Invest

Can shares be less risky than investing in residential property?

The Australian love of property has resulted in unrivalled growth in some cities, with the belief that real estate is a safe investment. But is residential property always safer than shares?

Can shares be less risky than investing in residential property?

The Australian love of property has resulted in unrivalled growth in some cities, with the belief that real estate is a safe investment. But is residential property always safer than shares?

Many Australian cities have enjoyed a prolonged period of house price increases. It is safe to say that a large number of Australians have fallen in love with residential investment property as an asset class. The housing price increases so many investors have enjoyed has also led to a popular perception that residential property is a relatively low risk way to invest.

However, is investing in residential property really that low risk, particularly if house prices start declining?

Let’s compare the risks involved when investing in residential property versus another popular asset class – listed shares. Since this analysis will be focused on risks, it will be looking at what could happen when things go wrong, especially when prices decline. It is not meant to be a pessimistic one-sided analysis of investment property versus shares. Rather, it will present some facts about downside risks not often mentioned in glossy marketing brochures.

Borrowing risks

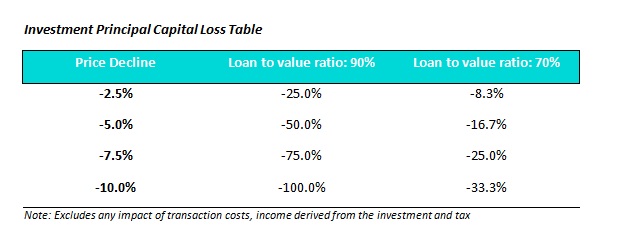

Borrowing money to buy an investment property has become a national pastime. While debt on an investment property can significantly increase investment returns when property prices are rising, the opposite is also true. The table below shows how much an investor would lose in principal capital value for a given level of decline in prices and loan-to-value ratio.

At a 90 per cent loan-to-value ratio, a house price decline of a mere 5 per cent would result in an investor losing 50 per cent of the equity they have in that investment. Is it possible Australian residential property prices can decline by 5 per cent?

The short answer is yes. In fact, in cities such as Perth and Darwin, the average house prices have already declined by this amount or more in the last 12 months.

Although it is also possible to borrow money for investing in listed shares, the maximum a bank will normally lend against listed shares is much lower than what they will lend against an investment property. For example, many banks will lend up to 90 per cent or more of the value of an investment property but will only lend up to 70 per cent against large blue chip shares. As a result, investors are not able to gear their share investments as much as property investments which leads to a measurably lower risk of suffering substantial losses on principal capital value if prices decline.

Liquidity risks

During a housing price downturn, it usually takes a longer period to sell a house. Again, let’s take Perth as an example where publicly available statistics show the average number of days for a house to sell has increased from under 50 days, when house prices were rising rapidly, to more than 70 days when house prices started to fall.

If you have an unexpected life event which requires access to cash at short notice, having the majority of your investments in residential property can be an issue. This is an even greater risk if the property has a high loan-to-value ratio in a declining house price environment as the banks are unlikely to lend any more money against that property.

In comparison, most listed shares (particularly blue chip shares) are highly liquid and can be sold for cash within a few days. Whether it is due to an unplanned need for cash or if you simply want to rapidly de-risk your investment portfolio during a market downturn, listed shares tend to have substantially less liquidity risk than a direct investment in residential investment properties.

Investment concentration risk

Do you know someone who owns a residential investment property in the same city or even suburb that they live in?

If that person’s only substantial investment is in one or two residential investment properties, they are likely to have significant investment concentration risk. For example, someone who works in Sydney, lives in in Sydney and invests only in residential property in Sydney is completely exposed to how the Sydney economy performs.

Let’s look at Detroit in the US as an example. The city suffered greatly during the depths of the global financial crisis when the unemployment rate more than doubled and house prices fell by approximately 50 per cent. Undoubtedly there would have been a lot of people in Detroit who lost the regular income from their job and also lost tremendous amounts of money on their Detroit investment properties.

Yes, Detroit is an extreme example and there are no suggestions what happened there could happen in Australia, but it does show the real danger of potential investment concentration risk.

Even if you decide only to invest in a handful of blue chip listed shares, you are likely to be much better diversified than buying one or two investment properties near where you live. Many large listed companies usually have operations across Australia, or even globally, with multiple revenue streams and provide a much better diversified investment compared to a concentrated investment property portfolio.

