Invest

Can ethical investing actually be profitable?

Ethical investing has experienced strong growth in recent years, but how can it be implemented and does it really yield the desired results?

Can ethical investing actually be profitable?

Ethical investing has experienced strong growth in recent years, but how can it be implemented and does it really yield the desired results?

Current investors have never had more choice when it comes to investment opportunities, but with all this choice there’s always been one common objective – and that is to make a profit.

But what if you, as an investor, were able to make that profit by investing in companies or organisations that marry their commercial aims with sustainable, social and ethical values? Too good to be true? Or are we starting to experience a global trend toward sustainability and healthy living which is leading to strong financial performance?

Is there even such a thing as true ethical investing?

Paradoxically, the answer is both yes and no. Because we are driven by different sets of values, we have different definitions of what we consider to be ethical. If you strip down ‘ethical investing’ to its core, it can simply be defined as investing with a conscience.

No one ethical investment may be perfect at ticking every box for every single one of us, but isn’t it still important to support companies that are making a conscious, pro-active effort to make a positive change? This positive change can come in three forms:

1. Ethical investing – investing in companies that use a moral compass;

2. Responsible investing – not investing in companies that promote social ills or activities harmful to the environment, such as gambling, tobacco, animal cruelty, pollution etc; and

3. Sustainable investing – investing in companies of tomorrow, such as innovative technology, renewable energy, healthcare etc.

If investment shifts to more of these companies leading positive change and we start to divest away from unethical organisations, this creates a fundamental demand shift. This movement has the potential to encourage more laggard organisations in the industry to adopt a similar philosophy resulting in a fundamental supply shift.

Does investing ethically make good financial sense?

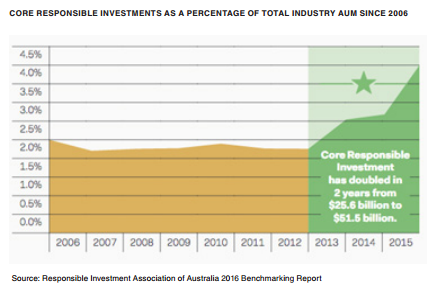

The 2016 benchmarking report from the Responsible Investment Association of Australia shows ‘core’ responsible investment funds doubling in size from $25.6 billion in 2013 to $51.5 billion in 2015. At the end of 2016, the broader responsible investment industry in Australia accounted for $633 billion in assets under management.

Ethical organisations also benefit from unintended competitive advantages in that they are less vulnerable to litigation, consumer boycotts and even catastrophes associated with unsustainable practices such as oil spills in the ocean. The devastating effects of BP’s Deepwater Horizon explosion in April 2010, where an estimated 206 million gallons of oil spilled into the ocean over the course of 85 days, is still being felt today. Consequentially, BP has spent in excess of US$56.4 billion in court fees, penalties and clean-up costs thus far, and lost 55 per cent of shareholders’ wealth within a two-month period. However, even though significant, the financial cost doesn’t even begin to address the damage done to the families of the 11 crew members who lost their lives, the wildlife, the environment and the local economy.

What should investors look for when selecting an ethical investment?

1. Is the ethical investment in fact ‘true to label’? This means understanding the investment methodology and screening process. Some funds provide a positive (inclusions of companies that are pro-active with ethical, responsible and sustainable practices) or a negative (exclusions of companies that detract from ethical, responsible and sustainable practices) screen. Some funds have both positive and negative screens, and are therefore likely to be more comprehensive in nature.

2. Do you have transparency of the underlying companies held in the fund? Having transparency of holdings is key to knowing if your investment is consistent with your ethical values. Without having full insight into the investment portfolio, you may possibly be taking on the fund manager’s own value biases, resulting in holding exposures that may not align with your values and definition of ‘ethical’.

3. What fees are you paying for your ethical investment? Although this is may not be a primary determinant in choosing an ethical investment, it is an important consideration for you, as an investor, when seeking to profit from your values. For example, there may be a big fee difference in an active style fund in comparison to a passive style ethical fund. The fees you pay on your investment will impact your return and need to be considered.

No matter which fund you choose, it’s important that you fully understand the screening process used and have insight into the exposures to make sure you can ‘profit from your principles’.

