case study follows an Australian real estate group that rebuilt its sales motion ...Read more

Property

Selling in 2025: How to spot bad agents fast—and build an ROI-first vendor playbook

In Australia’s property market, choosing the wrong listing agent isn’t just inconvenient—it’s a textbook principal–agent failure that can wipe tens of thousands off your sale outcomeRead more

Property

Selling in 2026: How to de‑risk your agent choice and protect tens of thousands at settlement

Choosing the wrong selling agent isn’t just an inconvenience — it’s a balance‑sheet risk. In a market where digital discovery is concentrated and AI is recasting how listings are priced and promoted, ...Read more

Property

Rate resilience in Australian housing: why scarce supply is overpowering monetary tightening

Australia’s housing market is defying higher borrowing costs because the binding constraint isn’t demand—it’s supply. Brokers report persistent buyer competition and investor repositioning, while ...Read more