For all the reasons above, investing in a diversified portfolio of shares can be less risky than buying one or two investment properties, particularly during periods of price declines.

Kent Kwan, cofounder, AtlasTrend

RELATED ARTICLES

Property

Australian property’s quiet pivot: resilience hides a new competitive map

Australia’s housing market remains sturdier than the macro noise suggests, but the sources of resilience have shifted. For operators, the profit pool is migrating from ‘volume at any price’ to ...Read more

Property

Gen Z’s 5% deposit rush: how policy‑driven demand is reshaping Australia’s housing value chain

A government-backed 5% deposit guarantee has triggered a surge in first-home buyer intent among Gen Z, pulling forward demand and resetting competition across banks, brokers and buildersRead more

Property

Cautious bidders, smarter sellers: a Queensland auction case study on repricing risk

Queensland’s auction market has hit a caution cycle as buyers price in higher borrowing costs, global uncertainty and cost-of-living pressure. Clearance softness is forcing agencies to re-engineer ...Read more

Property

Trust, technology and triage: what NSW’s ‘name and shame’ signals for real estate governance

NSW’s latest enforcement action on real estate trust accounts isn’t a one-off embarrassment; it’s a stress test of sector governance. With licences suspended and penalties applied, the message is ...Read more

Property

Vacancy is rising, demand is resilient: A case study in defending yield as Australia’s rental cycle rebalances

After a blistering run, Australia’s rental market is loosening at the edges. Vacancy is edging up off historic lows, rent inflation is set to moderate into 2026, yet underlying demand remains ...Read more

Property

Don’t lose the deposit: A case study in stopping real estate payment fraud — and the ROI for doing it

Deposit redirection scams are quietly eroding buyer savings and agency reputations in Australia’s property market. This case study unpacks how a mid-tier real estate group redesigned its settlement ...Read more

Property

The $12m threshold: Why portfolio value, not property count, now defines Australia’s investor elite

The old yardstick of six properties as shorthand for investment success has been overtaken by a harsher reality: in today’s market, elite status is defined by balance-sheet strength, not asset countRead more

Property

From intuition to instrumentation: How a "two-stakeholder" sales playbook lifted close rates and cut cycle times

High-stakes consumer purchases are increasingly joint decisions. When one partner is under-served, deals stall. This case study follows an Australian real estate group that rebuilt its sales motion ...Read more

Property

Australian property’s quiet pivot: resilience hides a new competitive map

Australia’s housing market remains sturdier than the macro noise suggests, but the sources of resilience have shifted. For operators, the profit pool is migrating from ‘volume at any price’ to ...Read more

Property

Gen Z’s 5% deposit rush: how policy‑driven demand is reshaping Australia’s housing value chain

A government-backed 5% deposit guarantee has triggered a surge in first-home buyer intent among Gen Z, pulling forward demand and resetting competition across banks, brokers and buildersRead more

Property

Cautious bidders, smarter sellers: a Queensland auction case study on repricing risk

Queensland’s auction market has hit a caution cycle as buyers price in higher borrowing costs, global uncertainty and cost-of-living pressure. Clearance softness is forcing agencies to re-engineer ...Read more

Property

Trust, technology and triage: what NSW’s ‘name and shame’ signals for real estate governance

NSW’s latest enforcement action on real estate trust accounts isn’t a one-off embarrassment; it’s a stress test of sector governance. With licences suspended and penalties applied, the message is ...Read more

Property

Vacancy is rising, demand is resilient: A case study in defending yield as Australia’s rental cycle rebalances

After a blistering run, Australia’s rental market is loosening at the edges. Vacancy is edging up off historic lows, rent inflation is set to moderate into 2026, yet underlying demand remains ...Read more

Property

Don’t lose the deposit: A case study in stopping real estate payment fraud — and the ROI for doing it

Deposit redirection scams are quietly eroding buyer savings and agency reputations in Australia’s property market. This case study unpacks how a mid-tier real estate group redesigned its settlement ...Read more

Property

The $12m threshold: Why portfolio value, not property count, now defines Australia’s investor elite

The old yardstick of six properties as shorthand for investment success has been overtaken by a harsher reality: in today’s market, elite status is defined by balance-sheet strength, not asset countRead more

Property

From intuition to instrumentation: How a "two-stakeholder" sales playbook lifted close rates and cut cycle times

High-stakes consumer purchases are increasingly joint decisions. When one partner is under-served, deals stall. This case study follows an Australian real estate group that rebuilt its sales motion ...Read more