Aditi Grover, business development associate, BetaShares

RELATED ARTICLES

Property

Australian property’s quiet pivot: resilience hides a new competitive map

Australia’s housing market remains sturdier than the macro noise suggests, but the sources of resilience have shifted. For operators, the profit pool is migrating from ‘volume at any price’ to ...Read more

Property

Gen Z’s 5% deposit rush: how policy‑driven demand is reshaping Australia’s housing value chain

A government-backed 5% deposit guarantee has triggered a surge in first-home buyer intent among Gen Z, pulling forward demand and resetting competition across banks, brokers and buildersRead more

Property

Cautious bidders, smarter sellers: a Queensland auction case study on repricing risk

Queensland’s auction market has hit a caution cycle as buyers price in higher borrowing costs, global uncertainty and cost-of-living pressure. Clearance softness is forcing agencies to re-engineer ...Read more

Property

Trust, technology and triage: what NSW’s ‘name and shame’ signals for real estate governance

NSW’s latest enforcement action on real estate trust accounts isn’t a one-off embarrassment; it’s a stress test of sector governance. With licences suspended and penalties applied, the message is ...Read more

Property

Vacancy is rising, demand is resilient: A case study in defending yield as Australia’s rental cycle rebalances

After a blistering run, Australia’s rental market is loosening at the edges. Vacancy is edging up off historic lows, rent inflation is set to moderate into 2026, yet underlying demand remains ...Read more

Property

Don’t lose the deposit: A case study in stopping real estate payment fraud — and the ROI for doing it

Deposit redirection scams are quietly eroding buyer savings and agency reputations in Australia’s property market. This case study unpacks how a mid-tier real estate group redesigned its settlement ...Read more

Property

The $12m threshold: Why portfolio value, not property count, now defines Australia’s investor elite

The old yardstick of six properties as shorthand for investment success has been overtaken by a harsher reality: in today’s market, elite status is defined by balance-sheet strength, not asset countRead more

Property

From intuition to instrumentation: How a "two-stakeholder" sales playbook lifted close rates and cut cycle times

High-stakes consumer purchases are increasingly joint decisions. When one partner is under-served, deals stall. This case study follows an Australian real estate group that rebuilt its sales motion ...Read more

Property

Australian property’s quiet pivot: resilience hides a new competitive map

Australia’s housing market remains sturdier than the macro noise suggests, but the sources of resilience have shifted. For operators, the profit pool is migrating from ‘volume at any price’ to ...Read more

Property

Gen Z’s 5% deposit rush: how policy‑driven demand is reshaping Australia’s housing value chain

A government-backed 5% deposit guarantee has triggered a surge in first-home buyer intent among Gen Z, pulling forward demand and resetting competition across banks, brokers and buildersRead more

Property

Cautious bidders, smarter sellers: a Queensland auction case study on repricing risk

Queensland’s auction market has hit a caution cycle as buyers price in higher borrowing costs, global uncertainty and cost-of-living pressure. Clearance softness is forcing agencies to re-engineer ...Read more

Property

Trust, technology and triage: what NSW’s ‘name and shame’ signals for real estate governance

NSW’s latest enforcement action on real estate trust accounts isn’t a one-off embarrassment; it’s a stress test of sector governance. With licences suspended and penalties applied, the message is ...Read more

Property

Vacancy is rising, demand is resilient: A case study in defending yield as Australia’s rental cycle rebalances

After a blistering run, Australia’s rental market is loosening at the edges. Vacancy is edging up off historic lows, rent inflation is set to moderate into 2026, yet underlying demand remains ...Read more

Property

Don’t lose the deposit: A case study in stopping real estate payment fraud — and the ROI for doing it

Deposit redirection scams are quietly eroding buyer savings and agency reputations in Australia’s property market. This case study unpacks how a mid-tier real estate group redesigned its settlement ...Read more

Property

The $12m threshold: Why portfolio value, not property count, now defines Australia’s investor elite

The old yardstick of six properties as shorthand for investment success has been overtaken by a harsher reality: in today’s market, elite status is defined by balance-sheet strength, not asset countRead more

Property

From intuition to instrumentation: How a "two-stakeholder" sales playbook lifted close rates and cut cycle times

High-stakes consumer purchases are increasingly joint decisions. When one partner is under-served, deals stall. This case study follows an Australian real estate group that rebuilt its sales motion ...Read more